Steve Randy Waldman

@interfluidity.com

it does suck. but going from a suck equilibrium to a great one is a challenge to which neither of us have an answer. 1/

it does suck. but going from a suck equilibrium to a great one is a challenge to which neither of us have an answer. 1/

one answer is somehow just find the money to run high frequency clean buses, build it and they will come. from this perspective fares help. another is encourage more middle class use of what exists and hope that changes the politics so we can actually find that money in the US. 2/

which approach is best? both are currently unlikely. i'll stay off a high about the second approach, but i'd recommend you do the same about the first. /fin

it's great you don't need metrocards anymore! but the NYC subway is an easy case, it's already very much middle class transit. the challenge is places like my native Baltimore, where "everybody" has a car and transit is perceived as an underclass ghetto. (i don't know how bus fares work there now!)

there is a case consistent with this for free transit, which is simply that middle-class habitual drivers are put off by the fare box, that at a psychological level dealing with the awkwardness of cash or getting a transit card means middle class people who otherwise might never step on a bus. 1/

it’s not the cost of the fare, it’s the barrier to casual entrance that prevents middle-class people from slipping toward mixed-automotive-and-transit lifestyles that woukd make fully transit-based lifestyles more thinkable. 2/

making payment of fares much more convenient, and advertising that widely, could help. just tap an ordinary payment card, easy peasy! but even that’s not nothing, and most places don’t even have that. /fin

i don’t think it’s that tough! it’s not that we have to let bad things happen, it’s that we have to take seriously bad things that might only happen infrequently. 1/

again, stabilizing inflation and the business cycle was not the problem. it was that we let triumphalism over this superficial stability lull us into complacency about things we all knew were occurring! 2/

we knew, in the triumphalist 1990s, that inequality was accelerating, manufacturing was offshoring and trade imbalance growing, that households were increasingly reliant on wealth and asset appreciation. the policy community cheerled financial complexity. 3/

we could have addressed these issues while finding ways to keep inflation low and business cycles moderate. (to address inequality we’d have had to tolerate the “bad things” of asset wealth losses, but we could have cushioned the “main street” impacts.) 4/

the problem is that slow, quiet poisons develop interested constituencies, and absent some sense of crisis, it’s politically difficult to overcome those constituencies and enact an antidote. 5/

if we can do a better job of avoiding those poisons, or if we can improve the political system to act capably even against strong parochial resistance absent crises, we don’t need the frequent crisis! 6/

(but if we can’t do those things, we might. that indeed would be a hard pill to swallow. even there, however, like controlled forest burns, we can design for more smaller, frequent crises to be tolerable.) /fin

(jinx!)

i guess i’d point to Minsky a bit on that. or Ashwin/macroresilience. tempering high-frequency business cycles may be bad for overall systemic stability. the “great moderation” stabilized an era of burgeoning inequality, indebtedness, and financial fragility until a large crisis resulted. 1/

more frequent course corrections might be better than stabilization that leaves underlying vulnerabilities unaddressed. Ashwin likes to use the forest fire analogy, better to do frequent controlled burns to address fuel accumulation than to suppress indefinitely until any fire will be massive. 2/

the lesson isn’t Mellonist recessions-are-good. it’s that when you have stability, you have to pay great attention to the dynamics underlying what you are stabilizing. 3/

the problem of the Great Moderation was not the moderation of the business cycles, but the insouciance it enabled re household debt growth (“democratization of credit”), fragile securitiz8ns, domino credit risk in financial derivatives, especially wealth+income rather than consumption inequality. 4/

this is exacerbated by an empirical, “social scientistic” ethos within the policy community. partial stabilization condenses problems into low frequency events. there is no evidence to point to in the high-frequency data, in the good sample sizes, between those events. 5/

this is not to say that all versions of economic liberalism (“neoliberalism?”) are doomed to collapse, nor is it to say that people like Friedman were anything worse than mistaken in their optimism. We can all be mistaken. 6/

but the late 20th C version of economic liberalism really has failed, and part of its failure derives from the partial stabilization we built into it and the hubris that resulted. whatever kind of mixed economy we hopefully will try next needs to attend to what the last iteration did not. /fin

this too shall pass, nothing is ultimately enduring! but we don’t know how good things can be or how long things can last, we can just go for as good as long as we can. 1/

