Why is finance so complex?

Lisa Pollack at FT Alphaville mulls a question: “Why are we so good at creating complexity in finance?” The answer she comes up with is the “Flynn Effect“, basically the idea that there is an uptrend in human intelligence. Finance, in this view, gets more complex over time because financiers get smart enough to make it so.

That’s an interesting conjecture. But I don’t think it’s right at all.

Finance has always been complex. More precisely it has always been opaque, and complexity is a means of rationalizing opacity in societies that pretend to transparency. Opacity is absolutely essential to modern finance. It is a feature not a bug until we radically change the way we mobilize economic risk-bearing. The core purpose of status quo finance is to coax people into accepting risks that they would not, if fully informed, consent to bear.

Financial systems help us overcome a collective action problem. In a world of investment projects whose costs and risks are perfectly transparent, most individuals would be frightened. Real enterprise is very risky. Further, the probability of success of any one project depends upon the degree to which other projects are simultaneously underway. A budding industrialist in an agrarian society who tries to build a car factory will fail. Her peers will be unable to supply the inputs required to make the thing work. If by some miracle she gets the factory up and running, her customer-base of low capital, low productivity farm workers will be unable to afford the end product. Successful real investment does not occur via isolated projects, but in waves, forward thrusts by cohorts of optimists, most of whom crash and burn, some of whom do great things for the world and make their investors wealthy. But the winners depend upon the existence of the losers: In a world where there was no Qwest overbuilding fiber, there would have been no Amazon losing a nickel on every sale and making it up on volume. Even in the context of an astonishing tech boom, Amazon was a pretty iffy investment in 1997. It would have been an absurd investment without the growth and momentum generated by thousands of peers, some of whom fared well but most of whom did not.

One purpose of a financial system is to ensure that we are, in general, in a high-investment dynamic rather than a low-investment stasis. In the context of an investment boom, individuals can be persuaded to take direct stakes in transparently risky projects. But absent such a boom, risk-averse individuals will rationally abstain. Each project in isolation will be deemed risky and unlikely to succeed. Savers will prefer low risk projects with modest but certain returns, like storing goods and commodities. Even taking stakes in a diversified basket of risky projects will be unattractive, unless an investor believes that many other investors will simultaneously do the same.

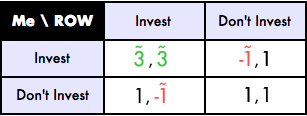

We might describe this as a game with two Nash Equilibria (“ROW” means “rest of world”):

If only everyone would invest, there’s a pretty good chance that we’d all be better off, on average our investments would succeed. But if an individual invests while the rest of the world does not, the expected outcome is a loss. (Colored values wearing tilde hats represent stochastic payoffs whose expected value is the number shown.) There are two equilibria, a good one in the upper left corner where everyone invests and, on average, succeeds, and a bad one in the bottom right where everybody hoards and stays poor. If everyone is pessimistic, we can get stuck in the bad equilibrium. Animal spirits are game theory.

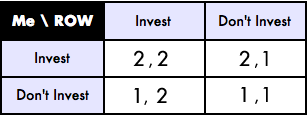

This is a core problem that finance in general and banks in particular have evolved to solve. A banking system is a superposition of fraud and genius that interposes itself between investors and entrepreneurs. It offers an alternative to risky direct investment and low return hoarding. Banks guarantee all investors a return better than hoarding, and they offer this return unconditionally, with certainty, without regard to whether other investors buy in or not. They create a new payoff matrix that looks like this:

Under this new set of payoffs, there is only one equillibrium, the good one on the upper left. Basically, the bankers promise everyone a return of 2 if they invest, so everyone invests in the banks. Since everyone has invested, the bankers can invest in real projects at sufficient scale to generate the good expected payoff of 3. The bankers keep 1 for themselves, pay their investors the promised 2, and everyone is made better off than if the bad equilibrium had obtained. Bankers make the world a more prosperous place precisely by making promises they may be unable to keep. (They’ll be unable to honor their guarantee if they fail to raise investment in sufficient scale, or if, despite sufficient scale, projects perform more poorly than expected.)

Suppose we start out in the bad equillibrium. It’s easy to overpromise, but harder to make your promises believed. Investors know that bankers don’t have a magic wealth machine, that resources put in bankers’ care are ultimately invested in the same menu of projects that each of them individually would reject. Those risk-less returns cannot, in fact, be riskless, and that’s no secret. So why is this little white fraud sometimes effective? Why do investors’ believe empty promises, and invest through banks what they would have hoarded in a world without?

Like so many good con-men, bankers make themselves believed by persuading each and every investor individually that, although someone might lose if stuff happens, it will be someone else. You’re in on the con. If something goes wrong, each and every investor is assured, there will be a bagholder, but it won’t be you. Bankers assure us of this in a bunch of different ways. First and foremost, they offer an ironclad, moneyback guarantee. You can have your money back any time you want, on demand. At the first hint of a problem, you’ll be able to get out. They tell that to everyone, without blushing at all. Second, they point to all the other people standing in front of you to take the hit if anything goes wrong. It will be the bank shareholders, or it will be the government, or bondholders, the “bank holding company”, the “stabilization fund”, whatever. There are so many deep pockets guaranteeing our bank! There will always be someone out there to take the loss. We’re not sure exactly who, but it will not be you! They tell this to everyone as well. Without blushing.

If the trail of tears were truly clear, if it were as obvious as it is in textbooks who takes what losses, banking systems would simply fail in their core task of attracting risk-averse investment to deploy in risky projects. Almost everyone who invests in a major bank believes themselves to be investing in a safe enterprise. Even the shareholders who are formally first-in-line for a loss view themselves as considerably protected. The government would never let it happen, right? Banks innovate and interconnect, swap and reinsure, guarantee and hedge, precisely so that it is not clear where losses will fall, so that each and every stakeholder of each and every entity can hold an image in their minds of some guarantor or affiliate or patsy who will take a hit before they do.

Opacity and interconnectedness among major banks is nothing new. Banks and sovereigns have always mixed it up. When there has not been public deposit insurance there have been private deposit insurers as solid and reliable as our own recent “monolines”. “Shadow banks” are nothing new under the sun, just another way of rearranging the entities and guarantees so that almost nobody believes themselves to be on the hook.

This is the business of banking. Opacity is not something that can be reformed away, because it is essential to banks’ economic function of mobilizing the risk-bearing capacity of people who, if fully informed, wouldn’t bear the risk. Societies that lack opaque, faintly fraudulent, financial systems fail to develop and prosper. Insufficient economic risks are taken to sustain growth and development. You can have opacity and an industrial economy, or you can have transparency and herd goats.

A lamentable side effect of opacity, of course, is that it enables a great deal of theft by those placed at the center of the shell game. But surely that is a small price to pay for civilization itself. No?

Nick Rowe memorably described finance as magic. The analogy I would choose is finance as placebo. Financial systems are sugar pills by which we collectively embolden ourselves to bear economic risk. As with any good placebo, we must never understand that it is just a bit of sugar. We must believe the concoction we are taking to be the product of brilliant science, the details of which we could never understand. The financial placebo peddlers make it so.

Some notes: I do think there are alternatives to goat-herding and kleptocratically opaque semi-fraudulent banking. But adopting those would require not “reform” but a wholesale reimagining of status quo finance.

