Inequality and demand

I’d rather interfluidity take a break from haranguing Paul Krugman. But I think that the relationship between distribution and demand is a very big deal. I’ve just gotta weigh in.

Here’s Krugman:

Joe [Stiglitz] offers a version of the the “underconsumption” hypothesis, basically that the rich spend too little of their income. This hypothesis has a long history — but it also has well-known theoretical and empirical problems.

It’s true that at any given point in time the rich have much higher savings rates than the poor. Since Milton Friedman, however, we’ve know that this fact is to an important degree a sort of statistical illusion. Consumer spending tends to reflect expected income over an extended period. If you take a sample of people with high incomes, you will disproportionally include people who are having an especially good year, and will therefore be saving a lot; correspondingly, a sample of people with low incomes will include many having a particularly bad year, and hence living off savings. So the cross-sectional evidence on saving doesn’t tell you that a sustained higher concentration of incomes at the top will lead to higher savings; it really tells you nothing at all about what will happen.

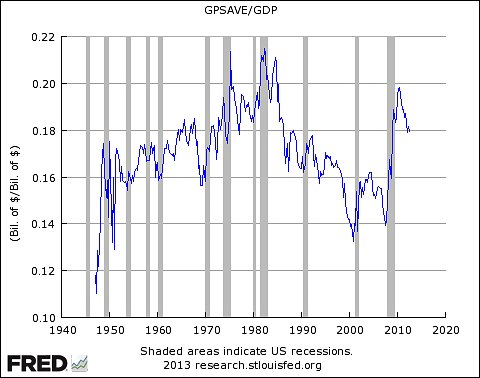

So you turn to the data. We all know that personal saving dropped as inequality rose; but maybe the rich were in effect having corporations save on their behalf. So look at overall private saving as a share of GDP:

The trend before the crisis was down, not up — and that surge with the crisis clearly wasn’t driven by a surge in inequality.

So am I saying that you can have full employment based on purchases of yachts, luxury cars, and the services of personal trainers and celebrity chefs? Well, yes.

Let’s start with the obvious. The claim that income inequality unconditionally leads to underconsumption is untrue. In the US we’ve seen inequality accelerate since the 1980s, and until 2007 we had robust demand, decent growth, and as Krugman points out, no evidence of oversaving in aggregate. Au contraire, even.

And Krugman is correct to point out that simple cross-sectional studies of saving behavior are insufficient to resolve the question.

But that’s why we have social scientists! Unsurprisingly, more sophisticated reviews have been done. See, for example, “Why do the rich save so much?” by Christopher Carroll (ht rsj, Eric Schoenberg) and “Do the Rich Save More?”, by Karen Dynan, Jonathan Skinner, and Stephen Zeldes. These studies agree that the rich do in fact save more, and that they do so in ways that cannot be explained by any version of the permanent income hypothesis. Further, these studies probably understate the differences in savings behavior, because the “rich” they study tend to be members of the top quintile, rather than the top 1% that now accounts for a steeply increasing share of national income.

So how do we reconcile the high savings rates of the rich with the US experience of both rising inequality and strong demand over the “Great Moderation”? If, ceteris paribus, increasing inequality imposes a drag on demand, but demand remained strong, ceteris must not have been paribus.

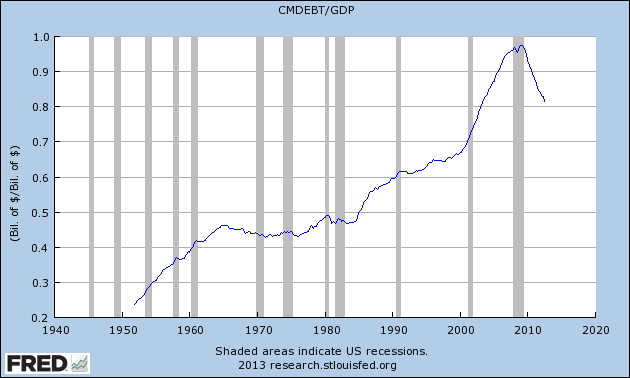

I would pair Krugman’s chart with the following graph, which shows household borrowing as a fraction of GDP:

includes both consumer and mortgage debt, see “credit market instruments” in Table L.100 of the Fed’s Flow of Funds release

Household borrowing represents, in a very direct sense, a redistribution of purchasing power from savers to borrowers. [1] So if we worry that oversaving by the rich may lead to an insufficiency of purchases, household borrowing is a natural place to look for a remedy. Sure enough, we find that beginning in the early 1980s, household borrowing began a secular rise that continued until the financial crisis.

And this arrangement worked! Over the whole “Great Moderation“, inequality expanded while the economy grew and demand remained strong.

Rather than arguing over the (clearly false) claim that income inequality is always inconsistent with adequate demand, let’s consider the conditions under which inequality is compatible with adequate demand. Are those conditions sustainable? Are they desirable?

Suppose that the mechanism that reconciles inequality and adequate demand is household borrowing. Is that sustainable? After all, poorer households would have to borrow new purchasing power in every period in order to support demand for as long as inequality remains high. That’s jarring.

But quantities matter. Continual borrowing might be sustainable, depending on the amount of new borrowing required, the interest rate on the debt, and the growth rate of borrowers’ incomes. If the interest rate is lower than the growth rate of income to poorer households, then there is room for new borrowing every period while holding debt-to-income ratios constant. Even without much income growth, sufficiently low (and especially negative) interest rates can enable continual new borrowing at constant leverage.

If the drag on demand imposed by inequality is sufficiently modest, it can be papered over indefinitely by borrowing without much difficulty. But as the drag grows large and the quantity of new borrowing required increases, sustaining demand will become difficult for institutional reasons. Economically, there’s nothing wrong with letting real interest rates fall to very sharply negative values, if that’s what would be required to create demand. But that would require central banks to tolerate very high rates of inflation, or schemes to invalidate physical cash. It would piss off savers.