economic liberalism has failed multiple times, but i don’t propose we do away with it. i propose we modify it, learn from the specifics of how it has failed, reorganize, regulate, cabin it in ways likely to prevent those failures and other failures we can foresee. 2/

we will always have the unforeseeable to contend with. 3/

social democracy (itself a hybrid of socialist and economic-liberal ideas) collapsed in much of the world over the 1970s. that doesn’t mean we jettison it, presume it is doomed to rapid collapse. 4/

like “economic liberalism”, it refers to a broad space of possible arrangements. we try to learn from experience how to make its considerable virtues more resilient and sustainable than the last time around. 5/

how well can we succeed at this? we can’t know. but lots of fruitful development takes the form of failure and iteration. it’s unwise to let failure signal its useless to iterate, if the goals you are not quite adequately achieving remain worth pursuing. /fin

Excellent. cc @poetryforsupper.bsky.social

Loading quoted Bluesky post...

i’m glad to concede that “neoliberalism” has become kind of a bogeyman, often used as an ill-defined target of free-floating opprobrium. when i write, i try to define what i mean when i use the term, e.g. www.interfluidity.com/v2/7333.html 1/

here i was intervening in a debate that had already adopted neoliberalism, and it seemed fine to go with in a you-know-what-they-mean way. 2/

laissez faire is maybe more specific. i think neoliberalism actually connotes something a bit stronger than that, colonization by market mechanisms of traditionally nonmarket spheres. /fin

