Greece

Greece is a remarkable country full of wonderful people, but along dimensions of development and governance, the place is plainly pretty fucked up. It has been fucked up that way for a long time, for decades at least. This has never been secret. Anyone who has visited Athens knows it has far more in common with Bucharest or Istanbul than with orderly Western European capitals. In the run up to Greece’s joining the Euro, everyone who wanted to know knew that Greece’s qualifications to join the Eurozone were, shall we say, ambitious. Mainstream establishment banks “helped” Greece and other Southern European countries with accounting fudges that, while perhaps obscure, were not secret even at the time. Despite protestations when these deals hit the news in 2010 that officials were “shocked, shocked”, they were explicitly blessed by the agency that compiles the statistics on which Eurozone entrance was based in 2002 and Greece’s gaming was extensively reported in 2003 (ht Heidi Moore, both cites). The Euro was and ought to be primarily a political enterprise. In order to sell the common currency to Northern European elites, its architects required Eurozone members to meet strict “convergence criteria” and especially the requirements of the Stability and Growth Pact. But in practice, those criteria have always been interpreted flexibly. Most Eurozone members have broken their promises at one point or another, including both Germany and France. The Euro was a unification project, and erred (not unreasonably, I think) on the side of building a big tent.

Germany and France may have missed their Stability and Growth commitments now and again, but they are not fucked up like Greece is. Greek governments — not the current, much maligned Syriza, but decades of its predecessors — treated the state like a teat from which clients and friends of electoral victors might suck. The Greek state has been a shady, opportunistic borrower, no doubt, the kind of character no one would lend money to with any great expectation of seeing it back.

And yet, that’s precisely what bankers in the relatively not-fucked-up Eurozone countries did! These people were not naïfs. They knew the Greek state was sketchy. But precisely because it was sketchy, prior to the financial crisis its debt paid slightly higher interest rates than that of safer Eurozone sovereigns. European banking regulations attached zero risk weights to all EU sovereigns, rendering it nearly costless for banks to simply manufacture deposits to purchase sovereign debt. Eurozone sovereigns were default-risk-free as a regulatory matter and currency-risk-free from the perspective of Eurozone banks. The European financial system was architected to make lending to Greece — and Spain and Portugal and Italy — a money machine for bankers with little career risk over a medium term. Sketchy credits tend to punch above their weight in terms of volume of issuance, so there was a lot of nice paper to buy. The bankers who lent to these states understood perfectly well that there was in fact a long-term risk, an uncertainty, a constructive ambiguity. They lent anyway, and took home very nice salaries and bonuses for doing so. It was conventional to lend, the mainstream consensus was that credit risk was over and worry warts were old-fashioned, Europe was strong and would work this out. If the worry warts turned out to be right, it was likely years away, IBGYBG.

When the game was up, when the global house of credit cards collapsed in the late Aughts, European leaders had a choice. They had knowingly and purposefully brought weak states into the Eurozone, because they genuinely, even nobly, wished to build a large, strong, United Europe. When they did so, they understood there would be crises. A unified Europe, they had always claimed, would be forged one crisis at a time. The right thing to have done for Europe at this point would have been to point out the regulatory errors and misaligned incentives that encouraged profligate lending and enabled corruption and waste among borrowers, and fix those. Banks that had made bad loans would acknowledge losses. The banks themselves would have to be restructured or bailed out.

But “bank restructuring” is a euphemism for imposing losses on wealthy creditors. And explicit bank bailouts are humiliations of elites, moments when the mask comes off and the usually tacit means by which states preserve and enhance the comfort of the comfortable must give way to very visible, very unpopular, direct cash flows.

The choice Europe’s leaders faced was to preserve the union or preserve the wealth, prestige, and status of the community of people who were their acquaintances and friends and selves but who are entirely unrepresentative of the European public. They chose themselves. The formal institutions of the EU endure, but European community is now failing fast.

It is difficult to overstate how deeply Europe’s leaders betrayed the ideals of European integration in their handing of the Greek crisis. The first and most fundamental goal of European integration was to blur the lines of national feeling and interest through commerce and interdependence, in order to prevent the fractures along ethnonational lines that made a charnel house of the continent, twice. That is the first thing, the main rule, that anyone who claims to represent the European project must abide: We solve problems as Europeans together, not as nations in conflict. Note that in the tale as told so far, there really was no meaningful national dimension. Regulatory mistakes and agency issues within banks encouraged poor credit decisions. Spanish banks lent into overpriced real estate, and German banks lent to a state they knew to be weak. Current account imbalances within the Eurozone — persistent and unlikely to reverse without policy attention — implied as a matter of arithmetic that there would be loan flows on a scale that might encourage a certain indifference to credit quality. These were European problems, not national problems. But they were European problems that festered while the continent’s leaders gloated and took credit for a phantom prosperity. When the levee broke, instead of acknowledging errors and working to address them as a community, Europe’s elites — its politicians and civil servants, its bankers and financiers — deflected the blame in the worst possible way. They turned a systemic problem of financial architecture into a dispute between European nations. They brought back the very ghosts their predecessors spent half a century trying to dispell. Shame. Shame. Shame. Shame.

Until the financial crisis, people like, well, me, were of two minds about the EU’s famous “democracy deficit”. On the one hand, I believe that good governance requires accountability to and participation of the broad public. On the other hand, before the crisis, I was willing to cut the Euro-elite a lot of slack. I’m an American born in 1970, but my life is largely framed and circumscribed by events in Europe during the Second World War. I grew up on a diet of “never again”. I am writing these words from my grandfather’s villa on the Romanian Black Sea, which my mother worked doggedly to recover in an act of sheer vengeance for what this continent’s history did to her father. I was inclined to support Europe’s democratic fudges when they were about diminishing and diffusing the still palpable possibility here of reversion to ethnonational conflict. To see European institutions deployed precisely and with great force in the service polarization across national borders has radicalized and made a populist of me (as have analogous betrayals among the political leadership of my own country). If I were Greek, I would surely be a nationalist now.

With respect to Greece, the precise thing that European elites did to set the current chain of events in motion was to replace private debt with public during the 2010 first “bailout of Greece”. Prior to that event, it was obvious that blame was multipolar. Here are the banks, in France, in Germany, that foolishly lent. Not just to Greece, but to Goldman’s synthetic CDOs and every other piece of idiot paper they could carry with low risk-weights. In 2010, the EU, ECB, and IMF laundered a bailout of mostly French and German banks through the Greek fisc. Cash flowed into Greece only so it could flow out to rickety banks. Now, suddenly, the banks were absolved. There were very few bad loans left on the books of European lenders, everyone was clean, no bad actors at all. Except one. There were the institutions, the “troika”, clearly the good guys, so “helpful” with their generous offer of funds. And then there was Greece. What had been a mudwrestling match, everybody dirty, was transformed into mass of powdered wigs accusing a single filthy penitent (or, when the people with their savings in just-rescued banks decide to be generous, a petulant misbehaving child). [antidote]

Among creditors, a big catchphrase now is “moral hazard”. We cannot be too kind to Greece, we cannot forgive their debt with few string attached, because what kind of precedent would that set? If bad borrowers, other sovereigns, got the idea that they can overborrow without consequence, if Spanish and Portuguese populists perceive perhaps a better deal is on offer, they might demand that. They might continue to borrow and expect forgiveness, and where would it end except for the bankruptcy of the good Europeans who actually produce and save?

The nerve. The fucking nerve. Lenders, having been made nearly whole on their ill-conceived, profit-motivated punts, now fear that if anybody is nice to somebody who doesn’t deserve it, where will it end? I’d resort to that cliché about chutspa, the kid who murders his parents then seeks leniency ‘cuz he’s an orphan. But it’s really too cute for the occasion.

For the record, my sophisticated hard-working elite European interlocutors, the term moral hazard traditionally applies to creditors. It describes the hazard to the real economy that might result if investors fail to discriminate between valuable and not-so-valuable projects when they allocate society’s scarce resources as proxied by money claims. Lending to a corrupt, clientelist Greek state that squanders resources on activities unlikely to yield growth from which the debt could be serviced? That is precisely, exactly, what the term “moral hazard” exists to discourage. You did that. Yes, the Greek state was an unworthy and sometimes unscrupulous debtor. Newsflash: The world is full of unworthy and unscrupulous entities willing to take your money and call the transaction a “loan”. It always will be. That is why responsibility for, and the consequences of, extending credit badly must fall upon creditors, not debtors. There is one morality tale that says the debtor must repay, or she has sinned and must be punished. There is another morality tale that says the creditor must invest wisely, or she has stewarded resources poorly and must be punished. We get to choose which morality tale we most use to make sense of the world. We do, and surely should, use both to some degree. But if we emphasize the first story, we end up in a world full of bad loans, wasted resources, and people trapped in debtors’ prison, metaphorical or literal. If we emphasize the second story, we end up in a world where dumb expenditures are never financed in the first place.