Sovereign finance should be viewed simply as a form of banking. Sovereigns raise funds for unspecified purposes and promise risk-free returns they may be unable to provide in real terms. When things go wrong, bondholders think taxpayers should be on the hook, and taxpayers think bondholders should pay. As usual, everyone has a patsy, someone else was supposed to take the hit. Ex ante everyone was assured they have nothing to fear.

I have presented an overly flattering case for the status quo here. The (real!) benefits to opacity that I’ve described must be weighed against the profound, even apocalyptic social costs that obtain when the placebo fails, especially given the likelihood that placebo peddlars will continue their con long after good opportunities for investment at scale have been exhausted. By hiding real economic risks from those who ultimately bear them, status quo financial systems blunt incentives for high-quality capital allocation. We get capital allocation in bulk, but of low quality.

Update History:

- 26-Dec-2011, 10:15 a.m. EST: Flipped around a sentence: “You can have transparency and herd goats, or you can have opacity and an industrial economy.” becomes “You can have opacity and an industrial economy, or you can have transparency and herd goats.”

Your first game is J-J Rousseau’s “Staghunt” http://en.wikipedia.org/wiki/Stag_hunt

(It’s too late/early for me to give a more thought-out response.)

Merry Christmas!

December 26th, 2011 at 1:54 am PST

link

Good article. I’ve been thinking along the same lines lately.

I agree that a big part of the banks purpose is to get ordinary people to bear more risk, in addition to better risks (e.g. by credit analysis, good investment banking decisions etc).

Like you say, a lot of getting people to bear more risk is illusory. But that’s not reckless, because a lot of what is holding people back is also illusory — illusory fear. In a modern large scale society, so much of the factors of success is outside your control. The banks help mask that because they are big, have high status in society and have resources to protect their interests. So the illusion of certainty projected by the banks offset the illusory fear by the depositor.

However, if you just focus on the first part (confidence) and not the second part (improving risk selection), you run into diminishing returns and eventually negative returns. For the most part, the banks have done too good a job on masking risk and fear, and make people feel like they should win regardless of the underlying outcome. The bailout only doubles down on that concept.

So the priority is moved away from improving underlying outcomes. It’s too hard, takes too long and who knows if there’s any money to be made in it. Instead, with financial innovation, bankers focus instead on better disconnecting people’s rewards from the outcomes, so (wink) everyone can win!

You’ve sold me that transparency doesn’t solve the problem. It just pushes the problem onto the depositors when actually the banks are supposed to solve that. They pass the cost on rather than taking it themselves, which I guess is a common problem with many types of regulations.

December 26th, 2011 at 3:25 am PST

link

[…] Why is finance so complex? – interfluidity […]

December 26th, 2011 at 4:19 am PST

link

So… conglomerates? In the corporatist keiretsu/chaebol style, or the ‘New Industrial State’-Union/Business/Government antagonistic triumvirate, or semi-socialist national development bank as was popular in the 70s developing world (Singapore, etc.)? Mass financialization is a more recent phenomenon than industrialization, really; prior to that, bargaining over risks and return took place not on the market but in an overtly political arena. The whole impetus for conglomeration, etc. was to ensure that other projects would, indeed, simultaneously take place, with each entity operating its own bank to obtain funding or, if need be, bailouts at the expense of other industries in the conglomerate.

The key point in your model seems to be the requirement for coordinated investment, which no amount of risk diversification and maturity transformation alone can overcome; there must be some central actors who can monopolize enough of the residual to want a high-investment outcome and be in positions to consciously enforce it (so much for spontaneous order!). If so, then the elder Galbraith must be laughing at us from his grave.

December 26th, 2011 at 4:28 am PST

link

i get lost at the proliferation of ETFs, CDSs … Flynn effect seems appropriate

December 26th, 2011 at 6:02 am PST

link

Except people usually DO know the risks in a bubble. There was no shortage of information about crappy dot.coms but no one cared because most people are lazy and greedy.

December 26th, 2011 at 9:41 am PST

link

How much do those in finance believe their own con? For someone like me, fairly well read in general economics but not so much in finance, it seemed pretty clear that real estate was in a bubble. Prices had to drop, I just didnt know when. I think that like most people, I was unaware at the time how complex the mortgage market had become. Since I think it was obvious to most retail investors that housing prices never just go up, is the con aimed mostly at other major investors? If so, do they really believe it, or is it just a kind of Gresham’s dynamic where everyone knows it is going to go bad, but you have to go with the herd to make money? (Still a little hungover, hope this makes sense.)

Steve

December 26th, 2011 at 10:04 am PST

link

[…] Why is finance so complex? […]

December 26th, 2011 at 10:30 am PST

link

I think you and Daniel Davies would have a good time, over drinks, discussing this article.

I go with a shorter version: Complexity/Opacity is used for fraud. Gordon Notes had a good article

on how cell providers contracts use C/O to defraud their customers. The Black guy of the S&L crisis believes that C/O promotes criminological managements.

No matter. I liked your arguments.

December 26th, 2011 at 12:20 pm PST

link

In a world of investment projects whose costs and risks are perfectly transparent, most individuals would be frightened.

This strikes me as wrong. Risk aversion isn’t static, sometimes you want more risk (like when you are young) and sometimes you don’t. And sometimes the environment around you can support more risk, like if you have a strong personal or social safety net or there’s a brutal cost for failure.

On your broader point, government can also just tax and invest in stuff to solve a collective action problem. That’s why we have, say, computers and the internet. I admire your reach for intellectual counter-intuitive creativity, but the idea that one must tolerate fraud or else there could be no investment and wealth creation seems like it’s a narrow offshoot of bankrupt neoliberalism.

December 26th, 2011 at 1:07 pm PST

link

@ Nick Rowe

My solution for the stag hunt is to kill the hunter who leaps out and the rabbit, then cook & eat his flesh.

December 26th, 2011 at 1:35 pm PST

link

This is well thought out as usual but I think it misses the point. The great change in the last 30 years has been the rise of computers and global electronic trading. All these trades occurred in an earlier era but the super computer of today has replaced the back office slide rule and telephone.This expansion of technical ability has enabled an enormous expansion of the trading business, effectively creating a million or more essentially unregulated investment banks. This in turn produces a demand for increasingly complex products as people seek ways to profit from this computer power. This in turn has caused a shift from lending to trading, reducing the social benefits of credit intermediation.

We can’t abolish the computer but we can severely restrict the right of the regulated banking sector to trade or offer credit to trade these instruments; so if one hedge fund wants to sell cds to another hedge fund, fine; but JP Morgan and Citibank should stay the hell out of it.

December 26th, 2011 at 3:01 pm PST

link

[…] posted here: interfluidity » Why is finance so complex? This entry was posted in Uncategorized by admin. Bookmark the […]

December 26th, 2011 at 3:06 pm PST

link

What I am chiefly concerned about in lack of transparency is not only implications fo risk and risk-taking, but also lack of trust in institutions. The “need” for lack of transparency, ranging from opacity resulting from complexification and to mandated secrecy, betray lack of trust in the basic institutions underlying the great themes our this era, liberal democracy and free market capitalism, neither of which can exist without transparency. So is “progress” a justifiable tradeoff, or do we have to admit that “liberal democracy” and “free market capitalism” are empty slogans and the stuff of children’s stories, which do not reflect reality? It seems to me that this is close to the basis of the upheaval of the developed world is now undergoing as its principle institutions are being called into question, not only the financial sector and the Federal Reserve, but “democratic” governments subject to elite capture, and, indeed, capitalism itself as the preferred life-support system. Indeed, the revelations subsequent to the invasion of Iraq on “fixed intelligence” and the more recently the Wikileaks material shows that a great of the lack of transparency in government was for expediency rather than national security requirements. It does not seem to me that Jesuitical argument really works in any of these cases, due to unintended consequences. While such consequences may be unintended, they are not unexpected. Once truth is suppressed, illusion and hypocrisy grow. Little while lies sprout into the Big Lie.