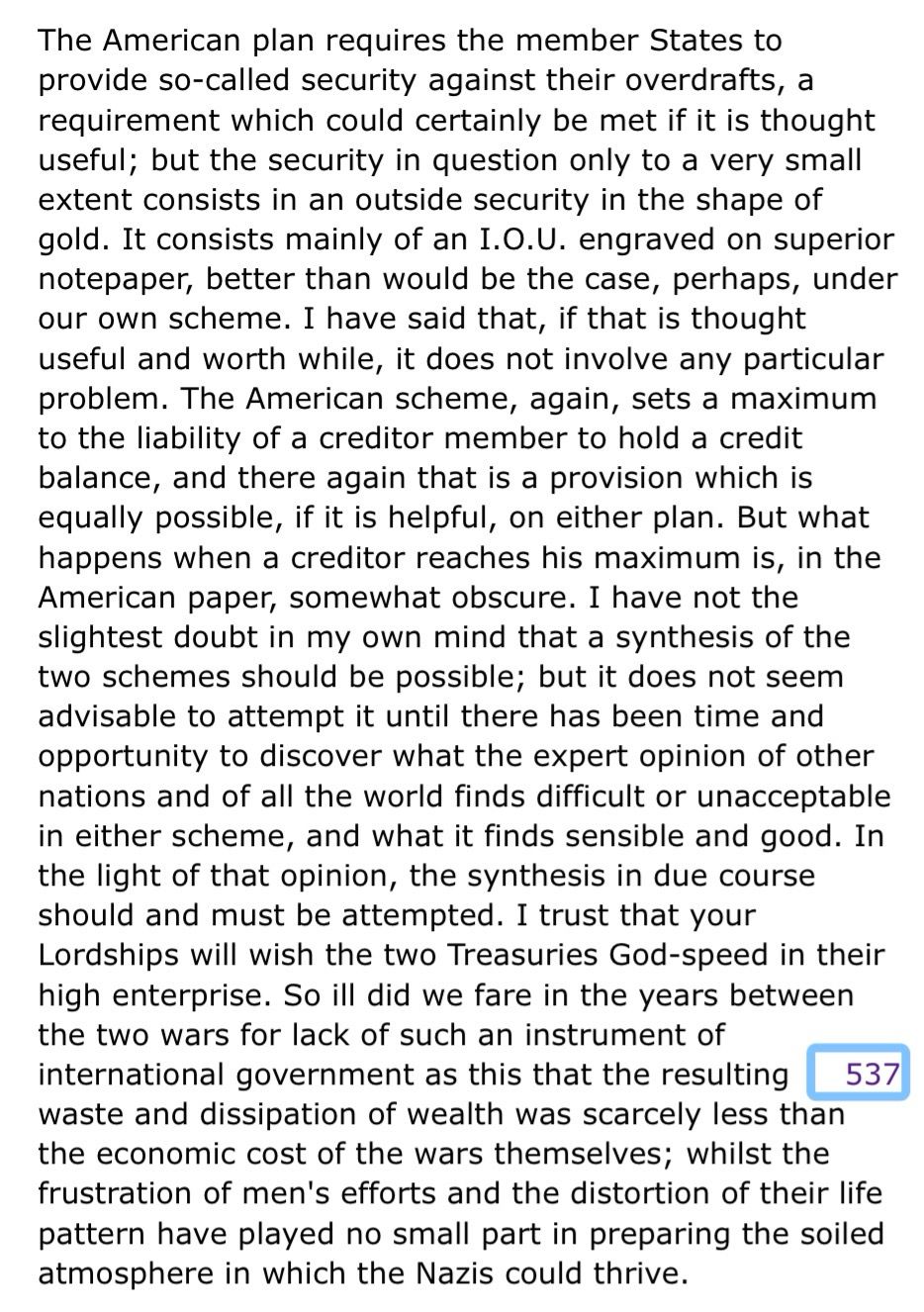

my approach to literature is much too casual and eclectic to give great answers. this week i’ve been reading Keynes on his ICU proposal, where he is quite explicit about failures of economic governance yielding fascism. api.parliament.uk/historic-han...

Text: The American plan requires the member States to provide so-called security against their overdrafts, a requirement which could certainly be met if it is thought useful; but the security in question only to a very small extent consists in an outside security in the shape of gold. It consists mainly of an I.O.U. engraved on superior notepaper, better than would be the case, perhaps, under our own scheme. I have said that, if that is thought useful and worth while, it does not involve any particular problem. The American scheme, again, sets a maximum to the liability of a creditor member to hold a credit balance, and there again that is a provision which is equally possible, if it is helpful, on either plan. But what happens when a creditor reaches his maximum is, in the American paper, somewhat obscure. I have not the slightest doubt in my own mind that a synthesis of the two schemes should be possible; but it does not seem advisable to attempt it until there has been time and opportunity to discover what the expert opinion of other nations and of all the world finds difficult or unacceptable in either scheme, and what it finds sensible and good. In the light of that opinion, the synthesis in due course should and must be attempted. I trust that your Lordships will wish the two Treasuries God-speed in their high enterprise. So ill did we fare in the years between the two wars for lack of such an instrument of international government as this that the resulting waste and dissipation of wealth was scarcely less than the economic cost of the wars themselves; whilst the frustration of men's efforts and the distortion of their life pattern have played no small part in preparing the soiled atmosphere in which the Nazis could thrive.

Text: The American plan requires the member States to provide so-called security against their overdrafts, a requirement which could certainly be met if it is thought useful; but the security in question only to a very small extent consists in an outside security in the shape of gold. It consists mainly of an I.O.U. engraved on superior notepaper, better than would be the case, perhaps, under our own scheme. I have said that, if that is thought useful and worth while, it does not involve any particular problem. The American scheme, again, sets a maximum to the liability of a creditor member to hold a credit balance, and there again that is a provision which is equally possible, if it is helpful, on either plan. But what happens when a creditor reaches his maximum is, in the American paper, somewhat obscure. I have not the slightest doubt in my own mind that a synthesis of the two schemes should be possible; but it does not seem advisable to attempt it until there has been time and opportunity to discover what the expert opinion of other nations and of all the world finds difficult or unacceptable in either scheme, and what it finds sensible and good. In the light of that opinion, the synthesis in due course should and must be attempted. I trust that your Lordships will wish the two Treasuries God-speed in their high enterprise. So ill did we fare in the years between the two wars for lack of such an instrument of international government as this that the resulting waste and dissipation of wealth was scarcely less than the economic cost of the wars themselves; whilst the frustration of men's efforts and the distortion of their life pattern have played no small part in preparing the soiled atmosphere in which the Nazis could thrive.