But don’t the Greeks want to borrow more? Isn’t that what all the fuss is about right now? No. The Greeks need to borrow money now only because old loans are coming due that they have to pay, and they have been trying to come to an agreement about that, rather than raise a middle finger and walk away. The Greek state itself is not trying to expand its borrowing. Greece’s citizens and businesses would like to expand the country’s borrowing indirectly, by withdrawing Euros from Greek banks that the Greek banks won’t be able to come up with unless they are allowed to expand their borrowing from the ECB. That is, Greece’s citizens are in precisely the place France’s citizens and Germany’s citizens were in 2010, at risk that personal savings maintained as bank deposits will not be repaid. Something was worked out for French and German citizens. Other than resorting to the ethnonational stereotypes that European elites have now revived in polite company, what is the justification for a Greek schoolteacher losing her savings that wouldn’t have applied just as strongly to a French schoolteacher five years ago? Because Greeks are responsible, as individuals, for what the governments they elect do? Well, then I deserve to be killed for what my government has done in Iraq and elsewhere. Is that where we want to go?

If citizens aren’t going to be held responsible for their governments’ bad debts, how will sovereigns borrow at all? Well, how do firms raise equity, when an equity claim makes no promise whatsoever that any cash will be returned? People invest in shares not because they have any sword of Damocles to hold over the enterprise, but because they believe the firm will engage in activities sufficiently productive that throwing some cash back to investors will not be burdensome, and because firms know repayment enhances access to continued finance. The same is true of sovereigns like the United States or the UK, which borrow easily in currencies they can print any time. Nothing prevents the US from conjuring $100T USD and handing it out to citizens, engineering a one-time inflation that leaves outstanding bonds nearly worthless. It wouldn’t even constitute a default. But the US has organized itself in ways that persuade creditors that their funds will be treated reasonably. Inflexible debt sows seeds of coercion and enmity between borrower and lender. Equity-like arrangements, including “debt” denominated in securities issuable at will by the debtor, require and encourage trust and collaboration. Sovereign debt in particular should always look like the latter, not the former, given the regularity with which government borrowings are disbursed into insiders’ bank accounts rather than used to aid the publics who might be pressured to foot the bill.

Greece should see its debts forgiven, pretty much wholesale. That forgiveness should be understood as a default, with future investors warned. Insured deposits in Greek bank accounts should be made whole, uninsured deposits should be “bailed in”, Greece’s banking system should be integrated into a much more carefully regulated European banking system that eschews investment in individual sovereigns entirely, Germany as much as Greece. Let sovereigns sell securities to the market, where incentives for careful credit allocation are sharper than they are within banks. Let European banks hold only claims against the ECB when they want a risk-free instrument. If Spain or Portugal or Italy wish to haircut or repudiate their existing debt, let them, at cost of future market access. Sovereigns have an option to default full stop. Investors in sovereign securities must price that. If perceived credit risk leaves public finance too expensive Europe-wide, then the EU should develop a mechanism whereunder states are permitted to sell equity securities to the ECB up to a fixed limit, set uniformly across Europe in per capita terms.

I’ll end this ramble with a discussion of a fashionable view that in fact, the Greece crisis is not about the money at all, it is merely about creditors wresting political control from the concededly fucked up Greek state in order to make reforms in the long term interest of the Greek public. Anyone familiar with corporate finance ought to be immediately skeptical of this claim. A state cannot be liquidated. In bankruptcy terms, it must be reorganized. Corporate bankruptcy laws wisely limit the control rights of unconverted creditors during reorganizations, because creditors have no interest in maximizing the value of firm assets. Their claim to any upside is capped, their downside is large, they seek the fastest possible exit that makes them mostly whole. The incentives of impaired creditors are simply not well aligned with maximizing the long-term value of an enterprise.

If it were 2009, I might have been persuaded that the corporate bankruptcy analogy is poor, that Europe’s interest in the development and cohesiveness of its empire would substitute for narrow economic incentives (which should in any case be blunted, since they are the incentives of 27 different fiscs). If the past five years had not happened, I might be open to the argument made here (ht platypus) that, having extended the maturity of a large quantity of debt far into the future, creditors’ position is more like equity, since the fraction of face value creditors eventually recover is dependent upon Greece’s long-term growth.

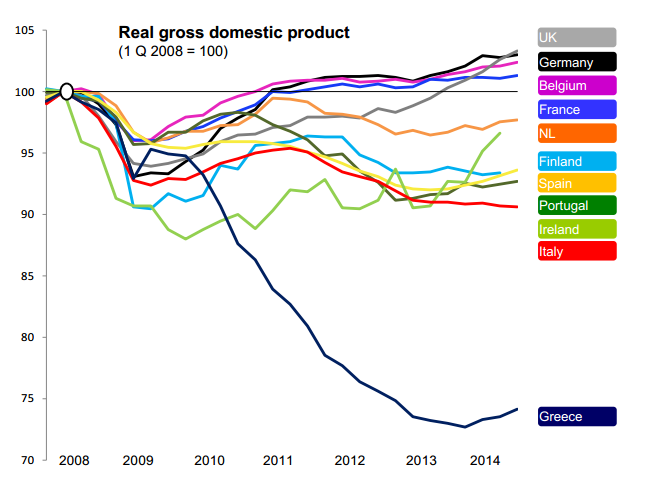

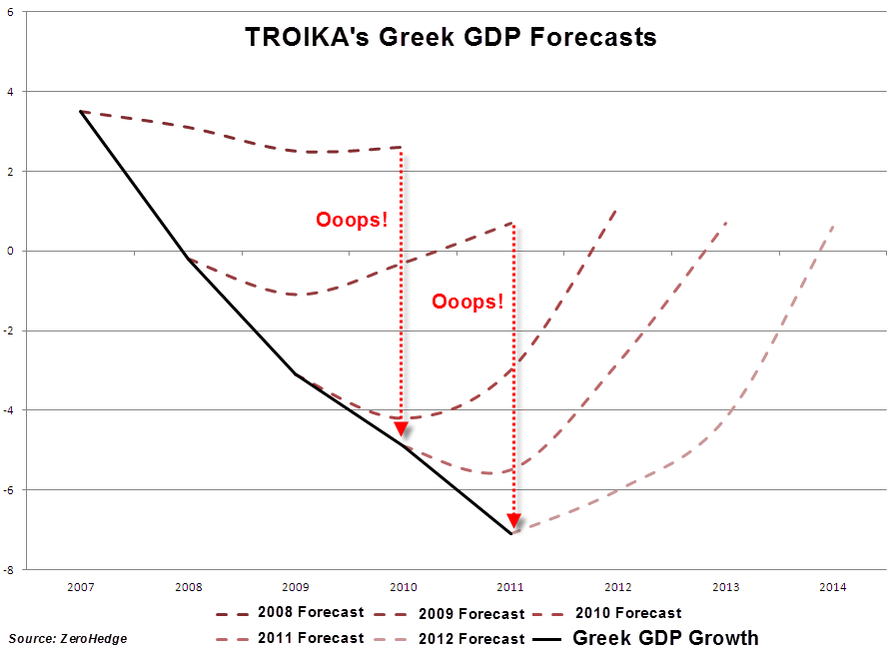

But we have had five years to observe creditors’ tender ministrations, under governments that complied with creditors’ every demand. This has been the result:

Euroelite apologists cite the small upturn at the very end of the graph to say, “See! Things were going swimmingly until the five-month old Syriza government screwed it all up. They just had to stick with the program! It was working! The darkest hour comes before the dawn!” These people, they are sophisticated highly educated people. You can trust them. Check out this track record:

The fact of the matter is no country, not Germany, not France, would voluntarily put up with the sort of “adjustment” that has been forced on Greece, for the good reason that gratuitous great depressions are not actually helpful to an economy. Creditors have had five years to mismanage Greece and they’ve done a startlingly effective job. Syriza has had five months to object. However much you may dislike their negotiating style, however little you think of their competence, Greece’s catastrophe was not Syriza’s work. If creditors respond to Syriza’s “intransigence” with maneuvers that cause yet more devastation, that will be on the creditors. Blaming victims for having insufficiently perfect leaders is standard fare for apologists of predation. Unfortunately, understanding this may be of little comfort to the disemboweled prey.