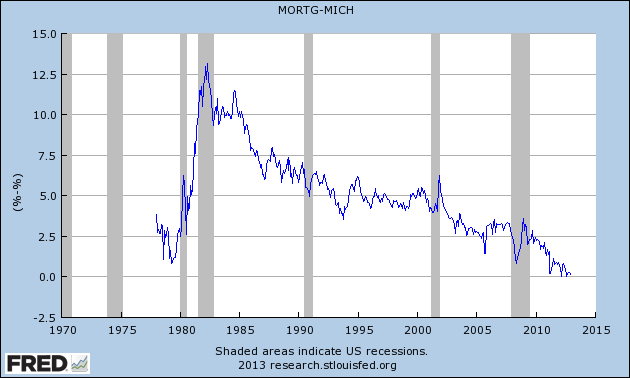

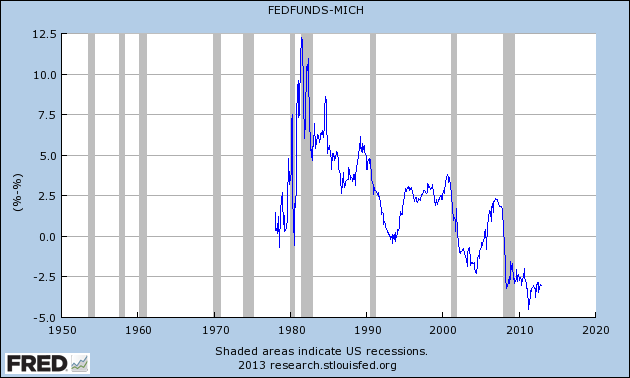

I think the behavior of real interest rates is the empirical fingerprint of the effect of inequality on demand:

Obviously, one can invent any number of explanations for the slow and steady decline in real rates that began with but has outlived the “Great Moderation”. My explanation is that growing inequality required ever greater inducement of ever less solvent households to borrow in order to sustain adequate demand, and central banks delivered. Other stories I’ve encountered don’t strike me as very plausible. Markets would have to be pretty inefficient, or bad news would have had to come in very small drips, if technology or demography is at the root of the decline.

It’s worth noting that these graphs almost certainly understate the decline in interest rates, at least through 2008. Concomitant with the reduction in headline yields, “financial engineering” brought credit spreads down, eventually beneath levels sufficient to cover the cost of defaults. This also helped support demand. John Hempton famously wrote that “banks intermediate the current account deficit.” We very explicitly ask banks to intermediate the deficit in demand, exhorting them to lend lend lend for macroeconomic reasons that are indifferent to microeconomic evaluations of solvency. We can have a banking system that performs the information work of credit analysis and lends appropriately, or we can have a banking system that overcomes deficiencies in demand. We cannot have both when great volumes of lending are continually required for structural reasons.

Paul Krugman argues that “you can have full employment based on purchases of yachts, luxury cars, and the services of personal trainers and celebrity chefs”. What about that? In theory it could happen, but there’s no evidence that it does happen in the real world. As we’ve seen, high income earners do save more than low income earners, and that is not merely an artifact of consumption smoothing.

If the rich did consume in quantities proportionate with their share of income, we would expect the yacht and celebrity chef sectors to become increasingly important components of the national economy. They have not. I’ve squinted pretty hard at the shares of value-added in BEA’s GDP-by-industry accounts, and can’t find any hint of it. I suppose personal trainers and celebrity chefs would fall under “Arts, entertainment, recreation, accommodation, and food services”, a top-level category whose share of GDP did increased by 0.5% between 1990 and 2007. Attributing all of that expansion to the indulgences of the rich, more than 90% of the proportional-consumption expected increase in the top one percent’s consumption remains unaccounted. The share of the “water transportation” sector has not increased. If the rich do consume in proportion to their income, they pretty much consume the same stuff as the rest of us. Which would bring a whole new meaning to the phrase “fat cats”. Categories of output that have notably increased in share of value-added include “professional and business services” and “finance, insurance, real estate, rental, and leasing”. Hmm.

Casual empiricists often point to places like New York City as evidence that rich-people-spending can drive economic demand. Rich Wall-Streeters certainly bluster and whine enough about how their spending supports the local economy. New York is unusually unequal, and it hasn’t especially suffered from an absence of demand. QED, right? Unfortunately, this argument misses something else that’s pretty obvious about New York. It runs a current-account surplus. It is a huge exporter of services to the country and the world. Does New York’s robust aggregate demand come from the personal-training and fancy-restaurant needs of its wealthy upper crust, or from the fact that the rest of the world pays New Yorkers for a lot of the financial services and media they consume? China is very unequal, and rich Chinese have a well-known taste for luxury. But no one imagines that local plutocrats could replace all the world’s Wal-Mart customers and support full employment in the Middle Kingdom. Why is that story any more plausible for New York?

While it’s certainly true that rich people could drive demand by spending money on increasingly marginal goods, the fact of the matter is that they don’t. To explain observed behavior, you need a model where, in Christopher Carroll’s words, “wealth enters consumers’ utility functions directly” such that its “marginal utility decreases more slowly than that of consumption (and hence will be a luxury good relative to consumption)”. It’s not so hard to believe that people like to have money, even much more money than they ever plan to spend on their own consumption or care to pass onto their children. You can explain a preference for wealth in terms of status competition, or in terms of the power over others that wealth confers. I’ve argued that we desire wealth for its insurance value, which is inexhaustible in a world subject to systemic shocks. These motives are not mutually exclusive, and all of them are plausible. Why pick your poison when you can swallow the whole medicine cabinet?