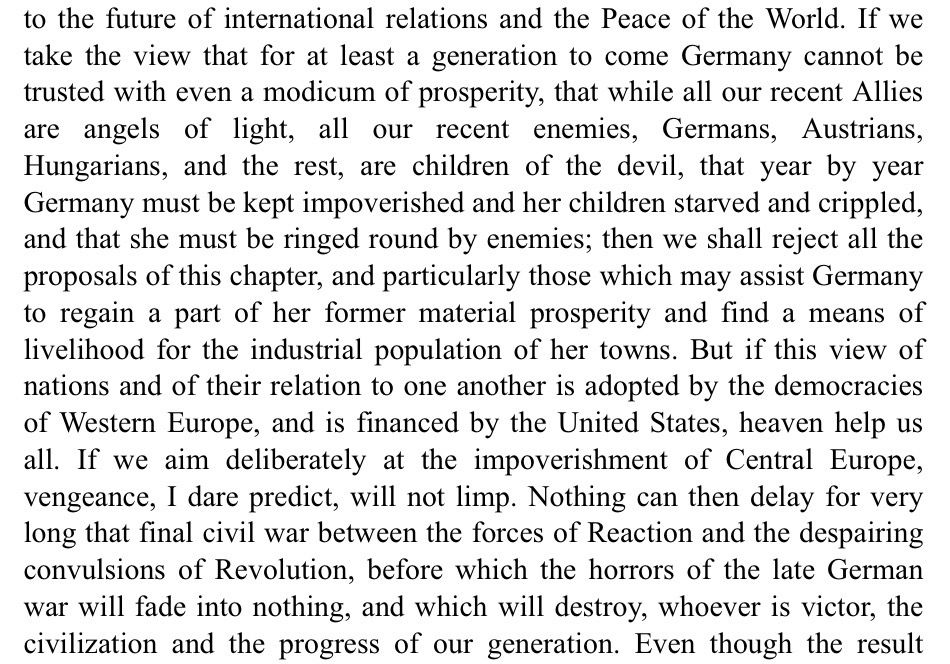

extraordinarily Keynes predicted the calamities, not as an outgrowth of economic liberalism per se, but as an outgrowth of unsupportable indebtedness. ICU is fundamentally about preventing dangerous indebtedness that emerges under liberalism absent regulation. www.gutenberg.org/cache/epub/1...

Text: If we take the view that for at least a generation to come Germany cannot be trusted with even a modicum of prosperity, that while all our recent Allies are angels of light, all our recent enemies, Germans, Austrians, Hungarians, and the rest, are children of the devil, that year by year Germany must be kept impoverished and her children starved and crippled, and that she must be ringed round by enemies; then we shall reject all the proposals of this chapter, and particularly those which may assist Germany to regain a part of her former material prosperity and find a means of livelihood for the industrial population of her towns. But if this view of nations and of their relation to one another is adopted by the democracies of Western Europe, and is financed by the United States, heaven help us all. If we aim deliberately at the impoverishment of Central Europe, vengeance, I dare predict, will not limp. Nothing can then delay for very long that final civil war between the forces of Reaction and the despairing convulsions of Revolution, before which the horrors of the late German war will fade into nothing, and which will destroy, whoever is victor, the civilization and the progress of our generation.

Text: If we take the view that for at least a generation to come Germany cannot be trusted with even a modicum of prosperity, that while all our recent Allies are angels of light, all our recent enemies, Germans, Austrians, Hungarians, and the rest, are children of the devil, that year by year Germany must be kept impoverished and her children starved and crippled, and that she must be ringed round by enemies; then we shall reject all the proposals of this chapter, and particularly those which may assist Germany to regain a part of her former material prosperity and find a means of livelihood for the industrial population of her towns. But if this view of nations and of their relation to one another is adopted by the democracies of Western Europe, and is financed by the United States, heaven help us all. If we aim deliberately at the impoverishment of Central Europe, vengeance, I dare predict, will not limp. Nothing can then delay for very long that final civil war between the forces of Reaction and the despairing convulsions of Revolution, before which the horrors of the late German war will fade into nothing, and which will destroy, whoever is victor, the civilization and the progress of our generation.

in the General Theory, written before the full, um, bloom of fascism, during the depression, Keynes is pretty clear that his project is to rescue what was good from the optimistic liberalism of his — now our! — youths 1/

while layering on top of ideas that proved too simple tools that might forestall what had already proved its catastrophic failure modes. /fin

(seems like an interesting and important thing to try to explain, how and why they swung so hard! and maybe, to someone with sensibilities like mine at least, a hopeful one!)

yes! i think we’re agreeing, just interpreting slightly differently. he treats historical events as contingencies, shocks. 1/

what i’m suggesting is it’s best not to interpret that as Piketty making a claim that this is the only or the best way to treat such events. 2/

it is better to understand that as reflective of *his project*, which like any project attends to some things and simplifies, abstracts away the complexity, of other things. 3/