Europe’s creditors are behaving exactly as one might naively predict private creditors would behave, seeking to get as much blood from the stone as quickly as possible, indifferent to the cost in longer-term growth. And that, in fact, is a puzzle! Greece’s creditors are not nervous lenders panicked over their own financial situation, but public sector institutions representing primarily governments that are in no financial distress at all. They really shouldn’t be behaving like this.

I think the explanation is quite simple, though. Having recast a crisis caused by a combustible mix of regulatory failure and elite venality into a morality play about profligate Greeks who must be punished, Eurocrats are now engaged in what might be described as “loan-shark theater”. They are putting on a show for the electorates they inflamed in order to preserve their own prestige. The show must go on.

Throughout the crisis, European elites have faced a simple choice: Acknowledge and explain to electorates their own mistakes, which do not line up along national borders of virtue and vice, or revert to a much older playbook and manufacture scapegoats.

Such tiny, tiny people.

Update History:

- 4-Jul-2015, 11:45 a.m. EEDT: Capitalize S in “Black Sea”, “then” ⇒ “than”

- 4-Jul-2015, 7:15 p.m. EEDT: “The brought back” ⇒ “They brought back”; add apostrophe to “debtors’ prison”.

Thank you so much for posting this. It put into words what I’ve been mulling over for the last month now.

July 3rd, 2015 at 7:54 pm PDT

link

This reinforces the notion of many of us that you are the best. Thank you. Thank you. Thank you.

July 3rd, 2015 at 8:11 pm PDT

link

The 2010 transaction wasn’t a “laundered” bailout of French and German banks. Dig into the numbers. It was a bailout of Greek banks, two of the biggest of which (Geniki and Emporiki) were owned by French parents. If that bailout hadn’t happened, CA and SG would simply have allowed their subsidiaries to fail, and limited their losses to the equity. Greek depositors, on the other hand, would have lost everything (and I mean everything – the Greek deposit insurance fund is laughably small).

July 3rd, 2015 at 9:30 pm PDT

link

Outstanding summary of the roots do the Greek Crisis. We all knew that Greece’s entrance into the currency union was based on bogus fiscal and financial data. What we did not anticipate was that French and German (and Finnish) elites would turn the Euro from a means of containing and channelling German political-economic power into a means by which Germany could, without legitimate purpose, wreck havoc on another European nation.

July 3rd, 2015 at 9:35 pm PDT

link

Thank you for putting it down so clearly. A compatible, possibly complementary, explanation could be that post-unification Germany may be up to her old tricks. A German European Union and all that. This possibility is bothering people as it is associated with the emergence of uncannily familiar alliances and the reappearance of traces of old scary national behaviors, such as tolerance of collective punishment, predatory superiority and aggression towards the weak, strong propaganda and scapegoating, and last but not least, of deluded public acceptance of unverified “facts”.

July 3rd, 2015 at 9:36 pm PDT

link

“The same is true of sovereigns like the United States or the UK, which borrow easily in currencies they can print any time.”

Very good except for this.

Sovereigns can ‘borrow’ easily because they borrow automatically when people save to excess in the sovereign currency. They are the ‘borrower of last resort’ – enabling the excess saving that would otherwise be destroyed by a ‘paradox of thrift’ recession.

In other words they borrow in precisely the same way your bank borrows when you pay in your salary. It’s interesting we talk about being in credit at the bank, but never about being in credit with the government.

The only other aggregate alternative in a non-convertible floating rate currency is to spend the money, which creates taxation and moves the budget closer to balance anyway.

Paying people interest in a sovereign nation is a policy choice.

Greece is a state in a union, like Alabama, Scotland or Queensland. It has a state government with similar control over its affairs as its counterparts elsewhere in other unions.

July 3rd, 2015 at 11:07 pm PDT

link

“Greek depositors, on the other hand, would have lost everything (and I mean everything – the Greek deposit insurance fund is laughably small)”

Or the ECB, like the UK, could have bolstered all the country’s deposit insurance funds so that insured depositors lost nothing.

It was very easy to let the banks fail and cover the depositors *which is how it is supposed to work*. That it didn’t shows you that the central banks are under political control by bankers.

July 3rd, 2015 at 11:19 pm PDT

link

Whatever. 10 years after being warned Greece still spends more than what it collects.

No one need such an irresponsible country.

July 3rd, 2015 at 11:44 pm PDT

link

[…] at 3:31 on July 4, 2015 by Mark Thoma Greece – interfluidity The ideologues of the Eurozone – mainly macro Did the IMF provide support to Syriza? – […]

July 4th, 2015 at 12:31 am PDT

link

Between June 2004 and November 2009, with Basel II, the regulators in the Basel Committee allowed banks to lend to the Government of Greece against only 1.6 percent in capital, which implies an authorized leverage of over 60 to 1 when lending to Greece…

That of course caused the banks to lend way too much to the Greek government.

Greek citizens, beware of Basel Committee’s bank regulators bringing gifts to your government!

http://teawithft.blogspot.se/2015/06/europe-you-want-truth-it-was-not-euro.html

July 4th, 2015 at 2:18 am PDT

link

A lot of talk went through the media about the Greek crisis. Yet most of it is how to solve, or not to solve the problem of Greek debt, which is in its essence a monetary problem, that can be solved relatively easily by monetary tools, that as were shown can be very effective if implemented correctly. But as it happens to be, monetary policy influences the physical scenery too, mainly if it is all about greed, deception and theft, and for very long time, like in the case of Greece. The mounts of loans that the Greek politicians took, since they entered the Eurozone based on false statistics, where used mainly to enrich the Greek plutocracy. To be able to do so undisturbed, they corrupted the whole Greek nation by enabling to them standard of living of Germany, without to be productive like Germany. This policy not only did not prepared the Greek economy for the D-day, when eventually the creditors will ask for loan repayments, but in contrary. The wages, the pension system, the business environment, were all formed not on economic achievements but on protective incorporation of employment associations, to protect those who are members of the incorporation from those who are not. These incorporations could be workers or profession unions or association of drivers, etc. When the hangover day came, all this associations and their members, will stuck together even more tightly than ever before. 50% youth unemployment is direct result of this situation.

These phenomena evolved in decades and there is no monetary policy, which can resolve it. So even if most of the Greek debts would be erased it couldn’t help to create a long term sustainable Greek economy.

Economics is not just about curves and numbers. It is also about people, their intentions and their acts within an economic, political and social system. If certain senior employees created in an organization where they are employed an union, which prevents from more talented new employees to bring positive changes to the organization (and I am not against the unions as principle, only if it fights for self destructive policy ) its damage to economy can’t be quantified. If certain entity becomes a monopoly and increases the prices of the products, it’s negative influence is also not measurable in the GDP. If highly educated young Greeks can’t get jobs, because the senior less educated and less effective Greeks are protected by laws, unions, professional guilds, etc. the negative impact of this state on the GDP is also not measurable.

So if Greece wants to overcome its problems, reduction of its debts is not enough. Somehow this economic train has to be relocated to a different track.

One other issue, there are commentaries in the media, where “professional economists” pointed out, that at 2008, Greece debt was “only” 100% out of the GDP, and now with the shrink of the GDP, even after its reduction it became 170%. This claim is worse than a lie, it is professional deception, done intentionally our out of ignorance. Before the crisis, the Greek GDP per capita was close to that of Germany, mostly financed by loans. The GDP can be sometime a very sleazy measure instrument, since it measures the short term economic performance calculated out of national income. Out of definition General Domestic Product equals to General Domestic Income. But this income doesn’t makes difference between income generated out of merchandise or service production an the income created by financial operation which creates indebtedness. So the Greek GDP did not represent real values, but values generated by debts, which became the very core of all the economic problems of Greece.

July 4th, 2015 at 3:10 am PDT

link

Outstanding – thank you.

July 4th, 2015 at 3:33 am PDT

link

Do you think the Troika is responsible for everything in Greece since 2008?