December 26th, 2011 at 4:02 pm PST

link

This post is thought provoking but I’m not convinced that financial complexity/opacity is necessary to “con” folks into taking risks they otherwise wouldn’t. In fact, the risks of goatherding and living in agrarian societies are far greater than investing time and treasures in seemingly unproven industrial schemes. Hiding these risks aren’t necessary for investment. There have always been and will always be people willing to work/invest in the Steve Jobs-type visions of future society even when the known risks include a high probability of immediate and ignominious death.

Financial complexity is more likely motivated by the fear/reality that transparent efficient services and markets would not be particularly profitable. At least that was message I took home from my intro econ/finance courses decades ago.

I think of two opposing market forces – one which tends to make products and services efficient, transparent, competitive, trustworthy and unprofitable. The other tends to make them innovative, opaque, complex, monopolistic, deceitful and highly profitable. The latter force has dominated many industries with natural information asymmetries or “market imperfections,” including financial services and health care. Regulations are often necessary so that both forces promote profitable yet trustworthy transactions.

Following Steve’s thesis to its logical conclusion leads me to a very dark place – a moral justification for untrustworthy behavior. I’ll need a better justification before I’ll accept it.

December 26th, 2011 at 4:15 pm PST

link

On the cynical side, complexity doesn’t just hide risk. It also hides rent collection. Even for investments that are low-risk, the complexities of the process allow the middle men to drain dollars from the money flows in opaque ways. Opacity through complexity hides the information that would otherwise subject the firm to competitive pressures as unnecessarily large service charges would drive the investors to other firms with lower service charges. Financiers have a common interest in preserving opacity, because they all benefit from a system in which their clients can’t ask smart questions about where all the money is going. So maybe it’s a kind of tacit collusion.

On the more optimistic side, complexity is a by-product of the endless search for efficiency, and both are boosted by information technology. Complex algorithms executing numerous rapid financial transactions, including moving funds from one account to another, and then back again, can save a firm a lot of money I imagine by using existing funds more efficiently to leverage other transactions, and pushing everything right up against the boundaries of margin requirements, insurance requirements, reserve requirements, etc.

As the system initially becomes for efficient through complexity, though, information is gradually lost, and fewer and fewer people have a firm grasp on what is happening. And having everything right at the boundary with degraded information makes the system very fragile, and vulnerable to catastrophic effects from modest shocks.

December 26th, 2011 at 7:07 pm PST

link

I have always had the notion that when there is a lot of opacity, i.e., too little trust, people herd goats. It is in societies where people have a lots of trust, and know that laws and institutions will function the way they expect, where finance and capital markets develop.

I guess there are examples that seem to confirm the reverse, but overall, I think increasing opacity is a recipe for less finance in the future.

December 26th, 2011 at 7:55 pm PST

link

This deserves the longer version (after more mulling) but the sketch goes like this:

– The banking transaction is sublimely simple (‘the mind recoils’ sez J K Galbraith), it is the transfer of borrowed funds from the lender to a recipient as his ‘profits’: complexity is the necessary rationalization that makes these profits ‘just’.

December 26th, 2011 at 9:48 pm PST

link

[…] Source: http://www.interfluidity.com/v2/2669.html […]

December 27th, 2011 at 7:56 am PST

link

Slow down. I have absolutely no clue what banks or doing and don’t trust any of my financial intermediaries. They tell me nothing, lie, and have zero transperancy. And this is supposed to INCREASE investment???

I’ll give you a hint, this has not caused me to increase investment. I own government securities, in a variety of sovereigns and gold. Hardly risk taking.

December 27th, 2011 at 10:15 am PST

link

You do realize that you have abandoned methodological individualism? The finance sector is out to make money, not to move us to a better equilibrium. The con may miraculously be good for us. Personally, I very much doubt that.

December 27th, 2011 at 11:14 am PST

link

[…] Why is finance so complex? (Steve Randy Waldman) […]

December 27th, 2011 at 11:32 am PST

link

The point about computers, technology, and the like suggests to me that not only must banking be complex, it must continually increase its complexity. Otherwise the masses will eventually get smart enough, or at least sophisticated enough, to recognize the emperor is wearing no clothes. Continue down that path of ever-increasing complexity, and you’re headed to a Tainter moment, rather than a Minsky moment.

This is not desirable. So much so, that I’m coming around to the idea that we made a mistake when we avoided the end of the world during the fall of 2008.

December 27th, 2011 at 12:55 pm PST

link

While I agree with much of the conclusion, the argument engages in a good bit of hand-waving. Why, in a world in which crop failure or rising (or falling) gasoline prices or Wal-Mart moving to a new location can shut down an individual enterprise very easily, do we assume investors would shy away from diversifying risk by investing in a number of enterprises? Arguing that investors simply wouldn’t invest if they had an honest assessment of the risks seems contrary to what we know of actual human behavior.

Greek merchants often had little information about the risks of sending cargo abroad, but they knew the risks were high, and that their own knowledge was limited. The answer they arrived at was to put merchandise in a number of ships to diversify the risk. Pulling up stakes and moving the family west (or east, in old Russia) meant running a huge risk, and making one’s welfare dependent on decisions of lots of others over whom one had little control, but lots of folks did it. The penalty for piracy through most of human history has been death, but there was also drowning, scurvy, starvation and the like with which to contend. Even so, lots of folks chose piracy as a vocation. Why do we assume timidity on the part of modern investors in the light of what we know about risk-taking in the past?

For your story to be true, it needs to be true even if there is a considerable willingness to take risk.

December 27th, 2011 at 12:59 pm PST

link

How do taxes and inflation/deflation affect the payoff matrices?

December 27th, 2011 at 1:24 pm PST

link

Matt Stoller hits the nail on the head. Go To #10 folks.

December 27th, 2011 at 1:37 pm PST

link

@24

Yeah, I don’t get the no risk thing. I just finished reading a blog about a guy in his 20s that quit a good paying 9-5 gig to fly to Asia and try to start a new business from scratch. It seems to me risk taking is alive and well, even in this economy. The problem is that people don’t trust the banks, and they don’t trust them because they don’t deserve to be trusted, not because people are irrationally afraid. If fear was the primary driver of most peoples actions our society wouldn’t remotely look like how it is.

December 27th, 2011 at 2:34 pm PST

link

This is very interesting, but there’s one thing that’s troubling me a little about your explanation: why does anyone choose to be an entrepreneur? Entrepreneurs know that they are first in line for losses and that the losses, if they happen, will be large. And the problem with entrepreneurs seldom seems to be unwillingness to accept an even larger portion of losses but rather an absolute limit on loss-bearing capacity. That is, entrepreneurs don’t seek financing for their projects because they are unwilling to self-finance but because they are unable. And they’re typically willing to take career risk on top of whatever financial risk they are capable of bearing. Nobody has to trick entrepreneurs into doing what they do, because they willingly trick themselves into it. Maybe we could say that economic development, like many things in life, thrives on irrational optimism, and the mystification of the financial sector of one several methods to induce that irrational optimism.