If the world Krugman describes doesn’t exist, we could try to manufacture it. We could tax savings until the marginal utility of extra consumption comes to exceed the after-tax marginal utility of an extra dollar saved. This would shift the behavior of the very wealthy towards demand-supporting expenditures without our having to rely upon a borrowing channel. But politically, enacting such a tax might be as or more difficult than permitting sharply negative interest rates. (A tax on saving rather than income or consumption would be much the same as a negative interest rate.) Moreover, the scheme wouldn’t work if the value wealthy people derive from saving comes from supporting their place in a ranking against other savers (as it would under status-based theories, or in my wealth-as-insurance-against-systemic-risk story). As long as one’s competitors are taxed the same, rescaling the units doesn’t change the game.

So. Inequality is not unconditionally inconsistent with robust demand. But under current institutional arrangements, sustaining demand in the face of inequality requires ongoing borrowing by poorer households. As inequality increases and solvency declines, interest rates must fall or lending standards must be relaxed to engender the requisite borrowing. Eventually this leads to interest rates that are outright negative or else loan defaults and financial turbulence. If we insist on high lending standards and put a floor beneath real interest rates at minus 2%, then growing inequality will indeed result in demand shortfall and stagnation.

Of course, we needn’t hold institutional arrangements constant. If we had any sense at all, we’d relieve our harried bankers (the poor dears!) of contradictory imperatives to both support overall demand and extend credit wisely. We’d regulate aggregate demand by modulating the scale of a outright transfers, and let bankers make their contribution on the supply side, by discriminating between good investment projects and bad when making credit allocation decisions.

[1] Readers might object, reasonably, that since the banking system can create purchasing power ex nihilo, it’s misleading to include the clause “from savers”. But if we posit a regulatory apparatus that prevents the economy from “overheating”, that sets a cap on effective demand in obeisance of some inflation or nominal income target, then the purchasing power made available to borrowers is indirectly transferred from savers. The banking system would not have created new purchasing power for borrowers had savers not saved.

Update History:

- 24-Jan-2012, 1:00 a.m. PST: Fixed a tense: “would have had to come”

- 24-Jan-2012, 11:20 p.m. PST: God I need an editor. Not substantive changes (or at least none intended), but I’m trying to clean up a bit of the word salad: “

in the world we actually live inin the real world“; “spendingdrivessupports the local economy”; “It is a huge exporter of services tothe rest ofthe country and the world.”;”pays New Yorkersof a wide variety of income levelsformucha lot of the financial services, entertainment, and literatureand media they consume?”; “Wal-Mart customersto sustainand support full employment”; “which is inexhaustible in a world subject to systemic shocksthat people must compete to evade.” Also: Added link to NYO piece around “piss off savers”.

Excellent post. I would just add that the Greenspan Put doctrine exacerbated the core problem of inequality – I’ll never quite understand why so many economists ignore the essentially trickle-down nature of modern central banking policy. When central banks prop up asset prices, asset-holders, i.e. the rich, benefit.

Much of this may not make sense within mainstream theory but it can quite easily be fitted into heterodox disequilibrium theory. For example, here’s my Schumpeterian take on post-Keynesian theory http://www.macroresilience.com/2011/11/02/innovation-stagnation-and-unemployment/ which attributes our economic woes and rising inequality to crony capitalism:

“The monetary policy doctrine of the Great Moderation exacerbated the problem of competitive sclerosis and the investment deficit but it also provided the palliative medicine that postponed the day of reckoning.”

January 24th, 2013 at 3:35 am PST

link

[…] – Inequality and demand. […]

January 24th, 2013 at 3:40 am PST

link

SRW: ‘ if we posit a regulatory apparatus that prevents the economy from “overheating”, that sets a cap on effective demand…, then the purchasing power made available to borrowers is indirectly transferred from savers’

You seem to be positing that households in aggregate spend their entire disposable income. But in the 2000s, US and UK households in aggregate ran a deficit (ie they were net borrowers). So to the extent purchasing power was in fact transferred to those (poorer) households which were net borrowers, this reflects a transfer from firms (and foreigners).

January 24th, 2013 at 4:14 am PST

link

Waldman, In the US we’ve seen inequality accelerate since the 1980s, and until 2007 we had robust demand, decent growth, and as Krugman points out, no evidence of oversaving in aggregate. Au contraire, even.

And Krugman is correct to point out that simple cross-sectional studies of saving behavior are insufficient to resolve the question.

But that’s why we have social scientists! Unsurprisingly, more sophisticated reviews have been done.

————-

Hasn’t some econometrics wizard done polynomial cointegration to test for spuriuos correlation? It isn’t exactly a new approach.

January 24th, 2013 at 4:14 am PST

link

An econometrics whiz did do a cointegration test, and found the relationship between savings and inequality inconclusive. http://mpra.ub.uni-muenchen.de/33350/1/incomein.pdf

I guess some social scientists are actually willing to try to be serious about math, as opposed to making dubious assumptions to do easy math.

January 24th, 2013 at 4:21 am PST

link

Steve, thanks. I’m not keen enough to register at NYT to put a similar rebuttal there (and my would be less well argued I’m sure), but ignoring the mechnism of which the demand is “shared” is, let’s say, quite an oversight.

Moreover, I believe we need to look closer at the stability of the scenario. If the majority (say 75% of the population) borrows to consume, if their income grows at less than the interest, the wealth is moved towards wealthy.

If, conversely, income grows faster than the interest rate, they need to borrow less (on constant consumption, i.e. they save), so the wealth gets re-distributed downwards. If consumption grows in line with income, then the situation is stable of course.

Moreover, the rates you need to look at are NOT the wholesale banking rates, but the rates that are actually applicable to the consumer, as for them only those really matter (they can’t borrow from Fed)

Thus, income inequality can start off a positive feedback cycle in either way, and at the moment I’d say we see it more towards the redistribution upwards.

January 24th, 2013 at 4:33 am PST

link

I can’t find anything stated in that article that I could criticise.