Do you think 2008 is a reasonable model for Greece to want to go back to, or an unsustainable model based on lies and eventually requiring “wholesale” default?

July 4th, 2015 at 4:34 am PDT

link

Very well written explanation. Thank you

July 4th, 2015 at 4:45 am PDT

link

[…] (Reuters) • Angela’s Ashes: How Merkel Failed Greece and Europe (Spiegel) • Greece (Steve Randy Waldman) • Greek Mass Psychology Of Revolt Will Survive Financial Carpet-Bombing (Mason) • Greek […]

July 4th, 2015 at 4:51 am PDT

link

Thank you for this excellent summary. As a non-economist and EU supporter, I’ve been sadly reaching these same conclusions over the past few months. One other thing:- 1) Banks crash the economy 2)states impose austerity 3)voters elect Fascist governments – isn’t that how it went last time? What is likely to happen with Golden Dawn in subsequent elections in Greece if Syriza is brought down?

July 4th, 2015 at 5:34 am PDT

link

out-fucking-standing.

July 4th, 2015 at 5:53 am PDT

link

[…] http://www.interfluidity.com/v2/5965.html […]

July 4th, 2015 at 6:11 am PDT

link

A great post. Thank you very much for writing it.

July 4th, 2015 at 6:23 am PDT

link

In 2010, the EU, ECB, and IMF laundered a bailout of mostly French and German banks through the Greek fisc. Cash flowed into Greece only so it could flow out to rickety banks. Now, suddenly, the banks were absolved. There were very few bad loans left on the books of European lenders, everyone was clean, no bad actors at all…That is, Greece’s citizens are in precisely the place France’s citizens and Germany’s citizens were in 2010, at risk that personal savings maintained as bank deposits will not be repaid. Something was worked out for French and German citizens.

I don’t see how this is even close to a fair representation of the 2010-2012 Greek debt restructuring. 199.2b EUR of Greek debt was exchanged for 29.7b notes and 62.4b new Greek bonds. This was a 52% write-down, only using par value, except the new bonds were not valued worth par, because the new coupon was way below market. After the exchange, the new bonds traded at ~25c of new par and 6c of original par. When the EFSF later repurchased bonds from private owners, it paid 11.3b to retire 31.9b of debt. That is, 34c of the new par value of the bonds, or 17c of original par. Including the haircut on the aforementioned notes (which were EFSF notes and worth new par), private creditors ended up with about 25c on the dollar of what they lent. This is not “cash flowing into Greece so it could flow out to rickety banks.” It is the exact opposite. A near complete sovereign wipeout borne by private lenders.

Who took these writedowns?

Paribas, Commerzbank, Dexia, SocGen, RBS, Unicredit, Groupama, HSBC, Metlife, Allianz, Axa, DB, ING, Generali and many more all wrote down and realized losses on between 60-80% of what they lent to Greece. It’s true that some of these banks got liquidity support during the Euro crisis, but the Greek write-downs were ultimately born by the stakeholders of these banks.

In fact, the only banks that were directly bailed out with respect to the Greek debt restructuring were the Greek banks. The largest holders of Greek debt were Greek banks. They were the only institutions who were undoubtedly doomed as a result of losses in the value of Greece’s sovereign dooms, and the stakeholders in those banks, especially depositors were blatantly saved. National Bank of Greece held 13.7b. Piraeus held 9.4b. Alpha held 3.7b. The capital injections, initially 23b euros, meant that Greek depositors were protected from what would otherwise have been inevitable losses due to enormous domestic bank holdings in Greek debt. Foreign banks and private holders actually took losses.

July 4th, 2015 at 7:09 am PDT

link

Outstanding summary!

Some have suggested that the troika’s current motivation with regards to Greece is to keep the likes of Portugal and Italy in line in the future. But, what lessons will be learned from this episode? If another, larger Southern European state progresses towards failure, will they accede to European elite demands for a prolonged program of austerity and bailouts permitting time to make private creditors whole. Or, will such states default upfront imposing losses on private, wealthy creditors? If the last five years events are viewed objectively, the latter seems the better course of action. I doubt this is the lesson that the Troika hoped to teach.

July 4th, 2015 at 7:32 am PDT

link

The apologists for the creditors are acting quite shamefully. Facts are facts. And of course they’re the same people who blame the victims. And the victims are standing up for supposed European ideals!

As Krugman wrote in his latest column, European austerity is failing across the continent. A No vote may serve as a wakeup call to the elite but I doubt it. It will take growing grassroots opposition across Spain, Italy and then finally in France and Germany etc.

My hope is that Greece votes No. They’ll probably be pushed out. J.W. Mason has some interesting thoughts on what to do if the ECB cuts the chord.

http://jwmason.org/slackwire/what-greece-must-do/

July 4th, 2015 at 7:51 am PDT

link

I do not get the infatuation and obsession of some posters about Germany. The Greek default affects everyone in the Eurozone pretty much equally. Spaniards and Italians may not be so much aware of this, but their taxmoney goes to Greece just as that of German taxpayers. Oh yes, austerity: WTF is that all about ? Persistently spending more than you earn and then obliging others (the Germans, the ECB, the IMF, the Russians, the Chinese, whoever) to bail you out – and if they don’t calling them terrorists (or Nazis) is very much what I would call the Mediterranean Disease. I’d rather live with “austerity” than being afflicted with that disease. Check out Germany”s economic growth and unemployment rates – then you know what the better concept is.

July 4th, 2015 at 8:08 am PDT

link

I agree with all of this, though I can’t rise to the level of anger (and I appreciate it) because I think I’d boil over and start breaking things.

I’d only add that the corrupt elites were not only overspending, but they were involved in vendor finance scams. Hundreds of millions in bribes on some single deals. The credit came through to sign the contracts, and the bribes were rolled into the contracts. On one deal alone, Siemens, you had the Greek defense minister take hundreds of millions to approve a tens of billions deal. He is in jail, so are members of his family, but then there are 64 others being prosecuted as well for this one deal. Think about it, hundreds of millions spread to 64 people (who probably doled out more themselves).

The flip side to this is to look at Europe and say, not only were the banks short-term or medium-term in terms of outlook, but actually they were embroiled with multinationals in host countries. The CEO of Siemens sits on the board of Deutsche Bank. I’m not saying there is a quid pro quo, no one has shown any proof of that, yet when a huge contract is signed between Greece and a company like Siemens everyone knows the money will be there to fund it. It comes close to a vendor finance scam. Heck, the Germans were willing to lend Greece money in 2010 to complete a frigate and submarine deal.

I am also glad that someone pointed out finally that the Goldman deal with Greece was known by all, completed by many, and approved by the legal teams at Eurostat (though Gustav Piga reviled such deals). Not only that, but Greece was well under the budget deficit threshold, it was at 1.4% before the deal. The deal hid Greece’s debt to GDP, however, and reduced it from 107% to 104%. The question is, did this reduction fool anyone? If it hadn’t been done, would Greece have been disqualified? Remember, Belgium at the time had a higher debt to GDP, and it was trying to enter as well.

There is no doubt Greece was not fit for the eurozone (I am not sure that Spain or Portugal are fit either, they are losing lots of companies) but to say Greece is not fit is not the same thing as saying that fitness depends on your balance sheet (as hidden or rooked as it may be). My take is that the balance sheet was adequate for entry at the time, but that the country’s competitiveness was very poor, and it could never survive.

July 4th, 2015 at 8:25 am PDT

link

“That is why responsibility for, and the consequences of, extending credit badly must fall upon creditors, not debtors.”

This is the most twisted logic I’ve seen in a while. It basically promotes to go borrow money, not paying it back and blaming the creditor for not foreseeing our unwillingness to repay or, to shoot someone and blame the gunshop and the NRA for letting us have a gun. Utter bull….

July 4th, 2015 at 8:39 am PDT

link

The Eurocrats are caught in a ‘credibility trap.’

So are their counterparts in the US and the UK, who have committed policy errors of a far greater magnitude. They are merely more adept (ruthless?) at covering it up and delaying, thanks to far greater political control over their own areas, and more practice.

The reckoning will go rolling on.

