The world is reminding us once again of its bleakness.

I haven’t written much the past couple of months. Anxiety will probably compel me to start writing more soon.

As I have been recently, I’ll write for my drafts blog, not here. E-mail subscribers won’t see those posts until eventually I do a round-up post, like this one. I'll try to do them more frequently! When I have comments and e-mail subscriptions worked out for my new home-made blogging platform, I’ll probably bring the blogging back here. In the meantime, please consider subscribing to the drafts blog by RSS, or to my all blogs or all blogs and microblogs feeds.

For now, here are excerpts from “drafts” posted since, um, March. In reverse chronological order.

From Fascism as triage (2023-08-14):

[T]he model I would encourage you to think about is triage. For most of us today, triage is just the name they give to intake at the ER. But in wartime, it refers to the harsher practice of deciding whom to treat and whom to let die. When medical resources are scarce, you make decisions about who won’t make it anyway… Fascism is a process of internal exclusion, quite analogous to triage, although more in anger than in sadness. At a material level, a fascist order divides the polity into the worthy volk and “life unworthy of life”… This is not how human communities behave when they are secure and prosperous, when generosity, magnanimity, “civilization”, are broadly understood to be affordable public virtues. Polities “triage” the worthy from the unworthy under circumstances of perceived scarcity, of perceived threat… With medical triage it may (or may not) be sufficient for a few professionals to coldly decide, on the basis of medical facts, that these patients are a bad use of resources, while those patients may be helped by treatment. But humans writ large don’t work this way. We require moral heuristics to guide our actions, to motivate and then justify what we do… [W]e will find reasons why they deserve it. We will discover why they are in fact a danger whose dispossession is not to be lamented, but celebrated…

With this account, we can reconcile the conflicting evidence about economic anxiety and cultural resentment. At the communal level, economic factors predict which places are likely to become susceptible to a fascist dynamic, because the case for dividing and culling begins with a perception of scarcity… [A]t an individual level, within distressed communities, the people most enthusiastic to participate in the fascist dynamic are not likely to be the weak and dispossessed (who after all, might be susceptible to culling, depending what internal enemy gets identified) but those who feel safe in their own position and have preexisting resentments against candidate enemies… The members of the community who most enthusiastically participate in the thrill of fascism are not primarily the downtrodden…but relatively safe people who perceive an opportunity long denied to give effect to resentments they stewed in privately when prosperity and security bred norms of magnanimity and tolerance in their communities.

From If I were the plutocracy (2023-07-26, a response to this video):

If I were the plutocracy, I’d scapegoat immigrants, racial minorities, and sexual minorities in order to give the public someone to blame for the metastatizing pathology that results from all the material security I am sucking and sucking from them. Then I’d lavishly fund advocates of immigrants, racial minorities, and sexual minorities — the more radical, the weirder, the more aggressive, the better — to ensure a constant parade of controversies and outrages that activate people’s deep sense of identity and threat and injustice, so that they argue with one other — they might even riot and kill one another — over anything and everything but me.

If I were the plutocracy, the public would always know me to be there for them. I would be on their side in all these fights, since I would be effusively financing all the sides. Some of my organs would fund racial justice, while others would be donors to “antiwoke”, while others would ensure nicely catered luncheons for “Moms for Liberty”, and others would build underground railroads for people seeking gender-affirming care. Almost all of my organs would be deeply sincere about what they do. Meet them, you will love how genuine they are! Yet while they seem to be battling against one another, in a deeper sense they all — we all — would be pulling together in perfect harmony towards a common purpose, maintaining and expanding our extraordinary wealth and control that — surely you agree! — must be the basis for any notion of progress and civilized society, even if it does impose some unfortunate but necessary burdens on the rest of you who must serve us.

From Degrowth for Whigs (2023-07-17):

Until recently, virtual reality (like artificial intelligence) has been a joke, a transformational technology perpetually a decade away from transforming anything. But Apple's preternatural knack is to take technologies that already exist but are marginal, mere toys for hobbyists, and turn them into products so ubiquitous they upend society… What if it turns out that "mobile" was mere dress rehearsal, and the main event will be virtual reality for the rest of us? Smartphones have already delivered dematerialization. Kids aren't breathless for their drivers' licenses at age 16 anymore…

What if virtual copresence…proves to be better than the real thing? …This would be The Matrix, except emerging "voluntarily". We need those scare quotes. Acquiescing to technological change is never voluntary, exactly, at an individual level. If this is the way the world goes, you don't really have a choice but to join it. It becomes voluntary like driving was voluntary once jobs and residences became so far dispersed you could only access both with a car. But, like that evolution of the mid-to-late 20th Century, this brave new world might emerge without much in the way of overt coercion by states… [I]t is plausible — and I think the fact of ecological and environmental limits renders it quite likely — that we will collectively choose our own quasi-Matrification. To a large degree, we already have.