I would however suggest that inequality has an important role to play in capitalism and economy generally. Its a self-limiter, in the same sense biological systems have self limiters built in to prevent their metabolisms from going into oerdrive and burning the organism to death.

My point is best illustrated by asking – what if we could through some kind of policy, ensure aggregate demand is always sufficient to consume all output? The answer is you’d get rampant and exponential growth until the system crashed headlong into very final resource constraints. If we could always have sufficient aggregate demand, we have created an economic perpetual motion machine.

Far from being a bug in capitalism, inequality is a rather important feature. I think this fact is under-appreciated in terms of real-world constraints on policy. In fact, the article does allude to this constraint towards the end I think, but never makes it explicit.

January 24th, 2013 at 5:07 am PST

link

The orthodox account is that all that saving is not to drive consumption, but investment, and sustaining that elevated capital stock from elevated depreciation requires a bucketload of employment. Thus, full employment would still be consistent with high borrowing and relatively little wealthy consumption.

Which would be consistent with the graph of the real interest rate, in any case. The real (heh) question is what the households borrow to buy. Wasn’t the econoblogosphere rocked by an argument over whether mortgaged real estate was best considered consumption or investment a while ago?

January 24th, 2013 at 5:11 am PST

link

Not sure about this: “Economically, there’s nothing wrong with letting real interest rates fall to very sharply negative values, if that’s what would be required to create demand. But that would require central banks to tolerate very high rates of inflation, or schemes to invalidate physical cash. It would piss off savers.”

The problem is not the savers, it’s the borrowers! When indebted households are busy deleveraging increased expected inflation (necessary to turn real interest rates negative) will push them to tighten their belts even further. This is because when the problem is depressed aggregate demand due to low private consumption you would expect wages to fail to adjust for ever raising inflation, which would bring an income squeeze, hence the need to save more (proportionally) to pay down outstanding debts. This is a vicious cycle that might more than offset the borrowing leverage you talk about! You just have to look at the UK for a real world example of that mechanism in place, where people accept below-inflation wage-adjustments (or lower hours worked) to keep hold of their jobs and deleverage, but at the cost of unending income squeeze, which depresses private consumption and aggregate demand even further.

January 24th, 2013 at 5:21 am PST

link

Paolo, I think you are right to some extent. If for example inequality was at a level that was more moderate, and there was still a shortfall of demand for some reason, what then? The answer could be that society should discard such fixed capital as is idle until demand is sufficiently strong. The upside of doing this is that unnecessary fixed costs that don’t align with genuine demand are eliminated from our economic machine (these upkeep costs must be paid for from our precious stock of natural resources), which results in a saving of fossil fuels, a reduction in pollution and so on.

This would be an appropriate response if we thought that competition would de-select the correct fixed assets – i.e. the ones society decides are not adding value.

Given that the reduction of the capital stock would imply losses, then quite likely interest rates do need to be negative such that a corresponding amount of financial capital is also retired. In this formulation, the negative interest rates are a means by which a contraction is accomodated in a socially safe way, not a means of avoiding a contraction.

January 24th, 2013 at 5:38 am PST

link

“Obviously, one can invent any number of explanations for the slow and steady decline in real rates that began with but has outlived the “Great Moderation”. My explanation is that growing inequality required ever greater inducement of ever less solvent households to borrow in order to sustain adequate demand, and central banks delivered.”

I think the data you have shown is convincing about the correlations that exist, but the issue I have with this explanation is that it really doesn’t explain anything. Why are we having this inequality? Should we suppose that economic inequality is something that may just appear spontaneously for no particular reason, or purely driven by bad political decisions? I think we need to dig deeper here.

My opinion on the likely cause of inequality, inspired by the studies of the historian Peter Turchin, is that inequality appears as a consequence of (a) shrinking resources and (b) competition (that is very much fuelled by the shrinking resources). Under such conditions, increased competition creates winners and losers, where the winners get richer and the losers get poorer. Now, commodity prices jumped up just about the time when we start seeing this increase in inequality. I think there is a significant connection there.

January 24th, 2013 at 5:55 am PST

link

“Household borrowing represents, in a very direct sense, a redistribution of purchasing power from savers to borrowers.”

Where’s the supporting data on the income/wealth distribution of borrowers? It also included massive amounts of mortgage equity withdrawals (MEW) for consumption spending – prior to the crisis – something that Greenspan used to emphasize. That probably included many high income earners. You don’t have to be poor in income terms to borrow. You can be rich in income terms, and even in wealth terms, but without sufficient “liquidity”.

“My explanation is that growing inequality required ever greater inducement of ever less solvent households to borrow in order to sustain adequate demand, and central banks delivered.”

They “delivered” on interest rates because of disinflation – the level of borrowing was a by product of disinflation – not a central bank objective that ignored inflation.

January 24th, 2013 at 7:28 am PST

link

Disinflation of core CPI excluding housing, food and energy presumably?

Real housing costs have been on the up in the US since the 80’s (the recent crash apart), real food costs since the start of C21, and real oil/energy prices since the late 90s.

January 24th, 2013 at 7:58 am PST

link

Here is more fuel for this fire.

Guest Post: “The Savings Rate Has Recovered…if You Ignore the Bottom 99%”

Read more at http://www.nakedcapitalism.com/2009/08/guest-post-the-savings-rate-has-recoveredif-you-ignore-the-bottom-99.html#H7Th2PHG9aHPdgDk.99

One of my all time favorite posts.

January 24th, 2013 at 9:30 am PST

link

Paolo Siciliani,

Actually, higher demand-side inflation tends to _raise_ aggregate labor income under recession conditions. Yes, real wages may fall slightly, but hours worked increase more than proportionally, due to e.g. lower unemployment.