July 4th, 2015 at 8:51 am PDT

link

Excellent indeed Randster

One at this point has to see the need for a big fat Greek “NO! ”

Syriza is a loose outfit

But so are most popular self organizations

My Leninist comrades could have done more to support this trial of democracy

But it would seem hunkering on the margin is easier

July 4th, 2015 at 9:05 am PDT

link

[…] • Greece (Steve Randy Waldman) […]

July 4th, 2015 at 10:02 am PDT

link

[…] • Greece (Steve Randy Waldman) […]

July 4th, 2015 at 10:05 am PDT

link

It is human nature to blame others for one’s own shortcomings. Understandable, but unproductive, and progress is only possible when one comes to terms with them. Perhaps this is the start to that.

July 4th, 2015 at 10:41 am PDT

link

[…] • Greece (Steve Randy Waldman) […]

July 4th, 2015 at 10:59 am PDT

link

“We get to choose which morality tale we most use to make sense of the world. We do, and surely should, use both to some degree.”

Yes to the latter.

It’s only binary under ideological extremism and intransigent positioning.

Hence negotiation.

July 4th, 2015 at 11:42 am PDT

link

Laohu writes:

“That is why responsibility for, and the consequences of, extending credit badly must fall upon creditors, not debtors.”

This is the most twisted logic I’ve seen in a while. It basically promotes to go borrow money, not paying it back and blaming the creditor for not foreseeing our unwillingness to repay or, to shoot someone and blame the gunshop and the NRA for letting us have a gun. Utter bull….

And yet that is how the real world works. Creditors do not lend out of the goodness of their hearts, they lend because they wish to make money off of rent (interest). In exchange, they assume some risk that the rent, or even some or all of the principal, will not be repaid. A wise creditor assesses this risk as accurately as possible and only extends credit when the return (the rent) is high enough to compensate for that risk. If the borrower defaults… well, that was a foreseeable risk.

Borrowers of course should also assume some consequence. That is what credit ratings are for – if you fail to repay your loans on time, creditors share that information and you are viewed as a higher risk, and thus must pay higher interest to compensate for that risk. But this is what the author suggests regarding Greece’s credit rating.

What should not be done is to allow the hammer of the State to fall on the borrower. Although creditors may not like it, the risk of default was part of the deal. If a default happens and their risk-compensation turned out to be inadequate to cover their losses, they have only themselves to blame.

July 4th, 2015 at 11:46 am PDT

link

“A wise creditor assesses this risk as accurately as possible and only extends credit when the return (the rent) is high enough to compensate for that risk. If the borrower defaults… well, that was a foreseeable risk… if a default happens and their risk-compensation turned out to be inadequate to cover their losses, they have only themselves to blame.”

Now that’s the better way to look at this.

July 4th, 2015 at 11:57 am PDT

link

First: all this talk about the details of how actual banks actually work? Anyone who accuses you of being an econoblogger is a shameful liar. There is far too much knowledge and far too little theory here for that awful slander.

Second: what is it about these situations that makes people fail to understand the meaning of the words that come out of their mouths. I mean, if somebody who went to a state university in the 50s or 60s calls themselves a “self-made man”, they are a douchebag, but only because the fact is that state university educations cost the equivalent of a summer at a minimum wage job in the 50s and the 60s thanks to taxes paid by a lot of workers who didn’t go to college and whose kids didn’t go to college.

But what on earth is going on with folks like the German public or commenters 23 and 25 above. “Persistently spending more than you earn and…” This is supposed to be a great sin. But the meaning of the words quoted is literally synonomous with the term “borrowing money.” The words used to demonize Greece, or the people in this country who ended up with underwater mortgages, are words that litterally mean “borrowers.” And these words are tossed about by people who live in houses that are mortgaged or, worse, who run companies that don’t build things, that don’t use tools, companies whose main activity is “leveraging this to do that”. “Leverage”! The meaning of the word is synonymous with the epithet you lob at Greece. How do you avoid the cognitive dissonance?

July 4th, 2015 at 12:39 pm PDT

link

Mr. Waldman, in light of your June comments: “The expansion of inequality since 1980 is a devil with many fathers. But it was not an inexorable fact of nature. It was the product of politics and policy and institutional arrangements that stripped US workers of bargaining power, and stripped US capital of tax obligations and ties to community. The Fed played a role in those arrangements, and not an unimportant role.”

I was interested in your take on the following remarks by American law professor and geopolitical strategist Philip Bobbitt, who seems to be practically expressing a ‘Candidean’ (“best of all possible worlds take) on recent and current U.S. foreign policy and military interventions: ‘This fallacy indulges in the frequent, unthinking assertion that we should compare the present state of affairs with the past in order to evaluate the policies that have gotten us to where we are now. In fact, we should compare our current situation with alternative outcomes that would have arisen from different policies, had they been chosen. This is true for prospective policies as well: It is a sophist’s argument to deride a proposed policy (say, social security reform or free trade) by simply saying we will be worse off after the policy is implemented than we are now. That may well be true. But it could be true of even the wisest policy if other alternatives, including doing nothing, would make us even worse off in the future…In the same way, we should reframe fallacious prospective questions like, “Will we be better off in five years than we are now if we adopt a certain policy?” The better question to ask is, “Will we be better off in five years by adopting this policy than we will be in five years if we do not?’

Implying that things might look bad, while in truth all other options available to America’s sagacious and farseeing policy elites were/would have most likely resulted in even worse outcomes: so in, essence, Iraq, Libya, Syria, one can be fairly sure were the best of all possible outcomes. Meaning that, in this analytical light, your comments cited above would need to be reevaluated as being not mistakes or elite indifference or iniquity towards the rest of society, but as intended to be the best of all possible outcomes for the nation and state as a whole considering all other epistemologically available and actually implementable outcomes. Can America’s foreign policy elite actually be thinking and acting under such conceptions?

https://www.stratfor.com/weekly/strategy-real-time-dueling-enemy-moves

July 4th, 2015 at 12:39 pm PDT

link

>not the current, much maligned Syriza, but decades of its predecessors — treated the state like a teat from which clients and friends of electoral victors might suck.

Why not Syriza? The very first thing they did was to give their clients at the DEH union a raise. A Syriza MP made a speech in parliament saying that ERT (the government TV channel) should be opened again in order to reward the people who helped get Syriza elected. Loads of people in top places have been getting their relatives appointed to other top places. The idea that Syriza represents a break from the corruption and clientism of the past is simply false.

After all the people who voted Syriza are those who benefit from these arrangements in the first place; it would be weird if their party suddenly went against them.

July 4th, 2015 at 12:40 pm PDT

link

>But we have had five years to observe creditors’ tender ministrations, under governments that complied with creditors’ every demand.

This is false. The Greek governments agreed to all sorts of things, yes. They just never did what they said they were going to do. 99% of those were growth-inducing reforms: decreasing red tape, various measures aimed at attracting FDI, liberalization of closed professions (which is all of them), liberalization of various markets, fixing the tax system, regulations to control cartels, getting rid of state enterprises losing hundreds of millions every year, the list goes on and on. NOTHING was actually implemented.

I challenge you, go through this list of planned reforms from 2010 and make a list of which ones were actually implemented: http://ec.europa.eu/economy_finance/publications/occasional_paper/2010/pdf/ocp61_en.pdf

It will be a very, very short list.

July 4th, 2015 at 12:54 pm PDT

link

You do realize you’re just advocating a massive bailout of a different set of creditors? On a balance sheet, a bank deposit is a loan to the bank, and the holder of a bank deposit is a creditor of the bank. Every argument you make about creditors’ responsibilities and risks applies directly to Greek bank depositors . . . but you just happen to personally favor that class of creditors over the others. Why are you pretending that there’s some obvious moral argument in bailing out one particular favored-by-you class of creditors at 100% while other creditors are handed a massive loss?

July 4th, 2015 at 1:06 pm PDT

link

dsquared writes:

“The 2010 transaction wasn’t a “laundered” bailout of French and German banks. Dig into the numbers. It was a bailout of Greek banks, two of the biggest of which (Geniki and Emporiki) were owned by French parents. If that bailout hadn’t happened, CA and SG would simply have allowed their subsidiaries to fail, and limited their losses to the equity. Greek depositors, on the other hand, would have lost everything (and I mean everything – the Greek deposit insurance fund is laughably small).”

As opposed to now, when they’ve undergone years of depression, and will likely suffer something similar?

July 4th, 2015 at 1:11 pm PDT

link

This text is wholly bizarre. Mostly because of the moral hazard bit and its incidence upon lenders or borrowers.

