Inequality and demand

I’d rather interfluidity take a break from haranguing Paul Krugman. But I think that the relationship between distribution and demand is a very big deal. I’ve just gotta weigh in.

Here’s Krugman:

Joe [Stiglitz] offers a version of the the “underconsumption” hypothesis, basically that the rich spend too little of their income. This hypothesis has a long history — but it also has well-known theoretical and empirical problems.

It’s true that at any given point in time the rich have much higher savings rates than the poor. Since Milton Friedman, however, we’ve know that this fact is to an important degree a sort of statistical illusion. Consumer spending tends to reflect expected income over an extended period. If you take a sample of people with high incomes, you will disproportionally include people who are having an especially good year, and will therefore be saving a lot; correspondingly, a sample of people with low incomes will include many having a particularly bad year, and hence living off savings. So the cross-sectional evidence on saving doesn’t tell you that a sustained higher concentration of incomes at the top will lead to higher savings; it really tells you nothing at all about what will happen.

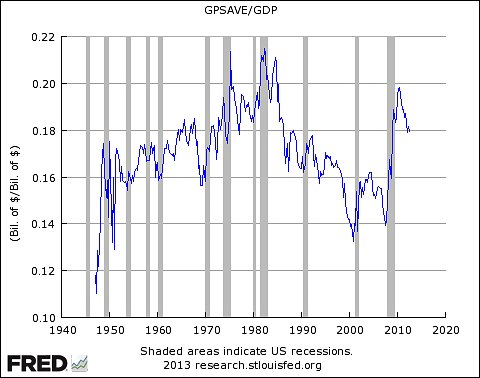

So you turn to the data. We all know that personal saving dropped as inequality rose; but maybe the rich were in effect having corporations save on their behalf. So look at overall private saving as a share of GDP:

The trend before the crisis was down, not up — and that surge with the crisis clearly wasn’t driven by a surge in inequality.

So am I saying that you can have full employment based on purchases of yachts, luxury cars, and the services of personal trainers and celebrity chefs? Well, yes.

Let’s start with the obvious. The claim that income inequality unconditionally leads to underconsumption is untrue. In the US we’ve seen inequality accelerate since the 1980s, and until 2007 we had robust demand, decent growth, and as Krugman points out, no evidence of oversaving in aggregate. Au contraire, even.

And Krugman is correct to point out that simple cross-sectional studies of saving behavior are insufficient to resolve the question.

But that’s why we have social scientists! Unsurprisingly, more sophisticated reviews have been done. See, for example, “Why do the rich save so much?” by Christopher Carroll (ht rsj, Eric Schoenberg) and “Do the Rich Save More?”, by Karen Dynan, Jonathan Skinner, and Stephen Zeldes. These studies agree that the rich do in fact save more, and that they do so in ways that cannot be explained by any version of the permanent income hypothesis. Further, these studies probably understate the differences in savings behavior, because the “rich” they study tend to be members of the top quintile, rather than the top 1% that now accounts for a steeply increasing share of national income.

So how do we reconcile the high savings rates of the rich with the US experience of both rising inequality and strong demand over the “Great Moderation”? If, ceteris paribus, increasing inequality imposes a drag on demand, but demand remained strong, ceteris must not have been paribus.

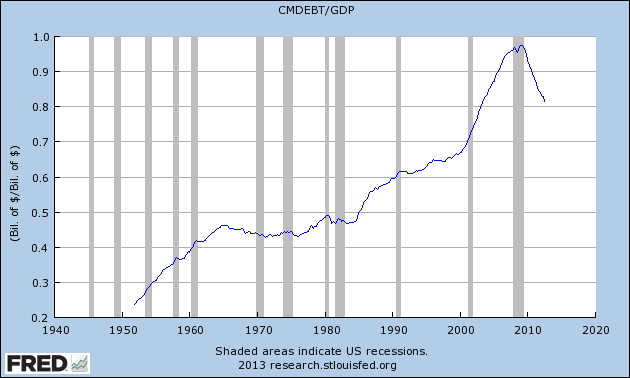

I would pair Krugman’s chart with the following graph, which shows household borrowing as a fraction of GDP:

includes both consumer and mortgage debt, see “credit market instruments” in Table L.100 of the Fed’s Flow of Funds release

Household borrowing represents, in a very direct sense, a redistribution of purchasing power from savers to borrowers. [1] So if we worry that oversaving by the rich may lead to an insufficiency of purchases, household borrowing is a natural place to look for a remedy. Sure enough, we find that beginning in the early 1980s, household borrowing began a secular rise that continued until the financial crisis.

And this arrangement worked! Over the whole “Great Moderation“, inequality expanded while the economy grew and demand remained strong.