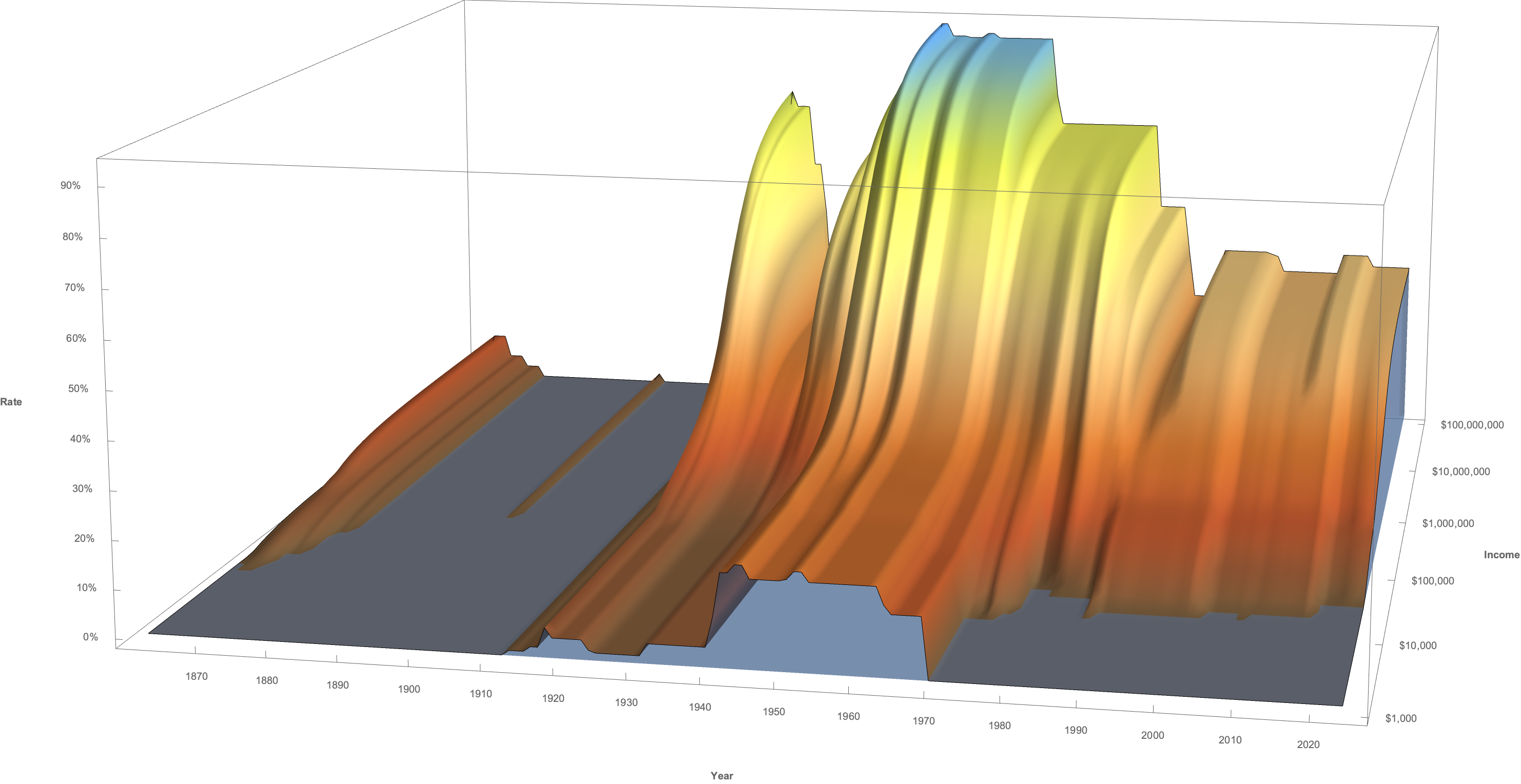

From Cornering the future (2023-07-10):

What the FIRE industry sells is not abstract at all. The product it vends is future well-being. And like candy or plane tickets or drugs, whatever future well-being we purchase has a price… From a nadir in the early 1980s…measures [of that price] rise, by the 1990s, to new heights relative to mid-20th-Century experience. [T]he attractor these measures oscillate around remains secularly higher in the post-1990s period than during the midcentury period. In other words, purchasing future well-being in the form of investment cash flows has grown a lot more expensive…

If the good we were talking about were a cans of beans, it would be obvious that an increasing price might be good for people who already have cans of beans or who can produce them, but bad for people who need to eat but don't already have any beans. There is a divergence of interest between incumbent owners and potential buyers. But with financial assets, incumbent owners go on CNBC and say, "no, it's great that the price of beans has gone up, if you don't have any yet buy however many you can because the price is going to go up more!" Incumbent owners persuade potential buyers that there is no divergence of interest, they're just a bit late to the game, no big deal, just get in on the action now.