December 27th, 2011 at 5:43 pm PST

link

I think you have it all wrong.

I am self employed and I take risks all the time in my business. Since I intend to retire I have no choice but to save and invest. I take risks by investing in equity markets and try to control those risks by being careful and by diversifying.

The complexity of modern finance has nothing to do with raising money. Much lower levels of complexity would be sufficient for effective financial inter-mediation. The complexity has become an impediment. In my view it has gotten to the point where no investor in their right mind would invest in a Chinese, American or European bank.

The complexity has two purposes: (1) gaming regulatory and taxation systems through instruments like interest rate swaps which have no economic purpose (the nominal amount outstanding on interest rate swaps far exceeds size of the bond market) and (2) creating risk out of thin air in the hope that you will get it right and the other guy will get it wrong in an inherently zero sum game (negative sum if you count transaction costs).

December 27th, 2011 at 5:56 pm PST

link

There is another way of looking at complexity.

Suppose you have two young bankers who consider themselves to be immortal, as most young people do. They could enter into a large trade betting against each other on the direction of the US / Euro exchange rate. For our purposes they could as easily bet a billion euros on the toss of a coin. The winner gets a ten million euro bonus and the loser loses his job and has to find another. (If they happen to be hedge fund managers the “bonus” is apparently likely to be over 100 Million euros.)

Those two young bankers have every incentive to make the bet and indeed to manufacture the bet out of thin air if the market does not generate enough risky situations. It is the asymmetric risk faced by bank employees which drives part of the complexity.

December 27th, 2011 at 6:11 pm PST

link

[…] Our Digital Financial OverlordsPosted on December 27, 2011 by Militant1 in MotherJonesSteve Randy Waldman: […]

December 27th, 2011 at 8:58 pm PST

link

The Great Opaque Ponzi Scheme…

After just writing my booms and busts post below, I discovered a beautifully written blog article regarding the banking system, and how it functions in a capitalist society. It is a sound argument, and recognition of the important role played by the b…

December 28th, 2011 at 12:12 am PST

link

Well, you got part of it right. This is why the great red doctor in his eponymous satirical epic styled the “heroes of high finance” sardonically as at once prophets or seers and swindlers or frauds. They were in the business of funding the next wave of technical advance in production, but also always collecting their fees upfront, while arranging to dump the consequences of inevitable glitches in implementation onto others. On the other hand, he also wrote a prescient sketch of the accumulation of fictitious capital at the expense of productive capital, and that might be the more relevant chapter in considering the “growth” in financial complexity nowadays.

December 28th, 2011 at 1:30 am PST

link

[…] “You can have opacity and an industrial economy, or you can have transparency and herd goats” — Interfluidity […]

December 28th, 2011 at 1:43 am PST

link

[…] Like so many good con-men, bankers make themselves believed by persuading each and every investor in… […]

December 28th, 2011 at 3:19 am PST

link

[…] people are going to lose money when they invest, but that's a good thing for the whole. (Interfluidity) also […]

December 28th, 2011 at 9:11 am PST

link

Opacity is inversely proportional to the soundness of risk management and the potential returns to public investors.

“Every thing secret degenerates, even the administration of justice; nothing is safe that does not show how it can bear discussion and publicity.”

Lord Acton

Will we never learn?

December 28th, 2011 at 10:55 am PST

link

SW:

I have long compared banking to alchemy. It’s complicated to let bankers collect rents from their ignorant depositors. Also to facilitate the sale of debt by sovereigns which are insolvent.

December 28th, 2011 at 11:20 am PST

link

I’m with Jesse. This seems a classic case of too smart by half.

Even if we grant your premise, more fear in recent decades would have been to society’s great benefit. All manner of misconceived investments might have been avoided. The end result would surely be a salutary repricing of risk and reward rather than a catastrophic collapse in investment.

December 28th, 2011 at 11:50 am PST

link

Nice point, but I submit that there is a different equilibrium available too – the one that goes something like in a world of honest people, the lone criminal will make a killing. The point being that the very opacity that is provided by banks is easily subverted into a different type of opacity, viz, where it is used to deliberately defraud people.

Note that I’m not necessarily saying that it is *criminal*. It is, however not a globally optimal solution (i.e., instead of society benefiting from the *soft* fraud that you have described, financial institutions benefit from *hard* fraud build on top of the opacity…

December 28th, 2011 at 1:46 pm PST

link

This is bullshit. I, along with everyone I know, am frightened to take the risk of investing *because* of the complexity and opacity of finance.

But then I, along with everyone I know, lie awake at night worrying about our insurance, the thing that is supposed to give us peace of mind. Is this another version of Goodhart’s Law?

December 28th, 2011 at 3:04 pm PST

link

I don’t think so.

Diversification – bundling of these projects – as occurs in corporations and portfolios of corporations and other assets, tremendously lowers the risk.

And as far as things like the good of fiber optics meriting overbuilding, that’s an issue of externalities, where it’s a lot better and more efficient for the government to just subsidize them in various ways, than to rely on huge opacity as a feature of the system.

December 28th, 2011 at 3:38 pm PST

link

I mean, look at Stocks for the Long Run, that’s too scary of a risk long term? It looks super well worth the high expected return for most peoples’ long term money. Diversification seems to make the risks very reasonable for long term money. High opacity looks like usually it would do a lot more harm than good (except for some special cases).

December 28th, 2011 at 3:45 pm PST

link

I don’t see the collective action problem as that hard at all. Stocks are hugely known, and have been known for a long time to have outstanding risk-adjusted returns. And they’re easy to buy in any amount. You’re always going to have trillions put in them even if there’s no opacity, because they’re a great investment long-term in truth when diversified.

As far as entrepreneurs, they tend to have huge inside information on their ventures, making them a lot less risky for them. Plus, entrepreneurs tend to dream big and are willing to take a lot of risk at at least one time in their life (I know from personal experience). One of the horrors of Republican/libertarian world, though, is that it makes the risks so grievous for failure (no health care for your family, severe poverty, maybe for a lifetime, and especially in old age when it gets very hard to start again,…), that far less people will embark on such high-risk/high-return ventures.

December 28th, 2011 at 4:18 pm PST

link

What you’re really getting at more, perhaps, is the great externalities of things like new internet companies in the 90s. Without opacity we wouldn’t have gotten all of this failed investment that created enormous positive externalities. But it’s a lot more efficient to just subsidize high externalities highly, than to have great opacity.

Have huge solar subsidies, and electric car subsidies, and safe nuclear subsidies, and we won’t need huge market opacity to create huge leaps forward in those areas and to get them to high scale. And it will be a lot less costly than constant high opacity, and trickery, and ripping people off, often for things with no positive externalities, or negative ones.

December 28th, 2011 at 4:24 pm PST

link

There seem to be two halves to Economics: One is an attempt to measure and track activities in an economy, and based on the data try to understand the interrelation of those activities; this ultimately leads to mathematical expressions of economic and market forces, based on the data.