Rather than arguing over the (clearly false) claim that income inequality is always inconsistent with adequate demand, let’s consider the conditions under which inequality is compatible with adequate demand. Are those conditions sustainable? Are they desirable?

Suppose that the mechanism that reconciles inequality and adequate demand is household borrowing. Is that sustainable? After all, poorer households would have to borrow new purchasing power in every period in order to support demand for as long as inequality remains high. That’s jarring.

But quantities matter. Continual borrowing might be sustainable, depending on the amount of new borrowing required, the interest rate on the debt, and the growth rate of borrowers’ incomes. If the interest rate is lower than the growth rate of income to poorer households, then there is room for new borrowing every period while holding debt-to-income ratios constant. Even without much income growth, sufficiently low (and especially negative) interest rates can enable continual new borrowing at constant leverage.

If the drag on demand imposed by inequality is sufficiently modest, it can be papered over indefinitely by borrowing without much difficulty. But as the drag grows large and the quantity of new borrowing required increases, sustaining demand will become difficult for institutional reasons. Economically, there’s nothing wrong with letting real interest rates fall to very sharply negative values, if that’s what would be required to create demand. But that would require central banks to tolerate very high rates of inflation, or schemes to invalidate physical cash. It would piss off savers.

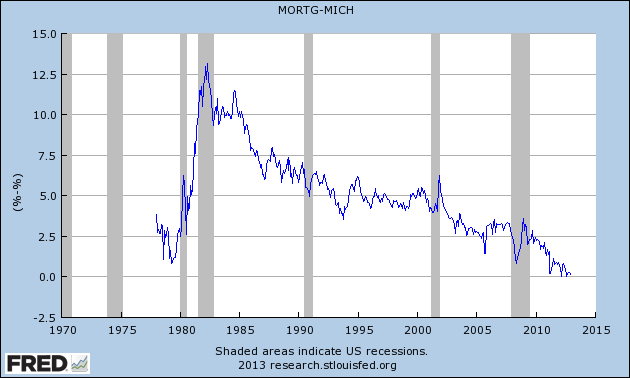

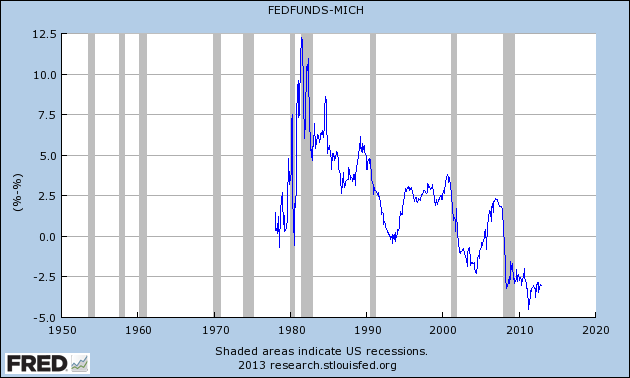

I think the behavior of real interest rates is the empirical fingerprint of the effect of inequality on demand:

Obviously, one can invent any number of explanations for the slow and steady decline in real rates that began with but has outlived the “Great Moderation”. My explanation is that growing inequality required ever greater inducement of ever less solvent households to borrow in order to sustain adequate demand, and central banks delivered. Other stories I’ve encountered don’t strike me as very plausible. Markets would have to be pretty inefficient, or bad news would have had to come in very small drips, if technology or demography is at the root of the decline.

It’s worth noting that these graphs almost certainly understate the decline in interest rates, at least through 2008. Concomitant with the reduction in headline yields, “financial engineering” brought credit spreads down, eventually beneath levels sufficient to cover the cost of defaults. This also helped support demand. John Hempton famously wrote that “banks intermediate the current account deficit.” We very explicitly ask banks to intermediate the deficit in demand, exhorting them to lend lend lend for macroeconomic reasons that are indifferent to microeconomic evaluations of solvency. We can have a banking system that performs the information work of credit analysis and lends appropriately, or we can have a banking system that overcomes deficiencies in demand. We cannot have both when great volumes of lending are continually required for structural reasons.

Paul Krugman argues that “you can have full employment based on purchases of yachts, luxury cars, and the services of personal trainers and celebrity chefs”. What about that? In theory it could happen, but there’s no evidence that it does happen in the real world. As we’ve seen, high income earners do save more than low income earners, and that is not merely an artifact of consumption smoothing.