When you are hungry and you can only buy three beans, you recognize claims like this are absurd. But give the beans a ticker symbol though and somehow it makes sense.

From Quietly expensive desperation (2023-06-04):

It is silly to attribute cross-national differences in costs to personal or psychological differences. People are public-spirited everywhere. They are public-spirited in the United States. People are greedy everywhere. They are greedy in the United States. But what is not so silly to point out is that in the United States we are structurally greedy. At a macro-level, in the name of maximizing capitalist incentives to produce, our institutions are designed to encourage self-interested income-maximizing behavior more than the institutions of other countries are. Low taxes for top-earners, tax-advantaged payouts from firms to shareholders, strong "intellectual property" rights, tolerance and even lionzation of firms that consolidate industries to extract rents, all combine to create an environment where the quantity of private income forgone for an aliquot of public-spiritedness is higher in the United States than it is almost anywhere else.

At a micro-level, the dispersion and precarity of life outcomes in the United States make us all as individuals behave as if we are more greedy than we would if all that was at stake for us was a bit of luxury… In the United States, very basic goods like having your kid in a reliably safe and decent school, or having a home in a neighborhood where your family will be safe, or getting decent health care, are far from universal. In fact, these basic goods are scarce and price-rationed. Most of us do not enjoy them, and those who do pay through the nose for them. [I]ncreasingly, the only way one can secure these goods in the United States is to price whatever services one sells into the market aggressively, gain some market power and extract some rents of your own like a true capitalist hero… Everything we can't source externally is more expensive in the United States because we are all, desperately, striving to make the labor, goods, or services that we sell — or else the hold-up costs we can impose — expensive.

From Smeagols (2023-05-27):

Outside of Mussolini's Italy and a few performative weirdoes, fascism is not an identity people adopt. It is not an ideology that people support. The better way to understand fascism is as a syndrome that people are in the throes of. The identity "fascists" adopt is, first, patriotic opponent of insidious enemies who threaten what is virtuous in my society. Then, in a later stage, devoted and obedient supporter of the great leader who will vanquish our enemies. That describes "rank and file" fascists… What about leaders of movements who seek power by manufacturing and scapegoating insidious enemies?

I don't think [Ron] DeSantis yearns to personally murder trans people. I don't think he cares one way or another about "gender ideology" (or at least that he did before he started to take actions that might demand that he persuade himself, in order to avoid cognitive dissonance and feelings of guilt). Sexual minorities are appealing sources of an internal enemy for conservative political entrepreneurs. They provoke fear and disgust at a visceral level among many conservatives, and they are supported by social liberals who can conveniently be blamed for them.

So is DeSantis a fascist? I doubt that he identifies, to himself or to anyone else, as a fascist. Almost no one does. I think a useful way to describe people like DeSantis — and Trump, and Rufo, and Knowles — is "Sméagols". Sméagol is the character in The Lord of the Rings who lusts for "my precious", a ring of power under whose influence he transforms into both a pathetic wretch and a kind of monster ("Gollum"). DeSantis is willing to conjure the social dynamic of fascism in the service of his rise to power. He may not intend the awful consequences often associated with that dynamic. Indeed he may hope that once it elevates him, he can moderate and set it aside. But just because you may be leader doesn't mean you are the master of social forces much deeper and more powerful than any single person.

From Decommodification and health care utilization (2023-05-17)

Under capitalism a persuasive apparatus emerges to sell us unnecessary baubles. Fine. There are worse things than having baubles. But superfluous health care services impose deadweight losses besides the financial transfers they provoke. Surgeries are painful and bring risks of complication. Medication has side effects, sometimes very serious. Drugs aggressively sold provoke addictions that destroy lives, families, and communities. If the ordinary result of commodification under capitalism is imperfect competition favoring sellers and then aggressive persuasion to maximize profits, then wouldn't we expect commodified health care to be overutilized? Wouldn't we expect the (important! good!) health care produced by the system be offset somewhat by manufacture of disease and addiction, matched by provider profits? And isn't this exactly what most of us think we see?