The other half simply uses the same tools, not for inquiry leading to evidence and a conclusion, but to cherry-pick details in support of already-held biases or points of view — in other words, obfuscation and propaganda.

In its worst expression, this half of economics only recognizes any rule or theory as a barrier to flow around, in pursuit of more efficient ways to game the system and increase personal wealth (‘#winning’, as Charlie Sheen or Lloyd The CEO might say).

It doesn’t take much to guess which half of Economics has been running the show for over a decade.

December 28th, 2011 at 5:32 pm PST

link

“But absent such a boom, risk-averse individuals will rationally abstain.”

Just not really true. Typically, these projects can be bundled in companies and portfolios of companies, so that the diversified risk is not that bad long term, and well worth the high expected return. Underestimates diversification, risk-pooling, the long term record of stocks speaks for itself very well.

December 28th, 2011 at 9:44 pm PST

link

“Even taking stakes in a diversified basket of risky projects will be unattractive, unless an investor believes that many other investors will simultaneously do the same.”

The investor has a hundreds of years successful track record to believe this. Like any of these games, investors get to trust the coordination, and it becomes self sustaining, with repeated cooperation and success, with a track record. The odds of all other investors abandoning stocks completely and permanently and leaving me in the lurch are zippo. Plus, these companies have safe and existing projects that generate a lot of investment funds internally.

December 28th, 2011 at 9:49 pm PST

link

Honestly, I think opacity may more often than not result in investing too little! not investing too much. Being intimidated, and not understanding the great long term returns on stocks, and the power of a high compound return, results perhaps in LESS good-for-society stock investment, not more. look at the post-depression period.

If all opacity disappeared, if everyone understood investing really well, and the power of a high compound return, I think we’d see much MORE of the good kind of investing.

Coordination’s not an issue. You need only a tiny percentage of the worlds savings to get a nice diversified portfolio of 100 well funded firms going. Very easy to get, especially with the ridiculously successful past record of achieving coordination in the stock market and high returns. And you’d easily have that record for good fundamental reasons with perfect transparency and expertise.

You just don’t need to fool people, or keep them ignorant. There’s usually tons of great long-term risk-adjusted returns in stocks. And where there’s not, but still high externalities, just subsidize those externalities directly, far more efficient than creating confusion.

December 28th, 2011 at 10:02 pm PST

link

This opacity we despise is or institutions not a creature of modern society, or technological advances. It is hard-wired in the human brain. It is why the toddler will deny any knowledge of the broken lamp, why the child will cheat in a game of Go Fish, and why young men and women will go to great lengths to present themselves as something other than what they are.

It is as common in Moldova as in Manhattan, and as well-honed among the poor as among the rich.

There is no fix in this world, technological or otherwise. But one other rule is also universal. Those who listen to and love others get taken less often, and mind it less when they do.

December 28th, 2011 at 11:38 pm PST

link

As something “everybody knows”, “stocks only go up” sure sounds like a candidate for eventual correction at whatever timeframe you’d like to specify; even random walks predict arbitrarily long bear markets.

The cynic in me says that now that the general public has ready access to the stock market, all of the profit will be squeezed out, to reappear somewhere only accessible to the wealthy and well-connected.

December 29th, 2011 at 12:25 am PST

link

[…] banks do much more than simple maturity transformation: they’re involved in what Steve Waldman calls a mutually-beneficial con. (Go read his post, by the way, it’s fabulous. Chris Hayes […]

December 29th, 2011 at 12:57 am PST

link

[…] Source: http://www.interfluidity.com/v2/2669.html […]

December 29th, 2011 at 1:07 am PST

link

Yeah and all those goat herding countries are so famous for their open economies.

December 29th, 2011 at 7:53 am PST

link

Finance is fundamentally simple.

It is the crooks who make it complex in order to obscure what they are doing.

Brilliant, highly intelligent people break down and simplify complexity in order to make it manageable.

The smartest people are those who can cut through the jargonese and turn it into plain language.

You can eat goats. You can drink their milk. You can turn their hides into clothing. You can use their manure as fertiliser. They are intelligent animals – hence their capriciousness!!!

Keeping goats sustainably is a clever thing to do.

December 29th, 2011 at 9:08 am PST

link

“We” are so good at creating complexity in finance because we live in a kleptocracy, and complexity is an essential tool for concealing looting and fraud.

December 29th, 2011 at 9:39 am PST

link

I think some people are missing a key point of the argument. The average investor isn’t the same thing as the average person. The average investor is a person who has enough wealth to invest.

It’s absolutely true that some people are risk-takers, and the average entrepreneur is usually in that category. However, the average risk-taker doesn’t usually have a high level of wealth. Most gamblers don’t become fabulously rich, even though some of them do.

The kind of person who has and keeps a high level of wealth, in other words, your average investor, is risk-averse, almost by definition.

Before capitalism, there were entrepreneurs who were limited by the amount of wealth they could raise from their own resources, family and friends. Big-scale projects were notably difficult, precisely because the kind of people who had enough money to finance them were usually averse to doing so. Of course, there were exceptions. But they were renowned as exceptions.

With the industrial revolution, there was a bigger potential for big-scale projects, but entrepreneurs hit against the problem of having very few potential investors for them. That’s when modern capitalism appeared, and I agree with Steve that there was an element of conning potential investors into believing that projects were less risky than they actually were. It all worked out well, partly because when they all are done at the same time there were bigger chances of success, and partly because many of those innovative ideas would have been profitable anyway, even if done on their own.

What nobody seems to mention is that the payoffs may change over time, with changing circumstances. At some point in the past the payoffs may have been roughly as Steve states. But maybe today the payoffs are different. It’s possible that the payoffs today are such that not investing and hoarding your wealth is the rationally best option for investors, and bankers are merely seeking to get rents out of a game where they know or suspect investors will lose out.

Many commenters note that goat-herding countries aren’t known for their transparency. My personal theory on transparency is that human beings have a certain average level of risk-taking, with some people being more or less than average. This may change a little between different times and places, but societies that take too many risks end up disappearing, and societies that take too few risks end up being backward and being colonized by more adventurous societies. So risk-taking is within a narrow band. On the other hand, uncertainty may come from two origins: it may come from the environment (weather, disease, etc.), or it may come from other people (lies). In times and places where environmental uncertainty is low, people are willing to accept more uncertainty coming from other people, and there is less punishment for lying and stealing. In most modern goat-herding countries today, we have reduced environmental uncertainty to manageable levels, and some such countries have increased people uncertainty in undesirable ways, while others have increased people uncertainty by embarking on a path to industrialization.

December 29th, 2011 at 10:02 am PST

link

[…] “You can have opacity and an industrial economy, or you can have transparency and herd goats” — Interfluidity […]

December 29th, 2011 at 10:07 am PST

link

[…] this is more than a little bit clever. In one of the most quoted pieces in the blogosphere these days, […]

December 29th, 2011 at 11:11 am PST

link

Look, this argument is simply stupid, and would not hold water in any other area. How about this: I’ve been selling this machine that doesn’t do anything useful, but it is so complex that people cannot figure out how it works, so they just keep buying! Sounds like a business plan to you?

December 29th, 2011 at 11:21 am PST

link

I’m not sure what you mean by open economies. Was there something wrong with the way goat herders conduct their trade? Or, by “goat-herding countries”, do you mean those that haven’t bought into modernism so blindly as the US has?