The UK is not a good example here, since it has actually been suffering from cost-push inflation due to a number of factors, including negative shocks to its financial-services sector.

January 24th, 2013 at 10:47 am PST

link

Mike Sankowski– Thanks for the reference. That is a good post. A moment’s reflection shows how hard it would be for a top earner to spend even 50% of their income.

January 24th, 2013 at 11:14 am PST

link

Re Note [1]: wouldn’t it be better to say, rather than banks “create

purchasing power ex nihilo”, that they “pull purchasing “power from

the future into the present”? The saving that has to take place in

order for banks to lend doesn’t have to be past. It can be future,

as illustrated by the steep decline in cumulative borrowing post-2007.

And some of that decline in debt is due to default (which is ex nihilo

purchasing power, after the fact).

January 24th, 2013 at 11:49 am PST

link

“Categories of output that have notably increased in share of value-added include “professional and business services” and “finance, insurance, real estate, rental, and leasing”. Hmm….”

Go to the BEA site: http://www.bea.gov/iTable/index_industry.cfm

Begin using data…

GDP by industry accounts…. Gross output by industry… Gross output by industry… Options… Select 2000 as the starting year, and highlight all the industries… Export to excel..

In your spreadsheet. Let’s account for population growth (11.3% increase) and inflation (33.3% growth since 2000) Multiply the gross output column for 2000 by 1.113 and by 1.333, into a new column. Then subtract the 2011 column from the column you just created. And for relative sake, you can divide the subtracted result by the 2011 column to se see how much variance we see compared to what we expect.

What has grown: Over what is expected from population and inflation: (top 10)

Support activities for mining – +72% more than expected.

Petroleum and coal products – +57%

Oil and gas extraction – +35%

Federal General government – 31%

Mining – +30%

Rail transportation – +26%

Hospitals – +25%

Primary metal mfg – +24%

Performing arts – +22%

Educational services – +20%

In terms of gross dollar increases above expected we get: (top 5)

Oil production – +$450B

Federal government – +$330B

Hospitals – +$210B

State/local government – +$190B

Ambulatory health – +$170B

We aren’t buying yachts, we’re buying carbon and government and health…

January 24th, 2013 at 4:05 pm PST

link

DD. The rich spend 50% of their income on taxes.

January 24th, 2013 at 4:08 pm PST

link

““professional and business services” and “finance, insurance, real estate, rental, and leasing”. Hmm…”

Professional and business services are only +6% above what is expected from population and inflation.

Finance, insurance, real estate, rental, and leasing is +3%

These are not sectors are not experiencing significant growth.

The rich’s largest expense is likely taxes. And the huge growth in government in the past decade is consuming this expense.

January 24th, 2013 at 4:18 pm PST

link

I don’t think you can use the GDP industry aggregates to discern the share of luxury goods. It seems quite plausible to me that the wealthy are buying the same categories of goods in the same proportions, but paying way more for a better quality or higher quantity of them. They probably spend the same share of income on food as the middle class, but instead of buying their food at the Cheesecake Factory, they are paying for 5 star restaurants and personal chefs. Instead of buying a suburban $250,000 house, they are buying several million dollar mansions. Instead of buying fishing boats, they are buying 150 foot yachts. These need not affect the share in each industry at the aggregate level, and I really wouldn’t expect it to. The changes are within industry. You need firm-level data.

January 24th, 2013 at 4:40 pm PST

link

[…] Inequality and demand (Steve Randy […]

January 24th, 2013 at 6:25 pm PST

link

Really,

You should really read the article. Really. It accounts for taxes.

January 24th, 2013 at 6:26 pm PST

link

Really? — The data I’m looking at is gdp by industry, value added as a share of GDP. That saves the trouble of extrapolating by inflation or population etc. We’re just looking at changes in the composition of GDP, 1990 – 2007.

Here’s a spreadsheet of some of the data I was squinting at.

Matthew’s point is very well taken: If changes in expenditure with income nearly all fall along a quantity dimension, then we would observe neither extraordinarily obese rich people nor changes in the industry composition of GDP. It would be interesting and surprising, if the composition of expenditure varies only by quality within industry. It would imply that at an industry level, there are no luxury goods. But it is possible, and not entirely implausible. My “squint” was not intended to be dispositive. But in the places I could think to look for some evidence of the rich-support-demand-with-increasingly-marginal-consumption-goods hypothesis, I couldn’t find support for it. This is consistent with the more careful studies that suggest the wealthy do in fact save rather than spend an increasing fraction of their wealth.

January 24th, 2013 at 6:32 pm PST

link

OK, here’s my quasi-Marxian theory about the inherently destabilizing and destructive impact of inequality, and its role in generating unemployment. It’s only a theory, because I have no idea how to defend it empirically other than from “observation of life”. These are the elements:

1. The growth in inequality is a self-sustaining process. Inequality in wealth corresponds to inequalities in social power, and so as inequality increases, the wealthy are increasingly empowered to use their power differential to accumulate even more wealth and promote even more social power.

2. An important share of total national wealth consists in the means of production.

3. Production decisions are made by those who own the means of production; they make those decisions to serve their own interests and satisfy their own desires for riches. They produce what they need to produce in order to satisfy those desires, generating only so much aggregate surplus as is needed to motivate others to do work in the kinds and amounts as are needed to produce that desired level of satisfaction.

4. The human desire for riches, while in some sense infinite, diminishes in marginal intensity for most people as those desires are satisfied, approaching a condition of satiety at which the motivation to use ones capital resources to expand production flags.

5. As ownership of the means of production becomes more concentrated, the owners of the means of production are able to satisfy their own desires by employing a smaller share of the national capital and national workforce (1000 people can be twice as rich per capita as 10,000 people, even if the economic system run by the former generates less aggregate output than the system run by the latter.