The cost of profit-motivated health-care overutilization is higher than the sum of individual disabilities and addiction occasioned by unnecessary care… The anti-vaxx movement is rendered credible to its adherents almost entirely by the conjecture that the pharmaceutical industry is very interested in getting us to take their products, and less interested in our heath. Anti-trans activists, when confronted by the strong consensus among medical providers in favor of cautious, incremental gender-affirmative care, argue that medical associations are corrupted by providers' interest in a lucrative new care market.

[M]edicine is the signal example of expertise in most people's lives. A world in which doctors can't be trusted because their financial incentives and patient welfare diverge is a world in which it will be hard for people to trust almost any form of professional expertise… For reasons beyond accessibility and cost reduction, we need to think about decommodifying medicine. Along with expertise in general.

From We haunt (2023-05-03):

-

I'm not actually going to excerpt this one. It's unusually personal, about my undergraduate alma mater, New College of Florida. New College has unfortunately become a subject of national controversy. This piece follows an even more personal post on the subject. You can also listen to this episode of the Palm Court Podcast, if you want my take on New College and what is happening to it.

From Urgency(2023-04-28):

We are in a foreign policy environment where catastrophically destructive war or even nuclear annihilation are plausible outcomes. We need to act with care, deliberation, and wisdom. Instead, political incentives militate either towards cartoon hawkishness or dogmatic isolationism, almost regardless of the actual circumstances. We need leaders who can actually negotiate and deliberate, who can understand nuance and consider compromise without those words becoming euphemisms for abandonning vital commitments.

We have to change the structure of our democracy.

And we can! Yes we can! Almost none of what ails us is embedded in our hard-to-change Constitution.

-

If our pustulent rotted Congress could rise above their pustulence and rottedness for a day or two, they could change the character of the antidemocratic Senate. It could become a body that elevates broadly popular, consensus-oriented statesmen rather than partisan sociopaths. It would take nothing more than an Act of Congress to insist that Senators be elected by approval vote.

-

We could ensure that at least four major parties emerge among the public and take seats in the House of Representatives, transforming today's stalemated trench warfare between implacably opposed camps into a more constructive dynamic where parties on their own can neither pass or block anything, where coalition building works while kneecapping a rival just advantages a different rival.

-

We could insist that elections be solely publicly financed.

-

We could properly fund Congressional staffs so they needn't outsource the basic work of legislating to think tanks bought by plutocrats and lobbyists working for industries eager to write their own laws.

-

We could even build a Supreme Court that would be trustworthy.

Any of these things, or all of them, could be accomplished by a simple Act of Congress.

From Two kinds of representation (2023-04-24):

Sometimes, we want one single person to represent an entire diverse public. In the United States, when we elect a president, he or she must look after the interests of all Americans… Sometimes, we define representative bodies whose role is to serve as "minipublics". In the US, the House of Representatives is the most prominent example. In a representative minipublic, the role of an individual member is not to stand for everyone, but to represent a particular faction or party… These two kinds of representation are profoundly different. Any conversation about electoral systems that fails to recognize this will be stunted from the start…

We don't need to repeal the Constitution to fix this. We just need to understand the different kinds of representation inherent in different Constitutional offices, and tailor our election rules accordingly. General elections for President and Senator, in every state, should be by approval voting, or some very similar system. Elections for the House of Representatives should be conducted under any of the many systems that reliably deliver proportional representation and are resistant to gerrymandering.

From Two parties make us stupid (2023-04-21):

A system that divides the public into two aggressively competing, highly cohesive factions renders an intelligent process of deliberation impossible… Intelligent deliberation requires that there exist some agent capable of weighing competing ideas without too much prejudice. It is fine — it is necessary! — that there are passionate interests on one side or another of any debate. But passionate interests don't deliberate. They advocate. You can't make a court only from the prosecution and the defense. Who would listen and synthesize the evidence? …[D]eliberation is only effective when there are judges and juries beholden to neither side, able to consider competing claims on their merits…

[W]e will never achieve perfect neutrality, objectivity, fairness, independence in our fallen human world. But these characteristics can exist in importantly different degrees… When a society becomes polarized into only two competing factions, each of which takes opposite sides over the set of issues under public contestation, there cease to be neutral-ish parties… A two-party system is a zero-sum game… In a multiparty system, on any given question, there may be factions without much skin in the game… What matters is that there be sufficient diversity and fluidity within the legislature that the swing vote usually comes from factions that has no strong, prior interest in the question considered, and no binding loyalty to any of the more interested factions.