If the rich did consume in quantities proportionate with their share of income, we would expect the yacht and celebrity chef sectors to become increasingly important components of the national economy. They have not. I’ve squinted pretty hard at the shares of value-added in BEA’s GDP-by-industry accounts, and can’t find any hint of it. I suppose personal trainers and celebrity chefs would fall under “Arts, entertainment, recreation, accommodation, and food services”, a top-level category whose share of GDP did increased by 0.5% between 1990 and 2007. Attributing all of that expansion to the indulgences of the rich, more than 90% of the proportional-consumption expected increase in the top one percent’s consumption remains unaccounted. The share of the “water transportation” sector has not increased. If the rich do consume in proportion to their income, they pretty much consume the same stuff as the rest of us. Which would bring a whole new meaning to the phrase “fat cats”. Categories of output that have notably increased in share of value-added include “professional and business services” and “finance, insurance, real estate, rental, and leasing”. Hmm.

Casual empiricists often point to places like New York City as evidence that rich-people-spending can drive economic demand. Rich Wall-Streeters certainly bluster and whine enough about how their spending supports the local economy. New York is unusually unequal, and it hasn’t especially suffered from an absence of demand. QED, right? Unfortunately, this argument misses something else that’s pretty obvious about New York. It runs a current-account surplus. It is a huge exporter of services to the country and the world. Does New York’s robust aggregate demand come from the personal-training and fancy-restaurant needs of its wealthy upper crust, or from the fact that the rest of the world pays New Yorkers for a lot of the financial services and media they consume? China is very unequal, and rich Chinese have a well-known taste for luxury. But no one imagines that local plutocrats could replace all the world’s Wal-Mart customers and support full employment in the Middle Kingdom. Why is that story any more plausible for New York?

While it’s certainly true that rich people could drive demand by spending money on increasingly marginal goods, the fact of the matter is that they don’t. To explain observed behavior, you need a model where, in Christopher Carroll’s words, “wealth enters consumers’ utility functions directly” such that its “marginal utility decreases more slowly than that of consumption (and hence will be a luxury good relative to consumption)”. It’s not so hard to believe that people like to have money, even much more money than they ever plan to spend on their own consumption or care to pass onto their children. You can explain a preference for wealth in terms of status competition, or in terms of the power over others that wealth confers. I’ve argued that we desire wealth for its insurance value, which is inexhaustible in a world subject to systemic shocks. These motives are not mutually exclusive, and all of them are plausible. Why pick your poison when you can swallow the whole medicine cabinet?

If the world Krugman describes doesn’t exist, we could try to manufacture it. We could tax savings until the marginal utility of extra consumption comes to exceed the after-tax marginal utility of an extra dollar saved. This would shift the behavior of the very wealthy towards demand-supporting expenditures without our having to rely upon a borrowing channel. But politically, enacting such a tax might be as or more difficult than permitting sharply negative interest rates. (A tax on saving rather than income or consumption would be much the same as a negative interest rate.) Moreover, the scheme wouldn’t work if the value wealthy people derive from saving comes from supporting their place in a ranking against other savers (as it would under status-based theories, or in my wealth-as-insurance-against-systemic-risk story). As long as one’s competitors are taxed the same, rescaling the units doesn’t change the game.

So. Inequality is not unconditionally inconsistent with robust demand. But under current institutional arrangements, sustaining demand in the face of inequality requires ongoing borrowing by poorer households. As inequality increases and solvency declines, interest rates must fall or lending standards must be relaxed to engender the requisite borrowing. Eventually this leads to interest rates that are outright negative or else loan defaults and financial turbulence. If we insist on high lending standards and put a floor beneath real interest rates at minus 2%, then growing inequality will indeed result in demand shortfall and stagnation.

Of course, we needn’t hold institutional arrangements constant. If we had any sense at all, we’d relieve our harried bankers (the poor dears!) of contradictory imperatives to both support overall demand and extend credit wisely. We’d regulate aggregate demand by modulating the scale of a outright transfers, and let bankers make their contribution on the supply side, by discriminating between good investment projects and bad when making credit allocation decisions.

[1] Readers might object, reasonably, that since the banking system can create purchasing power ex nihilo, it’s misleading to include the clause “from savers”. But if we posit a regulatory apparatus that prevents the economy from “overheating”, that sets a cap on effective demand in obeisance of some inflation or nominal income target, then the purchasing power made available to borrowers is indirectly transferred from savers. The banking system would not have created new purchasing power for borrowers had savers not saved.

Update History:

- 24-Jan-2012, 1:00 a.m. PST: Fixed a tense: “would have had to come”

- 24-Jan-2012, 11:20 p.m. PST: God I need an editor. Not substantive changes (or at least none intended), but I’m trying to clean up a bit of the word salad: “

in the world we actually live inin the real world“; “spendingdrivessupports the local economy”; “It is a huge exporter of services tothe rest ofthe country and the world.”;”pays New Yorkersof a wide variety of income levelsformucha lot of the financial services, entertainment, and literatureand media they consume?”; “Wal-Mart customersto sustainand support full employment”; “which is inexhaustible in a world subject to systemic shocksthat people must compete to evade.” Also: Added link to NYO piece around “piss off savers”.