Even if we do have something called an “open economy” in the US, we have dismantled small farming and many other intrinsically worthy institutions, and our society is in a terrible predicament. The “open economy” looks like a turkey to me.

December 29th, 2011 at 11:38 am PST

link

Theory is the backbone but you can’t side-step statistics. It is possible for a bank to take myriad positions but sufficiently hedge and calculate withdrawals based on their fractional reserve system so that despite risky holdings the holders are safe. Combined with the FDIC and Federal Reserve, i believe you over-hype the notion that if transparency existed people wouldn’t use banks.

I work in investments myself, do research on the crisis through my university, and am not fearful. Why should I be?

December 29th, 2011 at 12:52 pm PST

link

You illustrate your model with a game that represents a homogeneous world and a non-iterated decision process, and much of the rest of the argument shares this flavor. But —

* Coordination of investments in complementary products and their supply chains can develop incrementally (as it did).

* This process can incrementally establish rational expectations of positive expected returns from diversified portfolios (as it did, and as others have remarked).

In our intensely multi-causal world, you have, I think, identified an significant component of causation, but have (very likely deliberately) overstated its role and necessity in the overall system dynamics. That amounts to a net contribution, as I’d score it. Thank you.

December 29th, 2011 at 1:29 pm PST

link

[…] Randy Waldman has an interesting post at interfluidity about the role of banks as credit intermediaries and how their existence […]

December 29th, 2011 at 1:33 pm PST

link

“In a world of investment projects whose costs and risks are perfectly transparent, most individuals would be frightened.”

They should be. And those investment projects seeking money would have to either be more convincing through their records of accomplishment, or fund their own new projects with capital existing in-house profits. Short of that, just don’t proceed until more solvent. This prevents over-building and over-extension, and keeps build-out more in line with true market demand. So what would be wrong with that? Free markets require free flow of information in order to work correctly. Disclosure and transparency will always be key.

December 29th, 2011 at 2:19 pm PST

link

The acme of sophistication and thought is to develop a simple system. Complexity is the dreft of confused minds or magicians. Simple is hard.

The statement about ‘if everyone invested we’d all be better off’. Look at Japan, they saved themselves into a funk for a decade and a half. Consumers create the velocity of money that drives robust economies. But also don’t get Savers or Consumers out of balance as it means doom.

Farming is risky. Especially modern farming. Capital outlay for thousands of acres, dozens of pieces of equipment tallying past hundreds of thousands each. Markets that have monopoly intermediaries that buy low from the farmer and sell high to the consumer. Very risky. Even goat herders in antiquity needed capital to start their flock, and where dowries and such systems were created to start new farmers in the business.

And the waves of forward industrial advance are caused by invention. Some one had to build the tool that makes the tool that makes the next device that creates the future.

December 29th, 2011 at 2:37 pm PST

link

This might be a good argument for utility banking, but not for banking in the kleptocratic form practiced today.

December 29th, 2011 at 2:58 pm PST

link

I’d like to see a comparison of different instruments of opacity. Take Lehman’s repo transactions for starters. Was that something that allowed Lehman to take good risks individuals would have been too scared to take? No, it was a way to cheat to keep the firm running in the hope of a miracle. Was that good? If we had known the state of Lehman earlier, couldn’t a more coordinated wind-down have happened?

I would also fundamentally disagree with the premise that we want people taking risks they have no ability to understand. We had a lot of people taking huge risks they thought they understood, but in reality had no understanding of – it’s called the housing bubble, and it turned out terribly.

Also consider the people buying a security. Would knowing that the firm you’re buying it from was actively shorting it make a difference to you? How about if they constructed it with the express purpose of trying to make its failure as probable as possible? Free flow of information is much more important to well functioning capital markets than opacity.

December 29th, 2011 at 3:01 pm PST

link

[…] Why Is Finance So Complex? (Interfluidity) I don’t really agree with the premise, but it’s interesting and that is one of my absolute favorite blogs. […]

December 29th, 2011 at 3:20 pm PST

link

JS Your point about simple versus complex systems is especially apt with regard to traditional farming versus industrial agriculture. The latter is very much of a piece with other sectors of industry, while the former is an entirely different thing that is quite simple, difficult, durable, and healthy. However, it does not scale to national or global proportions, so the market was happy to destroy farming when it grew powerful to do so. That was an extremely bad investment, but the downside is invisible as long as it is taken for granted that financed industry is properly the basis for society.

Industrial advance isn’t caused by invention, rather they are both caused by surplus energy.

Talk about taking huge and misunderstood risks, how about building a civilization upon using up finite energy reserves as fast as possible, then layering financial derivatives on top of that to mask the consequent depletion of resources and degradation of system-wide health?

December 29th, 2011 at 3:24 pm PST

link

Have you ever looked at the financial model that is at the core of Islamic banking, and Islamic finance? Its payoff structure, I think, is different from the standard “Western” model you describe above. Perhaps Islamic banking is closer to the “wholesale reimagining of status quo finance” you mention above?

December 29th, 2011 at 3:48 pm PST

link

[…] “You can have opacity and an industrial economy, or you can have transparency and herd goats” […]

December 29th, 2011 at 5:10 pm PST

link

Arnoud Boot presented a paper at the Atlanta Fed in March attributing increased complexity to increases in marketability, with increasing opacity arising as a result. Boot seems better able to account for *increasing* financial complexity, even if a certain amount of complexity is a necessary part of finance as you suggest.

http://www.frbatlanta.org/documents/news/conferences/11fmc_boot.pdf

December 29th, 2011 at 5:14 pm PST

link

Looked through the rest of it, just don’t see it. You don’t need to con for something that’s fundamentally a good deal, and a well diversified stock portfolio usually is; the risk is usually not high at all given the expected return. Sure, some stocks are a bad deal and require conning at their current price, and sometimes the market is a bad deal, and requires deception or poor judgement to buy at that price, but in that case opacity is bad. It makes for investment in things that aren’t worth it. UNLESS, I repeat UNLESS, there are great externalities. But, as I said, a lot more efficient to just subsidize the externalites, then to infuse opacity and conning all over the place, for the investments with no, or negative, externalities, as well as those with positive. And even if the positive externalites exist, with no consideration for how big, with only consideration for what’s the maximum you can be ripped off for.

December 29th, 2011 at 6:13 pm PST

link

Steve – The basic premise of this argument seems valid – but opacity isn’t the only factor in intermediation – you also have to account for risk pooling and liquidity/maturity mismatch. It is difficult to separate those other aspects of intermediation from the opacity. Could you have a completely transparent financial system that also provides broad risk-sharing and maturity transformation? Maybe where banks listed every loan and investment they made to a very granular level? You still have the problem of imperfect information (even if there were perfect transparency on every single investment, mere mortals couldn’t track all that information).

For that matter, is it really opacity that is needed, or is opacity primarily a cost of specialization and division of labor?

Opacity also provides opportunities for fraud and deception, from the bank that makes honest but bad loan decisions to the complex derivative bets that rely on opacity to extract enormous rents, to outright fraud. I think it is hard to argue that the current level of financial complexity really provides some sort of optimal social results that keep us from herding goats. It seems more likely there is an optimal level of opacity – too little opacity and we are fussing around with micro-managing investments that would be better handled by specialists. Too much and there are too many opportunities for whole-scale looting and mismanagement. Some level between is necessary.