6. The result is that as wealth and capital ownership continuously concentrates, the economy will disemploy increasing numbers of workers, and also reach a point at which it shrinks the national productive capacity, even as the capital ownership class continues to increase its own per capita wealth.

7. An economy can settle into a sustained period of stagnant – even negative growth – where a shrinking share of the potential workforce is used to increase the well-being of the ownership class, and sustain a tolerable level of well-being for those who provided with work opportunities.

8. The relatively low, stagnant level of satisfaction for those who are working can be made to appear even more tolerable by being compared frequently with representations of the much worse lives of those who are not working.

9. Eventually this all blows up, because while wealth carries a social power premium, marginal increments to that premium diminish, and the trend toward narrower and narrower wealth concentration ultimately leads to the implosion of the reigning capital class. Depending on the details of the wealth distribution trends, it might only lead to a minor social coup in which an aspiring class of the lesser wealthy economically depose the ultra-concentrated and ultra-wealthy top dogs. Or it might lead to something more cataclysmic and revolutionary.

January 24th, 2013 at 6:59 pm PST

link

One needs to deconstruct the saving and consumption of the very wealthy.

First, there is saving in financial assets.

Secondly, there is saving in real assets such as primary investment, real estate, precious metals etc.

The “etc.” includes items that are considered to be consumer goods (“specialty consumer goods”), which the wealthy purchase to enjoy over time or for conspicuous consumption but which are not only not dissipated in consumption but are expected to increase in value. They are purchased as form of “consumption saving,” such as art, collectibles and the like. This is actually a significant portion of luxury spending. I think that calling it “consumption” is misleading.

How much can an individual or family actually consume in the sense of dissipate over a period? Not all that much in comparison with revenue over the period in the case of the very wealthy.

January 24th, 2013 at 7:53 pm PST

link

What is industry value added?

“… Value added equals the difference between an industry’s gross output (consisting of sales or receipts and other operating income, commodity taxes, and inventory change) and the cost of its intermediate inputs (including energy, raw materials, semi-finished goods, and services that are purchased from all sources).”

http://www.bea.gov/faq/index.cfm?faq_id=184

——————–

In English, you are analyzing profit, and I am analyzing output.

——————–

If you are looking for what peopls spend their money on, then why not just look at:

Table 2.5.6 Real Personal Consumption Expenditures by Function, Chained Dollars or,

Table 2.4.6. Real Personal Consumption Expenditures by Type of Product, Chained Dollars (A)

http://www.bea.gov/iTable/iTable.cfm?ReqID=9&step=1

We are spending lots more on housing, recreation and health. (1995-2011)

Lots more on internet access, phones (cell phones), and computer equipment.

“Financial service charges, fees, and commissions” is also up.

“Water transportation” is up 300%.

Not yachts, but cruises.

January 24th, 2013 at 7:58 pm PST

link

Mike,

That NC post looks fundamentally flawed to me.

Each year, a substantial component of high incomes will be in the form of capital gains. The higher earning distribution will shift around depending on the distribution of such gains.

But those gains don’t enter into national income accounting – or saving.

Am I missing something?

Tom,

Similar point on art.

The art business for the most part generates income for art dealers and auctioneers – but apart from that those doing the big dollar buying are swapping existing assets with the sellers – zero direct implication for tracing GDP, income, consumption, or saving at the macro level.

January 24th, 2013 at 8:54 pm PST

link

JKH,

Article mentions both NIPA and IRS data. NIPA excludes capital gains, while IRS includes realized capital gains. However, its unrealized capital gains that’s really missing from the data. Only person I’ve seen drill into this is that unexpected leveler, Arthur Laffer.

http://books.google.com/books?id=QzGAPcjf6ksC&lpg=PA182&pg=PA182#v

January 24th, 2013 at 10:33 pm PST

link

Beo,

Right.

But the point is – the saving measure being analyzed can only be NIPA based – to be coherent.

So a great deal of that higher “income” share includes a component that can’t include saving at all on that basis – meaning the high income “share” of saving being suggested by such numbers is vastly inflated.

IRS capital gains is essentially an asset swap type transaction – not saving from income.

Although taxing capital gains – realized or Laffer-unrealized – does/would reduce disposable income and potential saving on a NIPA basis.

January 24th, 2013 at 11:46 pm PST

link

The introduction of true aging reversal will have very very interesting effects on all of this.

First there will be a consumption increase, buying the new therapy.

But after that, there will be a huge saving effect as the rich people will have to save for 150-200 year lives.

January 25th, 2013 at 12:37 am PST

link

Not sure about the redistribution of savers to borrowers argument.

The capital control system we have at the moment simply requires that a bank converts a deposit into an equity bond to activate another chunk of lending power.

The converted deposit will have come from prior lending. It may have been laundered via the transaction system so that it isn’t directly available but that is largely irrelevant at the macro level. It’s the same as direct.

So the system only stops multiplying when demand for loans stops at the price offered, or the banks can no longer convince anybody to convert deposits to equity bonds – again at the price offered.

For me this whole argument fails to address the very definite empirical increase in the level of private debt relative to GDP. It’s the dynamic non-linear effects of having loans which demand to be serviced regularly from a system where the purchasing behaviour is not necessarily regular that eventually throws the system into cascade default. You have to factor time into the equation. Loans generally don’t allow you time.

January 25th, 2013 at 4:17 am PST

link

1) The Dynan, Skinner and Zeldes (DSZ) paper uses the CEX, SCF and PSID data which produce estimated aggregate savings rates in the range of 25%, 21% and 11-21% respectively over time periods (1980s) in which the savings rate measured by the BEA was approximately 8%-9% (see Table 2). The only data that even comes close to the correct aggregate measure is the PSID measure which uses an “active” measure of savings that effectively excludes capital gains income. This is not suprising because capital gains are not, nor should they be, considered part of GDP.