Piketty attends to a core wealth dynamic, abstracts away a lot of other stuff as mere contingency. but that’s not really a claim that everyone should shrug off those other things as mere contingency. it’s an artifact of, the negative space surrounding, what Piketty devotes himself to explaining./fin

nonquantifiable and Rorschach test are very far from the same thing. most of what matters in human affairs is not adequately represented by quantities. 1/

what is the quantity that distinguishes the groups fighting for a sliver of land between the river and sea? take their vitals, the numbers are about the same. 2/

yet there is something real, something less idiosyncratic than a Rorschach test, that means they’ve spent decades in an ever spiraling conflict that now threatens to burn down the world. 3/

and still we can’t quantify the distinction between them. /fin

to Piketty the garish events of midcentury last century are a shock that briefly undoes an almost inexorable dynamic of growing hierarchy. 1/

(his actual politics are not so fatalistic, but he explains continuing concentration of wealth in such deterministic terms. ironically, shocks of fascism and war creates space for a kind of respite!) 2/

i think it’s better to treat say a Piketty-ish approach and a Polanyi-ish approach as complementary. the events Piketty takes as shocks are the events Polanyi/Keynes/Arendt etc want to explain. 3/

i don’t think Piketty means to suggest no explanation is worthwhile. i think it is just not his thing as a modeler of the dynamics of wealth to explain them. 4/

so while he models those dynamics, he treats these events — which even in his tale are the most startling events in all if history! — like a comet. economists don’t model comets, but that doesn’t mean astronomers shouldn’t. /fin

no intervention precludes the possibility we might just have a heart attack and die, so really it’s not worth investigating heart healthy diets? the Keynes / Polanyi tradition makes pretty specific claims about particular kinds of errors we can avoid. 1/

even if 1000 years of peace and prosperity were to result from a more resilient social democratic turn than the last one, this too will pass, sure. but i’d go for that 1000 year moment anyway, wouldn’t write it off as nbd. /fin

i mean, i’d say we have demonstrated the claim about as well as anything is demonstrated in its domain! which, yes, is very far from perfect. 1/

but that imperfection extends to the full domain of social affairs (i try to avoid “social science”), because even where you think you have a big sample, you almost never have construct and external validity. 2/

you get data generated from processes that might be completely different if apparently distant aspects of context would change. 3/

our condition with respect to social affairs is we have to make actual choices under deep forms of uncertainty. there is no kind of formal procedure that can adequately guide us, although it can be useful to use formal procedure to inform our judgment. 4/

(even with the most quantitative social-science-paper-y forms of evidence, it is ultimately a matter of judgment whether applying the evidence will “work” in the slightly new social context the present is, or whether it would be better to take some action that would overthrow the context anyway.) 5/

the thesis economic liberalism -> social dysfunction -> backlash to tribalism/fascism can’t be demonstrated in a way that someone whose priors are adamantly opposed has to defer to, sure. in midcentury Hayek et al objected to it, which played some role in our arguably rerunning the experiment. 6/

let’s concede that. we are in a world where our judgment must be responsible for more than what we can with any certainly fully understand. 7/

what does your judgment take from the historical arc, triumphalist-turn-of-20th-c globalism/liberalism, war-depression-fascism, social democratic trente glorieuses, great inflation, triumphalist-1990s-globalism/liberalism, war-and-economic-crises, resurgent fascism? 8/

your take won’t be science, as neither is mine, but we have little choice but to have one, because the next stage is on us to perform, optimistically on us at least to some degree to choose. /fin

not really. multidecade social and historical theses aren’t going to have quantitative p < 0.05 kinds of evidence. we had mid century (last century) the most perceptive people of the era (Keynes, Polanyi) observe events and advance the thesis. then we reran the experiment, with similar results. 1/

i think that’s about as close to a slam dunk as you get in historical narrative arcs. /fin

i hate this era we are living through.

on the theory that we do the stupidest, laziest-but-politically-expedient possible thing, i can’t argue. 1/

but contributing to the massive rest-of-world oil shock we provoked for the convenience of big-ass truck drivers fetching a gallon of milk is going to do wonders for our place within the hearts and minds of our erstwhile allies. /fin