Is the author aware that the Greeks already benefited from one of the biggest haircuts in the entire history of mankind? In 2012, private lenders took a 50% loss on their Greek debt. Even though they were deceived by a Greek government that was cooking the books.

Nowadays, the creditors are others – they’re the taxpayers of other Eurozone countries (plus the IMF). Applying his rationale, it seems the author’s intention is to discourage those creditors from keep borrowing money to countries like Greece. Chief amongst them, Greece itself, of course.

The entire thing is so illogical it’s hard to comment on it.

As for the GDP chart, it’s misleading to say the least. I’d strongly suggest to extend the x axis to 2001, the year the euro started. And better yet, use indicators like consumption and labor costs along GDP. That would paint a much better picture.

July 4th, 2015 at 1:57 pm PDT

link

Excellent piece of work! It would be nice to edit it to reduce the lenght significantly so that more people read the whole thing.

July 4th, 2015 at 2:45 pm PDT

link

This is a great piece of work, and I appreciate it all to hell.

I do have a nit to pick, though. You write, “Having recast a crisis caused by a combustible mix of regulatory failure and elite venality into a morality play about profligate Greeks who must be punished, Eurocrats are now engaged in what might be described as ‘loan-shark theater’.” No, Angela Merkel, at least, really believes. Probably Wolfgang Schäuble does too.

July 4th, 2015 at 4:04 pm PDT

link

What a fucking joke of an article.

July 4th, 2015 at 4:44 pm PDT

link

[…] They were enticed into the eurozone by what turned out to be fantasy promises by an institution whose architecture was pretty much designed to fail. European bureaucrats, Greek politicians, and French and German bankers were well aware that Greece was a risky proposition, but they were willing to look the other way because there was money to be made: […]

July 4th, 2015 at 4:47 pm PDT

link

I’m curious about why you disagree with the argument that the creditors are actually not so much interested in getting back their money but in keeping leverage over the government to enact reforms. You say that this cannot be the case, because as creditors their incentive is not the long-term good of the nation, but only their short-term recovery of the debt. I don’t think this is necessarily true.

In the end, the goal of the EU should be (I hope) to allow Greece to become a prosperous nation with a sustainable economy, to form a stronger union overall. Whether or not the actual debt ever gets fully repaid should be secondary to that. So aren’t the incentives in this case, unlike for corporate debt, actually quite well-aligned?

The idea that the creditors do not want to give up all their leverage (the debt) makes perfect sense to me. The Greek government has shown time and time again that it is unable to enact the reforms it needs to. Properly reforming the political structures and getting rid of clientelism and waste is going to require some external factor forcing them to act.

July 4th, 2015 at 4:49 pm PDT

link

An outstanding paper – so many facets of importance covered here.

July 4th, 2015 at 4:49 pm PDT

link

Superb article. Thank you.

July 4th, 2015 at 4:50 pm PDT

link

Playing the role of the “after Christ prophet” is so easy and intriguing as much as writing a history novel and anyway you can’t. fail in your conclusions. But not everyone knew or was sceptic 10 years ago as you imply because everyone was making huge profits from Greece

July 4th, 2015 at 5:36 pm PDT

link

One thing to note: a big driver of the desire to lend by German banks was the trade surplus that Germany kept running with the rest of the Eurozone. Euros accumulating in Germany had to go somewhere, else the trading partners would not have the money to keep buying so many German goods.

July 4th, 2015 at 6:44 pm PDT

link

I find it amazing that the meme is “lenders lent and fully understood the risk of default” and now should take it on the nose.

Yes they did know. But something else that was understood was ” and in the event of default becoming probable, would use all legal means and make it as unpleasant as possible before and after default”.

The interest rate on a loan always has a lot of information: collateral, legal institutions to enforce the loan, collateral, bankruptcy rules etc.

Does any one borrowing money from a loan shark ever seriously think the kneecapping is not part of the deal?

July 4th, 2015 at 6:54 pm PDT

link

I find it amazing that the meme is “lenders lent and fully understood the risk of default” and now should take it on the nose.

Yes they did know. But something else that was understood was ” and in the event of default becoming probable, would use all legal means and make it as unpleasant as possible before and after default”.

The interest rate on a loan always hides a lot of information: collateral, legal institutions to enforce the loan, collateral, bankruptcy rules etc.

Does any one borrowing money from a loan shark ever seriously think the kneecapping is not part of the deal?

July 4th, 2015 at 6:55 pm PDT

link

Kneecapping should not be part of the deal because kneecapping is morally abhorrent. Both sides share the blame for a default, but only the kneecappers can be blamed for the kneecapping.

July 4th, 2015 at 7:05 pm PDT

link

This article highlights significant factors beyond the problem of a greek default.

Modern financial institutions, economists for many decades, seem to see something akin to vitrue

In money itself or the act of investment. They do this missing the point that virtue is only

Inherent to the individual person. Absolved of guilt, any marginilised entity is to blame for

It’s problems but never the entities that marginilised them in the first place.the innocent must

Always be punished for the sins of the guilty.

I hope this article becomes widely read and i am grateful to the author for his insight.

July 4th, 2015 at 7:34 pm PDT

link

@dsquared : CA and SG could not just have written off their equity a let their subsidiary go down for two reasons :

A) they were probably the main source of funding of their subsidiary in money markets and they would have lost on that two

B) other international counterparties where relying on the CA and SG “brand names” to expect support from the parent as long as it was a majority shareholder. If CA and SG went short of that expectation, they would have cut themselves on all local funding for any subsidiary they have in the whole world. It would have essentially meant the closure of their investment banking franchise worldwide and dumping their derivatives book at the worst moment.

@dlr :

A) you seem to forget that for years, Banks pocketed the carry on a fat coupon in Greece and rode the convergence trade. Their so-called “losses” was only giving back illegitimate gains

B) French banks were exposed to 52bln Greek Debt in March 2010 (see http://blogs.cfr.org/geographics/2015/07/02/greecefallout/) , now practically nothing. If your computation was true, we should have seen 75%*52 = 39bln euros loss from Greece in the French Banking system. I guess we would have heard of it…

July 4th, 2015 at 7:39 pm PDT

link

Am I the only commenter who finds this post to be trivially reasoned? It’s an impassioned post about values and perspective, but the core seems to be a name-calling exercise. That is totally fine if the name-calling results offers clarity. But call an asshole an asshole… then what?

July 4th, 2015 at 8:27 pm PDT

link

Am I the only commenter who finds this post to be trivially reasoned? It’s an impassioned post about values and perspective, but the core seems to be a name-calling exercise. That is totally fine if the name-calling offers improved clarity. But call an asshole an asshole… then what?

July 4th, 2015 at 8:27 pm PDT

link

John C @4:44: What a fucking joke of a comment.

“Am I the only commenter who finds this post to be trivially reasoned? It’s an impassioned post about values and perspective, but the core seems to be a name-calling exercise. That is totally fine if the name-calling offers improved clarity. But call an asshole an asshole… then what?”

I’d suggest that it is trying to reverse what has thus far devolved into a name-calling exercise. The Greek state/people are being derided as profligate wastrels, and as a result are now being asked to bear the full brunt of loans that should never have been made. Merkel et al refuse to accept the EU’s own role in that transaction – an irresponsible debtor requires an irresponsible creditor. Irresponsible creditors usually end up taking a haircut. On smaller scale we have things like bankruptcy courts for situations precisely like this one. The IMF can’t do the nation-state equivalent of repo-ing Tsipras’ motorcycle, but one does not loan money to a sovereign ignorant of that.

It’s no secret that Greece was a corrupt and poorly governed basket case for most of its history. Expecting it to reverse course and transform into Austria just because it got a new currency was the height of wishful thinking. (Then again, so was expecting Iraq to become a stable democracy c. 2003 – but I digress.)

I also take issue with any suggestion that the suggested reforms will somehow “improve” Greece. They might, someday, but not before the political system collapses and/or elects someone truly frightening. Economics does not happen in a vacuum.

July 4th, 2015 at 9:21 pm PDT

link

[…] has an excellent post on Greece and I don’t wish to repeat what he’s written much more fluently than I could. […]

July 4th, 2015 at 9:42 pm PDT

link

I think solving the problems of the modern world requires, inter alia, reverse engineering the psychology of Reagan/Thatcher/Neoclasicalism. Comment threads like this one are instructive for that task. One facinating thing is that the believers seem unable to track a moral argument based on facts of economic reality. For some, the moral reasoning reads as “name calling.” Others recognize the language of moral discourse, but find the claim “sometimes the moral outcome is for borrowers to fail to pay back creditors” to be inscrutable nonsense, somehow failing to see that this would imply requiring Lehman shareholders to forfeit their Social Security checks back to American taxpayers (after first auctioning their kidneys on eBay).