From Taiwan (2023-04-19):

That one has a right to do a thing, however, does not imply that it's a righteous thing to do. Asserting ones rights should in general be a last, rather than first, resort. In ordinary life, nearly all of the time, we try to act with sufficient consideration of those our actions might affect that the question of rights never comes up. We assert rights only when someone will object, but we decide to act anyway… It is important that we can and do assert rights, that we have liberties that can overcome other peoples' objections. But it's also wise, when it is possible, to try to address people's concerns rather than jumping directly to an adversarial assertion of rights…

The keystone of the United States' policy with respect to Taiwan should be mutuality. Our position should be that we support any change in Taiwan's status so long as it is voluntarily agreed by both China's government and the de facto government of Taiwan. Voluntarily is important. The United States supports Taiwan, militarily and otherwise, only so that it cannot be coerced by China. If, at some point in the future, a convergence occurs so that China and Taiwan become ready to conclude a "peaceful reunification", that would be wonderful. If, in some future, friendly and mutually beneficial cross-strait relations lead China to become less concerned with exerting formal sovereignty over Taiwan and the parties jointly negotiate a more autonomous status for the island, that would be great too… For the forseeable future, no agreement is likely, so the parties will have to be patient. An awkward peace is so much better than the alternative.

From Systemic means it's not your fault (2023-04-10):

Much of the resentment that has condensed onto the term “wokeness” derives, I think, from people's perception that they stand accused, unjustly, of crimes they did not commit… [But a] structural problem demands a systematic solutions, usually in the form of public action. It is not an individual's fault, or within an individual's capability, to remedy.

I wish that those of us more on the “woke” side of the debate were clearer about this. When we say that racism or other social disparities are “systemic” or “structural”, we are absolving, not condemning, nearly everyone, as individuals… Systemic injustice is not your fault. But we’d love it if you’d help to fix it.

From Alignment is the problem of God's love (2023-04-06)

The presupposition behind AI “alignment” is that artificial intelligence technologies will grow into something much more capable than we are, with a kind of autonomous will or volition… Sufficiently advanced AIs, powerful beyond imagination and driven by their own wills, would be indistinguishable from gods. The alignment problem, then, is how do we encourage the emergence of a just and loving god or gods? But we have never found consensus on how a just and loving god should behave…

If alignment is god’s love, what does that make misaligned AI? Should we consider GPT training runs as the high-tech equivalent of rituals with pentagrams by power-mad occultists?

Am I wrong that the community that most urgently brings us these questions were once known as internet atheists? For what, if anything, does cosmic irony constitute evidence?

From State as coordination (2023-03-31)

Instead of defining the boundaries of the state by legal formalities — this institution is an agency of the education department, while that institution is organized as a private corporation — …define the state functionally, as the panoply of institutions that serve to coordinate human behavior at the scale that the formal state superintends… A small bank…may genuinely be private, because what it does or does not do will have mostly localized and idiosyncratic effects. But the banking system — even in a better, counterfactual, world with a banking system made entirely out of small banks — is part of the state. The banking system is a core means by which we coordinate economic behavior at scale… The system is state, and should be democratically managed. The elements are private, with owners who enjoy liberty rights. There are tensions there, but effective governance depends on managing those tensions.

Perhaps more jarringly, under this approach the conventional contradistinction between state and market is rendered absurd… The market is the primary means by which we coordinate behavior at national scale, in the service of internal goals like general prosperity or external goals like achieving moon shots or winning wars. So the market is properly classified as an element of the state… As individuals and moderate sized businesses, we maintain liberty rights against the formal state. Regulatory choices may shape our incentives, but we make our own decisions and set our own prices. But whether we like it or not, functionally the state must be responsible for market outcomes in aggregate, because the large-scale social coordination whose quality it is the responsibility of the state to support is itself primarily a market outcome…

[A] trick of states, especially the states we describe as liberal, is to launder massive wallops of state coercion through markets, and then deny they are exercising any form of coercion at all. Allowing the formal state to pretend, absurdly, that it stands apart from the market, to proclaim that the key institution that performs the function of the state is unfortunately some external fact of nature, provides politicians and bureaucrats with a commodity they value very highly: plausible deniability. Conceiving of state and market as distinct does not coherently constrain the modern state, because nation-scale markets cannot function without extensive state construction, regulation, and support. However, maintaining the conceit does help state actors — and the private interests who lobby them! — avoid accountability for outcomes that in fact result from political choices.