December 29th, 2011 at 7:58 pm PST

link

Las Vegas is complicated too. What isn’t complicated is a gamblers thirst for action. Winning or losing is secondary. A gambler is a very sick person, and thus we have a very sick world. You now what happens to gamblers? They go broke.

December 29th, 2011 at 8:22 pm PST

link

The “smartest people in the room” will always be the first to tell you that they are in fact the “smartest people in the room”, but that won’t stop them from reverting to pure selfishness and greed when the finance cops are looking the other way or have lost their jobs. There’s always somebody who thinks he can change the system to his favor, but it always works only so long, after which the late arrivals have already lost, but that’s exactly what the wiseguy counted on.

December 29th, 2011 at 9:33 pm PST

link

oh no.

I think you’re right.

December 30th, 2011 at 2:20 am PST

link

[…] Source […]

December 30th, 2011 at 9:00 am PST

link

People are confusing broker dealers with banking. The purpose of broker dealers was to supply alternate financing for companies, stocks, bonds, etc. Their mission was to be experts at evaluating corporate risks and informing the investor. Mission creep has them operating as hedge funds for their own book and preying on the investor. Regardless, they are not banks and have no source of funds. Over time they have developed methods of creating and using money substitutes, with leverage, to fund their projects which create spreads from which they can extract real money and collect transfer fees. Basically, they created alternate financing for themselves. If housing finance was exclusively in the domain of the broker dealers, we would have 30 types of mortgage products for investors. Borrowers would be placed in a mortgage by a broker collecting a commission. Garet Garrett wrote a book that included comments on an article by Morrow, “who buys foreign bonds and why”? It was a project of the broker dealers who conjured up loans in countries where the ability to assess risk was impossible. These bonds were sold to farmers and small savers in the US. Morrow had noticed the foreign bond listings in the newspaper had gone from 6 to about 128 and he was curious. Holding companies were another risk opaque device where three $1 million companies were combined and stock issued for a $10 million valuation. Sometimes the companies didn’t exist. It is still done today, buying stocks of companies in China with vapor assets.

December 30th, 2011 at 9:55 am PST

link

Why would financiers and their allies in government create an opaque financial system? George Orwell may have provided the answer:

“Now I will tell you the answer to my question. It is this. The Party seeks power entirely for its own sake. We are not interested in the good of others; we are interested solely in power, pure power. What pure power means you will understand presently. We are different from the oligarchies of the past in that we know what we are doing. All the others, even those who resembled ourselves, were cowards and hypocrites. The German Nazis and the Russian Communists came very close to us in their methods, but they never had the courage to recognize their own motives. They pretended, perhaps they even believed, that they had seized power unwillingly and for a limited time, and that just around the corner there lay a paradise where human beings would be free and equal. We are not like that. We know what no one ever seizes power with the intention of relinquishing it. Power is not a means; it is an end. One does not establish a dictatorship in order to safeguard a revolution; one makes the revolution in order to establish the dictatorship. The object of persecution is persecution. The object of torture is torture. The object of power is power. Now you begin to understand me.”

George Orwell

1984

December 30th, 2011 at 11:44 am PST

link

Ragweed is on the right track. All forms of fractional reserve banking require a form of deception: the promise that you can have your money back at any time. Maturity transformation is risky, and profitable. The opacity helps to disguise the source of the profit. of course banks today are immensely more complex than the early gold merchants who decided to do a bit of lending on the side. But the central deception remains the same.

December 30th, 2011 at 1:47 pm PST

link

[…] […]

December 30th, 2011 at 3:29 pm PST

link

[…] […]

December 30th, 2011 at 3:51 pm PST

link

I don´t believe, that you´ve really made your basic case, from which you then draw your conclusions. Your first example that of an industrialist building a car factory in an agrarian society, isn´t really all that convincing, an entrepreneurial industrialist, would alter the transmission, give the car bigger wheels and make it possible to attach a plow and call it a traktor. All of a sudden the farmer would be able to work a much larger area, producing more food, part of the surplus would go to the industrialist. In the real world, your industrialist would probably start not by building a factory right away, but by individually producing the first cars/traktors(not all that capital intensive).

Your second example, the dotcom bubble you state that Amazon would not have existed without Qwest overbuilding fiber, I can´t quite follow that line of reasoning. Selling books and CDs over the Web, saving on staff and physical stores, was a good idea idea even on 56k dialup connection. Furthermore, by using the example of Amazon, you´ve picked the only major player, still around today, that wasn´t breaking even almost from the start. If you look at some of the others: Google, Ebay, Skype, Facebook and Apple(in terms of mobile internet) you will find that none of them relied on any large amounts of external financing to buid the core of their businness and at least for Google and Ebay, the availability of dark fiber, whilst being a benefit, was not essential. Contrast that with the likes of Webvan and pets.com and you will find that the successful ones had sound business models, where making money and are sitting on huge piles of cash(Apple, Google, Microsoft too) whilst the ones that failed where able to raise large amounts of external financing and just burned through it due to nonworkable business models. Google had to be dragged to go public and was able to dictate the terms, and they did not go public because of a lack of cash.

If anything, taking large amounts of external funding, with the exception of maybe Amazon, was a pretty good indicator of future failure.

One of the positive externalities mentionend is the over building of fiber, the main factor however was that wavelength-division multiplexing actually became commercially viable increasing capacity of optical fibers by a factor of 100. Given that estimates of the total cost of installing fibre surplus to current requirement ranges from 10-50bn$ and assuming it not to be an externality, but to have been paid for by consumers(500mn(fairly well of customers in the west) over 2000-2010 at a cost of 50bn= 5bn p.a. /500mn = $10/p.p./p.a. = less than a dollar per customer/month in terms of high speed connection cost) and that is assuming that one would have wanted to match actual overcapacity rather then just adding on a “as needed” basis.

But moving on, on the basis of the examples you provided you move on to state that savers have the tendency to play it safe and not finance speculative investment, yet Amazon received plenty of equity financing(not bank lending!), covering it´s losses and enabeling it to reach profitability eventually.

I believe your Nash equilibria are overly simplistic and partially incorrect on a whole host of levels, I´ll be using Google as a reference point:

a) Investors that do not believe, that a “mechanical horse” or an “online library”(just to use your examples) could ever be superior to the “real thing” would never invest in a bond or a share of such a company, hence the expected payoff matrix should probably reflect the fact, that the only ones willing to invest are the ones buying into the idea. Furthermore having a monopoly in a smaller market is not necessarily worse than only having a fractional chance of being the top player in a larger market. (Sticking with your example: I´m fairly certain Yahoo shareholders would be perfectly happy with a market, a fraction of the current size, if Yahoo still where the top search engine; i.e. the payoff should be positive for both personal and general investment)

b) The potential returns stated in the tables are vastly wrong! It took 25 million to get Google to profitability; the company is currently valued at ~210bn; hence investing the necessary funds is more akin to buying a lottery ticket then the saver equivalent implied by a 3:1 ratio.

c) The Nash tables in the post seem to indicate, that moving from a 3:1 uncertain payoff to a 2:1 certain one is the sensible thing to do, unfortunately the change in odds is a lot worse

d) Furthermore, buying bonds issued by either Google or Apple today is a very different thing from what it would have been 10 years ago, lending money to a company with cash reserves of a several tens of billions is probably safer then doing it via a bank levered anywhere between 10X-60x.

e) I believe you are off by a couple of orders of magnitude, the investments necessary to start and bring to profitability the companies defining our lives nowadays are in the range of less than 10bn (even assuming a sucess rate of 1:10), the costs for supporting the current financial system measure in the trillions.