The long series here on the thinly veiled moral nature of “objective” welfare economics was, perhaps, SRW’s attempt to meet these folks halfway. But I don’t think it can be done. They can’t really comprehend the sentences, let alone be persuaded.

July 5th, 2015 at 12:06 am PDT

link

[…] and the economy is already nosediving. To me, it’s all incomprehensible, even after reading interfluidity about the stupidity of this all and this zerohedge post about the super seniority of IMF debts […]

July 5th, 2015 at 12:33 am PDT

link

“Including the haircut on the aforementioned notes (which were EFSF notes and worth new par), private creditors ended up with about 25c on the dollar of what they lent. This is not “cash flowing into Greece so it could flow out to rickety banks.” ”

Which is still money flowing into Greece to flow out again to rickety banks … it was certainly more than what the debt was worth, as evidenced by the IMF analysis of inability of Greece to pay the obligations taken on by the previous Greek government.

It certainly would have been a happier bail-out for the rickety German banks if they had received face value, but they received substantially more from their bail-out via Greece as a conduit than a prudent lender would have had any expectation of receiving.

25% of their face value, perhaps, but in the circumstances, debt from a sub-sovereign state in a similar financial position without a prospect of being bailed out by their economic sovereign state was worth much less than 25% of their face value, since the 25% bail-out

. Such reckless creditors lending to such a feckless borrower as the successive conservative Greek government, that were no longer in control of a sovereign economy, would not have justification for complaint if they had ended up with 10% of the face value, as

July 5th, 2015 at 1:05 am PDT

link

This idea of united Europe is nonsense. Cultural differences and differences in how societys work among Northern and Southern Europe are too big. Euro is just one big problem.

July 5th, 2015 at 1:21 am PDT

link

«It is difficult to overstate how deeply Europe’s leaders betrayed the ideals of European integration in their handing of the Greek crisis. The first and most fundamental goal of European integration was to blur the lines of national feeling and interest through commerce and interdependence, in order to prevent the fractures along ethnonational lines that made a charnel house of the continent, twice. That is the first thing, the main rule, that anyone who claims to represent the European project must abide: We solve problems as Europeans together, not as nations in conflict.»

Indeed Europe is working like that: the EU is still paying around €5 billion a year of free money for agricultural and regional support to Greece, mostly paid for by german taxpayers, and when votes on the greek negotiations come up usually the consensus includes *all* country governments save that of Greece. That to me looks like “solve problems as Europeans together”. That’s 18 government, all democratically elected, and standing for re-election, with different political backgrounds and very different countries, agreeing as «Europeans together, not as nations in conflict» as to EU policy with Greece.

«leaders gloated and took credit for a phantom prosperity. When the levee broke, instead of acknowledging errors and working to address them as a community, Europe’s elites — its politicians and civil servants, its bankers and financiers — deflected the blame in the worst possible way. They turned a systemic problem of financial architecture into a dispute between European nations. They brought back the very ghosts their predecessors spent half a century trying to dispell. Shame. Shame. Shame. Shame.»

Shame on you for accusing Europe’s leaders, and not Greece’s leaders, of betraying the european project. What you have written is a vile and baseless accusations, as someone wrote just name calling, something from a cesspit full of malice and delusions.

It is Greece’s leader who «gloated and took credit for a phantom prosperity», it is Greece’s leaders who «deflected the blame in the worst possible way» onto their very generous creditors, it is Greece’s leaders, in particular SYRIZA, who «turned a systemic problem of financial architecture into a dispute between European nations» and then who in a despicable and vile way «brought back the very ghosts their predecessors spent half a century trying to dispell» by resurrecting WW2 stories with Germany, and their only goal was simply to extract even more free cash from their creditors, trading a cruel history for money.

The greek story is beautifully summarized in these two graphs, the first abouty GDP:

https://rwer.wordpress.com/2015/07/01/gdp-in-emerging-europe-worse-than-you-think/

Here greek GDP before SYRIZA, in 2014, was at the same level as in 2000. Was Greece in a catastrophically poor state in 2000? If it was, why where not accusing european leaders of betrying the european project then? Also, greek GDP-per-capita in 2014 was still higher than that of 7 other EU members, and in parrticular 50% higher than that of Bulgaria. Why are you not accusing european leaders of betraying the european project over the poverty of those 7 countries, a much bigger tragedy than Greece’s?

The second is about imports:

https://rwer.wordpress.com/2015/07/03/lose-lose-in-greece/

It is pretty clear that most if not all of the growth in greek GDP between 2000 and 2008 was due to an epic, amazing boom in imports fueled by an epic, amazing boom in debt. This was a choice by the greek government and greek voters, democratically reached in several elections. Debts come due, and they have to be repaid or defaulted upon, and both courses have huge costs. Note also that imports continued at a very high level in the first three years of “austerity”, 2008-2011. So much for “austerity”.

«Until the financial crisis, people like, well, me, were of two minds about the EU’s famous “democracy deficit”.»

The democratic deficit is that today there is no referendum in Germany and the other 17 EU countries to which Greece wants to sell worthless greek bonds at face value as to whether EU citizens want to buy those bonds.

Today, if there was real democracy in the EU, german citizens would also be voting YES or NO as to whether to accept SYRIZA’s best offer. It is pretty certain that they would vote NO.

But do the greek government and the delusionary/resolutionary fractions of the left care about democracy *in Germany*? Of course not! German voters don’t matter. All that matters is that the german government force them to finance the re-election campaign of a greek government made of loveable, stylish, talk-the-talk “leaders”.

July 5th, 2015 at 2:59 am PDT

link

Outstanding.

July 5th, 2015 at 3:01 am PDT

link

Just wondering: are you planning on amending the factual inaccuracies in the article, or at least alerting your readers about them? It’s starting to feel like you wrote this piece in bad faith.

July 5th, 2015 at 3:24 am PDT

link

[…] people, but the place is plainly pretty fucked up. It has been fucked up that way for a long time (Interfluidity) • 15 Problems With Real World Portfolios (A Wealth of Common Sense) • 5 biggest financial […]

July 5th, 2015 at 4:30 am PDT

link

[…] Interfluidity (see […]

July 5th, 2015 at 4:52 am PDT

link

«For some, the moral reasoning reads as “name calling.” Others recognize the language of moral discourse, but find the claim “sometimes the moral outcome is for borrowers to fail to pay back creditors” to be inscrutable nonsense,»

For me this talk about “moral outcome” is buffooneering nonsense indeed *in *these circumstances*, for several reasons:

* “sometimes the moral outcome is for borrowers to fail to pay back creditors” is an appalling example of buffooneering because default is not a moral decision, it is simply a business decision. Bankruptcy is a business practice, not a moral stance. Perhaps it is a moral stance when there are “odious debts”, but all greek debts were taken by democratically elected governments, which were re-elected as they delivered the debt-fueled “pork”, and were given by banks subject to the policies of democratically elected governments, without any coercion. The greeks used that borrowed money to have a big fat greek party of consumer imports, which boomed in parallel with greek debt. It is entirely their right to default on their debts, and let others pay for that huge party, but it is not a “moral” decision, it is a business one.

* The issue at stake is not even really default: the other 18 EU countries know very well that greece will never pay back their debts in full. The issue is whether the costs of bankruptcy fall on greek taxpayers or rest-of-EU (mostly german) taxpayers, that is who pays for the cost of rolling over indefinitely the never-to-be-repaid majority of greek debt. Greek citizens have enough savings in Greece and mostly in Switzerland that they could absorb those costs, but SYRIZA wants those costs to be paid for by citizens of other EU countries, including those of the 7 countries with a loser GDP per person than Greece.

* For the past 35 years, since Greece joined the EU in 1981, the greek government has received a largish net contribution from richer EU countries, and this has continued. Recently Greece got around €5 billion a year, amounting to 2-3% of GNI, which is quite significant compared to the 4-5% of GNI that greek taxpayers give to the greek government in income taxes. In addition to this since the crisis began the creditors have been rolling over bankrupt greek debt at face value, effectively giving Greece free default insurance, and before SYRIZA came to power greek debt default insurance cost a 20% premium per year, which means that creditor were effectively donating a few dozen billion euros of free default insurance to Greece every year since 2008.