2) DSZ disaggregate income into quintiles. Does anyone seriously consider the top 20% to be “rich”?

3) Other studies, ones that actually produce aggregate savings rates consistent with the NIPA accounts, have shown that savings rates at times have actually been inversely related to income:

http://www.federalreserve.gov/pubs/feds/2001/200121/200121pap.pdf

This study in particular showed that the savings rate of the top quintile was negative in 2000.

January 25th, 2013 at 10:30 am PST

link

Mason and Jayadev (2012) showed that “Fisher dynamics” – the mechanical effects of

changes in interest rates, growth rates and inflation rates on debt levels independent of

borrowing – explain the evolution of household sector leverage very well:

http://repec.umb.edu/RePEc/files/FisherDynamics.pdf

They find that whereas the household sector borrowed heavily in the 1946-64 period, and more often borrowed than not in the 1965-80 period, the household sector ran a primary surplus throughout the 1981-99 period with the sole exception of 1985. Only more recently, during 2000-2006 did the household sector borrow heavily again. Nevertheless, household sector debt as a percent of disposable personal income rose substantially during 1981-99 due to high real effective interest rates and low rates of growth in nominal income. Thus the rapid growth in household sector debt during 1981-1999 is not due to borrowing.

Moreover, as Krugman notes, this is the period of time when inequality increased substantially and savings rates plummeted in the United States. These facts do not at all match up with Stiglitz’s “underconsumption” hypothesis. This is true even when one examines disaggregated debt and income data. For example the growth in median income leverage during from 1983 to 2007 is easily explained by Fisher dynamics.

January 25th, 2013 at 10:54 am PST

link

Finally, Mason and Jayadev (2012) estimate the the effective interest rate on household sector debt as the weighted average of the rate of mortgage, installment and revolving debt. This lags the current market averages. During 1981-99, 2000-06 and 2007-10 they estimate the real effective interest rate to be 5.6%, 5.5% and 5.3% respectively. (They find that the real effective interest rate was only 2.2% during 1946-64 and 1.7% during 1965-80.) Thus they find that real effective interest rates do not show the strong downward trend since 1980 seen in measures of current real interest rates.

January 25th, 2013 at 11:10 am PST

link

SRW,

You have this meta-theoretical habit: causes are the same because they generate same effects. Look at your old posts on how PKE are NK are closer because they support some form of fiscal policy. Of course, you can hedge: they are ‘almost’ same. This kind of hedging is unproductive if you want to produce knowledge.

You have to evaluate theories based on how better one theory is: in terms of problem-solving capacity (if you are a Laudan fan), in terms of explaining facts, in terms of empirical and conceptual anomalies.

Redistribution of purchasing power is not same as selective creation and destruction of purchasing power. Even the very notion of redestribution is theory-laden: it is part of the dominant paradigm sold by your buddies in the mainstream.

January 25th, 2013 at 2:09 pm PST

link

If the rich save more, isn’t there sort of a divisor (reciprocal of a multiplier) effect to basing an economy around the rich? Most of what they would spend would end up going to other rich people who would save and not spend.

January 25th, 2013 at 4:46 pm PST

link

Bravo!

January 25th, 2013 at 6:59 pm PST

link

Zach, thats exactly why monetary or fiscal stimulus can’t work unless the physical assets which actually attract the final profits in the real economy are not re-distributed.

January 25th, 2013 at 7:11 pm PST

link

People say that extraordinary claims require extraordinary proof.

If this post does not qualify as extraordinary proof, I don’t know what does.

Bravo!

January 26th, 2013 at 12:26 am PST

link

[…] CNETEconomist’s View: ‘Misinterpreting the History of Macroeconomic Thought’interfluidity » Inequality and demandGeorge Osborne’s austerity plan ‘risks lost decade’ for UK economy | Politics | […]

January 26th, 2013 at 6:21 pm PST

link

Dear Steve,

First time on your blog. I read this article with some interest then I moved to your old article that you were referring to at http://observer.com/2010/07/the-evils-of-saving/

I touched on this article as you continue referring to it.

I have never seen an article where an author is accusing victims of financial murder instead of real culprits.

First, please do not equate people buying bonds/CDs to savers. I consider myself a saver and have zero bonds and no CD.

There are savers out there who are trying to get things right.

Do not bark at me – a saver – since :

1) I was born into this fiat system. There is no single country without it.

2) I have no real control how government is spending all the money it is supposedly taking away from me in the form of taxes for my well-being later on (pension system. educational system, etc).

3) I am trying to save in precious metals, working my butt off, doing my best in my job creating wealth, so when I have enough true money saved, I can focus on starting my own company and create wealth in this manner. I hope to be, later on, a better wealth creator than my current employer.

4) I am trying my best to educate my fellow savers (including writing response at your blog).

It is not the fault of the savers that their wealth is being stolen from them so they can never feel like they can move on to more risky ways of creating value/wealth.

It is fiat money advocates/junkies you should bark at. It is them who steal through inflation wealth from hard working people never giving them a chance to stop and think for a moment to better allocate their savings. It is this fiat system that persists lack of financial education of the people within the education system. Poor people/”savers” investing in bonds and CDs are just uneducated victims of the banksters/politicians class. These people manipulate inflation calculations, provide false assurances like FDIC, … to keep simple folks unaware of the fraud going on daily.

Moreover, in this article you are supporting FDIC, instead of seeing it as means to pacify CD holders that would otherwise have more chance to choose other better methods of saving. Moreover, you suggest between the lines that they can protect their savings from the inflation. You wasted a perfect opportunity to wake up some of those misguided soals by explaining them true causes of our problems.