December 30th, 2011 at 4:14 pm PST

link

“Amazon losing a nickel on every sale and making it up on volume.”

If you mean Jeff B. had a long range outlook and decided losing in the short term made sense on the path towards building a platform/infrastructure/scale that turned profitable when it hit critical mass, ok.

On your larger point, not a chance. i have to agree with 10, sunshine trumps opacity.

December 30th, 2011 at 7:49 pm PST

link

[…] interfluidity » Why is finance so complex? – Opacity and interconnectedness among major banks is nothing new. Banks and sovereigns have always mixed it up. When there has not been public deposit insurance there have been private deposit insurers as solid and reliable as our own recent “monolines”. “Shadow banks” are nothing new under the sun, just another way of rearranging the entities and guarantees so that almost nobody believes themselves to be on the hook. […]

December 31st, 2011 at 8:12 pm PST

link

[…] one particularly pure example of a financial system prone to overcentalization, bubble-blowing, opacity, and disregard for long-term productivity. Henry Mintzberg has warned that the economy will never […]

January 1st, 2012 at 5:23 pm PST

link

[…] Why is finance so complex? – via http://www.interfluidity.com – Finance has always been complex. More precisely it has always been opaque, and complexity is a means of rationalizing opacity in societies that pretend to transparency. Opacity is absolutely essential to modern finance. It is a feature not a bug until we radically change the way we mobilize economic risk-bearing. The core purpose of status quo finance is to coax people into accepting risks that they would not, if fully informed, consent to bear. […]

January 1st, 2012 at 5:33 pm PST

link

[…] one particularly pure example of a financial system prone to overcentalization, bubble-blowing, opacity, and disregard for long-term productivity. Henry Mintzberg has warned that the economy will never […]

January 1st, 2012 at 7:07 pm PST

link

I find it very helpful and insightful to cast banks as solving the collective action problem of joint investing. However, I have two criticisms:

1) “The core purpose of status quo finance is to coax people into accepting risks that they would not, if fully informed, consent to bear.”

I’m of the view that the CORE purpose is positive– to legitimately diversify risks. Historically, the first shareholders would buy fractional ownership of several different shipping voyages rather than full ownership of one voyage, and the reduced risk encourages more people to fund ship voyages. Finance still does that kind of diversification, which has nothing to do with fooling or conning anyone.

That said, I think you’re right that finance does con people into risks they would not accept if they were fully informed, but I think consider that parasitical on the core purpose. The con game only works because most banking is legitimate.

Similarly, placebos would not be plausible unless there were also lots of real medicines out there.

2) “Societies that lack opaque, faintly fraudulent, financial systems fail to develop and prosper.”

Bold statements like this are wonderful for stimulating thinking. This statement can be settled empirically, of course. Operationalize your statements and then go get the data. I look forward to reading the results.

P.S. Hi from your old NC friend! :-)

January 2nd, 2012 at 11:15 am PST

link

[…] Interfluidity: Why is finance so complex?: Some essays are so good they represent an intellectual punch to the face, necessitating the equivalent of a “standing eight count” of ponderation. One of the undercurrents of Interloper to date has been an effort to illustrate the ways in which the industry subtly misleads its clients, with the intention that more transparency will allow for more investor wealth creation. Waldman turn this on its head by suggesting that hiding risk from investors is one of the primary, and overall economically […]

January 2nd, 2012 at 1:10 pm PST

link

[…] Felix Salmon is one of my favorite writers in this area. He and others have been talking up this post by Steve Waldman as uniquely informative and thought-provoking. I read it and I felt that this was fair, and then I […]

January 2nd, 2012 at 2:41 pm PST

link

[…] Felix Salmon is one of my favorite writers in this area. He and others have been talking up this post by Steve Waldman as uniquely informative and thought-provoking. I read it and I felt that this was fair, and then I […]

January 2nd, 2012 at 2:41 pm PST

link

[…] happens next?This provoked a lengthy and carefully reasoned essay from Steve Randy Waldman, who argues on his blog that such complexity in our banks is necessary to sustain the incredible affluence of our society. […]

January 3rd, 2012 at 4:11 am PST

link

[…] and morality in modern finance. This prompted some rather interesting discussion, among which this post from Interfluidity: Finance has always been complex. More precisely it has always been opaque, and […]

January 3rd, 2012 at 10:03 am PST

link

[…] and probity in complicated finance. This stirred some rather engaging discussion, among that this post from Interfluidity: Finance has always been complex. More precisely it has always been opaque, and […]

January 3rd, 2012 at 10:52 am PST

link

[…] a Boxing Day post, Steve Randy Waldman (http://www.interfluidity.com/v2/2669.html) commented on Ms. Pollock’s conclusion by addressing finance from a different […]

January 3rd, 2012 at 11:47 am PST

link

[…] More on the same theme from Interfluidity […]

January 3rd, 2012 at 5:51 pm PST

link

Are we not discussing just a special case of complexity to achieve opacity to extract dollars from marks? And is the case so special? Is there not the broader argument that without the extraction of marks’ dollars economic activity would plummet to grievous macro effect? Is otherwise senseless manufactured complexity (cf cell phone plans) just another facet of mass marketing?

January 3rd, 2012 at 10:22 pm PST

link

[…] J. Bradford DeLong interfluidity » Why is finance so complex? http://interfluidity.com/v2/2669.html 7 hours […]

January 4th, 2012 at 4:23 am PST

link

[…] in Europe. New funding methodologies that increase transparency reduce complexity and opacity. To suggest opacity is good for economic development is to miss the contractual heart of the relationship between debtors and creditors that has been […]

January 4th, 2012 at 8:37 am PST

link

“A lamentable side effect of opacity, of course, is that it enables a great deal of theft by those placed at the center of the shell game. But surely that is a small price to pay for civilization itself. No?”

For years since the Great Depression, banking served as an engine of economic growth. But since Reagan, deregulation has chipped away at the walls that kept the wolves out of the hen house. Now, with walls completely torn down, the hens have been consumed at the feast. So in 2012, the price we pay for the shell game you defend so eloquently has become far, far too great.

We are not at the seat of “civilization” any more. We’re at a bawdy banquet run by financial crooks – and the middle class has been served up as the main course. Not good for America. Not good at all.

January 4th, 2012 at 10:28 am PST

link

Excellent Article.GW2 Gold

January 5th, 2012 at 3:05 am PST

link

I can’t tell if you’re wearing a shemaugh or a brown shirt…best diablo 3 gold

January 5th, 2012 at 3:31 am PST

link

[…] on the Line (WSJ) • Fed Rate Outlook to Bite Traders (WSJ) • Why is finance so complex? (Interfluidity) • Top MuckReads of 2011: Domestic Surveillance, Shell Companies and College Sports Corruption […]

January 5th, 2012 at 10:35 am PST

link

[…] Steve Randy Wallman applies the stag hunt game to explain opacity in financial markets. Opacity provides the FIRE sector opportunity to win […]

January 6th, 2012 at 1:30 am PST

link