* There are 7 countries in the EU that have a lower GDP-per-person than Greece. In particular greek GDP-per-head is 50% higher even now than in Bulgaria, and desperate bulgarians emigrate in large numbers to Greece even now, where they are often exploited and abused by the much richer greeks. If there was any moral depth to those who argue for immense handouts to Greece, they would instead have been arguing for years for huge handouts to Bulgaria and those other 6 countries, because their situation is much worse. To me it is gross and immoral buffooneering to make a lot of fuss about Greece and none about Bulgaria.

July 5th, 2015 at 5:05 am PDT

link

“Blissex: The issue at stake is not even really default: the other 18 EU countries know very well that greece will never pay back their debts in full. The issue is whether the costs of bankruptcy fall on greek taxpayers or rest-of-EU (mostly german) taxpayers, that is who pays for the cost of rolling over indefinitely the never-to-be-repaid majority of greek debt.”

Clearly the issue at stake is NOT that, or else the Eurogroup would have allowed the taxation of higher income Greeks to be part of the reforms. Going beyond dictating not only a level of primary surplus to specifying that the primary surplus must be achieved by raising VAT and cutting pensions but not by increasing taxes on wealthy Greeks is only a decision of whether the cost should fall on Greek taxpayers in the sense that after decades of clientlism, the wealthy of Greece expect to have to pay relatively little tax.

July 5th, 2015 at 5:23 am PDT

link

A) you seem to forget that for years, Banks pocketed the carry on a fat coupon in Greece and rode the convergence trade. Their so-called “losses” was only giving back illegitimate gains

That is an interesting argument, to say the least. So they actually made really smart loans because those juicy coupons offset their “so-called losses?” Everybody wins!

B) French banks were exposed to 52bln Greek Debt in March 2010 (see http://blogs.cfr.org/geographics/2015/07/02/greecefallout/) , now practically nothing. If your computation was true, we should have seen 75%*52 = 39bln euros loss from Greece in the French Banking system. I guess we would have heard of it…

This information in the link is completely wrong, though it has been repeated a few times in blogs and media articles and seems to have been generated by a very poorly researched BIS note. Go back and look at the disclosures for SocGen, Paribas etc or any of the good research at the time. Paribas had 5b GGB in May 2010 which it still had in 2011 when it started to write it down, first by the 52% haircut and against to realize additional losses. SocGen had $3b which also didn’t decline materially into 2011 when they started writing it down. Natixis had almost none.

July 5th, 2015 at 5:47 am PDT

link

«”The issue is whether the costs of bankruptcy fall on greek taxpayers or rest-of-EU (mostly german) taxpayers, that is who pays for the cost of rolling over indefinitely the never-to-be-repaid majority of greek debt.”

Clearly the issue at stake is NOT that, or else the Eurogroup would have allowed the taxation of higher income Greeks to be part of the reforms.»

In fact they *demanded* that, and the german government even offered SYRIZA to send to Greece 500 tax inspectors at Germany’s expense. SYRIZA of course refused — they want to have a chance of winning the next elections.

And the “institutions” have not forbidden SYRIZA from taxing wealthy greeks, at any point. If SYRIZA had wanted they would have raised a land tax or whatever as soon as they got into government.

But why did they not do that? Because they want to be re-elected, and they are re-elected by greek tax evaders, not by german tax payers.

«specifying that the primary surplus must be achieved by raising VAT and cutting pensions but not by increasing taxes on wealthy Greeks»

But SYRIZA never proposed to increase taxes on wealthy greeks, they only *talked* about it. Note that SYRIZA seems to many people, including me, to be negotiating in bad faith. They could well be promising to raise taxes in greek in the future, expecting very well to be unwilling to actually make that happen.

Someone posted a link to SYRIZA’s proposal, and it included a once-only increase in tax on profits of greek companies with sales larger than €500,000 which is of course a joke because very few greek companies report their sales and profits honestly, and very few of them would in the current circumstances have any profits even if their tax statements were honest.

Then there is a the bigger issue of whether, even if SYRIZA wanted to make it happen, a greek government would be *capable* of taxing higher income greek voters. SYRIZA have certainly never published a credible plan (or any plan) on this, and the only obvious relatively quickly and safe way of doing it, a wealth tax on land, has carefully never even been mentioned.

I personally think that there are small chances that SYRIZA would want to actually increase taxes on wealthy greeks, and even if they wanted, that the chances of the greek government being able to do so are close to zero. Obviously the “institutions” think the same, and that the chances of increasing tax collection in Greece are imaginary, and the only way forward is to cut spending, as that is something that can be done and measured.

July 5th, 2015 at 5:52 am PDT

link

[…] interfluidity » Greece – Greece is a remarkable country full of wonderful people, but along dimensions of development and governance, the place is plainly pretty fucked up. It has been… […]

July 5th, 2015 at 6:01 am PDT

link

“Blissex: And the “institutions” have not forbidden SYRIZA from taxing wealthy greeks, at any point.”

But whether the “institutions” forbid it or not is beside the point if the informal Eurogroup of Eurozone finance ministers minus Greece rejects it.

“Blissex: But why did they not do that? Because they want to be re-elected, and they are re-elected by greek tax evaders, not by german tax payers.”

Credible evidence to confirm that Syriza’s primary base of support comes from wealthy Greeks is welcomed.

Indeed, credible evidence that doing as the creditors demand would ever result in sufficient economic growth to allow the current structural surplus to outweigh the cyclical deficit would also be welcomed. The graph in the piece showing the Troika’s projections of Greek GDP growth versus reality strongly suggests that complying with Troika’s demands is a recipe for shrinking your economy and generating a large cyclical budget deficit.

“fc writes: Does any one borrowing money from a loan shark ever seriously think the kneecapping is not part of the deal?”

If the relationship between Greece and the Eurogroup is presumed to be equivalent to the one between loan sharks and the desperate borrowers with limited access to formal credit that they largely prey upon … that rather confirms the thesis of the original piece than contradicts it. That is not the way that relations between a sub-sovereign state and the sovereign issuer of its currency are operated in a well functioning monetary union.

July 5th, 2015 at 6:52 am PDT

link

Debt and private lending is the worst invention of the last 300 years. It has helped fund wars and accelerate unnatural exploitation of the the earth’s resources. http://adriankuzminski.blogspot.com/2013/09/the-ecology-of-money-debt-growth-and.html

July 5th, 2015 at 6:54 am PDT

link

Paradise Lost

We stand today 05.07.2015 several hours before the completion of the national referendum in Greece about accepting further cuts from the European Union or not, and dealing with the consequences, however harsh they may be: the famous “GREXIT” being one of them.

But in the midst of the discussion about money, debt, economy, financial aid,… we lose easily perspective why the discussion became so heated. Europe was rebuild after WW2 with the premise that a Union on the state level must prevent any armed conflict, on any scale, and enable mutual growth in science, wealth and culture : a very respectable belief but a belief nonetheless. The European community grew to the Union, as belief became religion. And the European Union is more than just a economic and financial super-construct, it is in theory governed by all premises of this religion; ONE currency; free travel … There is one word for it: PARADISE.

The main emotional factor is that there may be not so small a minority, if not a majority of people who may want to leave paradise. How can anyone WANT to leave paradise? And as every religion has a monopoly on heaven and hell: you leave, and you are condemned to the fiery underground.

St. Merkel and St. Juncker guarding the gates of paradise want to have the expulsion from paradise as a weapon of last resort threatening other members who don’t and won’t behave. This weapon will lose all its awesome threatening power if a small country just leaves by itself (and gives St. Merkel the finger :) ).

Will the EU survive the GREXIT as an economical structure? YES. Will Greece to pay its debt sell itself more into slavery? NO. But will the EU survive the GREXIT as a BELIEF STRUCTURE? NOT SURE.

Greece doesn’t have money stashed somewhere in a secret hideout, so there is no money to be had. And now the question will stand like this: Will the EU risk with the exit of Greece changing its belief structure, or if you want its underlying religion.

Changing money is easy, changing an idea is easy too but changing a belief structure? For as long as humanity exists, changing a belief proved astonishingly disastrous for the belief.

July 5th, 2015 at 7:11 am PDT

link