We had decent (not perfect! as it is not possible in this world) system based on gold/silver. A saver was paying a price for keeping its savings in gold, but it truly had an ironclad insurance without counter party risk. It was self regulating system where an increase of savers meant more lost opportunity to buy cheap thus rewarding people who could find the proper way of allocating their savings. People who could change from savers to entrepreneurs (or vice versa) at the right moment were benefiting most! An amazing balance mechanism between savers and debtors, rewarding those who can see the inbalance and act accordingly. Governments had to tax people explicitly and not in a hidden way with the help of inflation so they had much harder time to feed an army of bureaucrats or start wars.

Financial instruments like stocks is even worse negligence of owner responsibility to take care of their savings. The law that enacted Plunge Protection Team and policy of central bankers (like Greenspan put) had the same intent to pacify stock investors to keep them unaware. You are barking at CD/bond savers and expect them to invest properly in stock market? This is truly insane expectation on those uneducated savers. No matter what saving approach (even precious metals due to their volatility) will not help an *uneducated* saver never be able to attain significant wealth. I am not surprised that most people go into debt like there is no tomorrow because given their financial knowledge there is no tomorrow for them.

You make your proof but forget one vital aspect. More and more savers are getting educated. Thus they will not willingly sacrifice their purchasing power to keep the system afloat. The negative interests rates will not last forever. The whole con game of inflating away the debt to keep status quo of fiat money is slowly falling apart. An appetizer in 2008 was a great wake up call for many people. In 2013 we may well be served the main dish of financial crisis due to the OTC derivatives.

“The Evils of Saving” article completely misses the point. Luckily, there is a growing number of educated savers that hopefully will make this fiat system collapse due to decreasing demand for fiat money, while its supply grows at amazing speed. The only question remains will it be a bloody collapse and what will be created afterwards? We can only hope and work hard to educate people around us so that we have peaceful collapse and an honest system after collapse and not even more globalized/controlled money system.

Sir, you are missing the point completely by barking at the savers.

Sir, you are not helping in what truly matters which is financial education of the masses, so they can not be screwed and have time to make the right decisions not only in financial matters but all aspects of their life.

Sir, if you truly hate savers then I have sad news for you. We are growing in numbers and getting smarter.

You have such a great writing potential, so utilize it well.

best regards,

Radek

January 27th, 2013 at 9:02 am PST

link

Steve,

Back to your premise: There is inequality, and where is the consumption of the rich?

You seem to be concerned with the relationship of inequality and the consumption from 1990-2007. Nearly all the income inequality that we see in that period happened from 1994-2000. There has been very little change of income inequality since 2000.

You use the words “wealth” and “wealthy” a number of times. Wealth has nearly no place in this conversation. (I presume you are not a US citizen and know little about our tax system and our Constitution) The US taxes income, not wealth. Our Constitution does not allow wealth taxation. Your fixation on the “wealthy” only confuses non-Americans, and poorly educated Americans.

Lastly, there are many examples of countries with very low GINI. Can you explain why Cuba, North Korea, the old Soviet Union, or Vietnam grew at very slow rates compared to countries with more inequality? A perfect example of this is North Korea, who had higher GDP/capita, more education, more wealth, more raw materials – more of nearly everything – than the poor South Koreans. How did the income equality of North Korea work out for them?

January 28th, 2013 at 10:31 am PST

link

that’s the Economics View

January 28th, 2013 at 6:42 pm PST

link

Hi Steve,

Thank you for this post. Vbounded hurled stones at you for your inferential approach to your question, which I thought less-than-civil. Using the narrow topic of the relationship to discuss the broader issue of inequality, it is perhaps even more interesting to open up the question further, look at it in a dynamic context and ask: “Where does it lead?” and “What are the logical policy responses?” from that result.

Interestingly, Fernholz & Fernholz have done precisely that in this paper on modeling inequality which effectively constructs a macro model of the economy and income distribution (answering VBounded’s pleas for the elegant maths), and runs the game through time. The result is no surprise: like monopoly, the winner takes all. And the prescription, verbatim:

It is also worth noting by those who are predisposed to disagree ex-ante with conclusions on ideological grounds , that Bob Fernholz is NOT some lefty crackpot but the founder of a $40bn quantitative investment firm (now owned by Janus) and is a model builder by trade.

–C

February 1st, 2013 at 4:51 am PST

link

Cassandra,

As children we modified Monopoly so as to make the game run longer. Simple, we just let the players have all the money they wanted. What happened was that all the plots were traded to become monopolies and soon had hotels on them. The players cycled through, paying and collecting rents from each other. A steady state prosperity. It might be interesting to see if a mathematical model would give the same results.

February 2nd, 2013 at 2:58 pm PST

link

allis, i’d thought of the same thing – but trying (because it is dynamic) to conceive the tipping point of the game – which may be deterministic and quite early should one be making the mathematical odds, though it likely manifests itself much later in time when the losing players, realizing the futility game, simply walk away, or worse, violently upends the board…

February 3rd, 2013 at 3:01 pm PST

link

I worry that a negative interest rate would not be at all like an asset tax. A negative interest rate would mean subsidized leverage for speculation. The commodity trading desks at JPMorgan and Goldman Sachs would be rubbing their hands in glee. It would also provide a windfall for everyone holding 30year treasury bonds. The price of long term treasuries and gold would rocket up. Already the business cycle seems to have evolved into being cyclical price spikes in commodities driven by speculation. The lower interest rates go, the more acute commodity price volatility will become IMO.

February 4th, 2013 at 3:48 am PST

link

How are you accounting for real estate? Perhaps the canonical case of a product that is ambiguous between consumption and investment. Rich people often seem to want lots of house, as a mix of enjoyable consumption, unambiguous status-value, opportunity to project political power, an investment that is often tax-efficient, a bequest that is often tax-efficient, and very often a form of insurance against political uncertainties of various kinds (at one end, Hitler; at the other, inquiry into the sources of one’s wealth).

And, you know, the great economic event of our times was marked by a massive run-up in property.

February 4th, 2013 at 7:00 pm PST

link