Steve Randy Waldman

@interfluidity.com

it’s not a dark enlightenment, what we are undergoing is a dark reenchantment. people’s understanding of the world is increasingly formed by sources seeking to intrigue or awe, rather than inform with anything like procedurally vetted approximations of mundane truth.

Steve Randy Waldman

@interfluidity.com

if you configure a bell to chime every time you get a like, that’s an engagement ring.

Steve Randy Waldman

@interfluidity.com

to be fair, the humans don’t seem to do much better with their tiktok than the llms do with all the crap and slop in their training data.

Steve Randy Waldman

@interfluidity.com

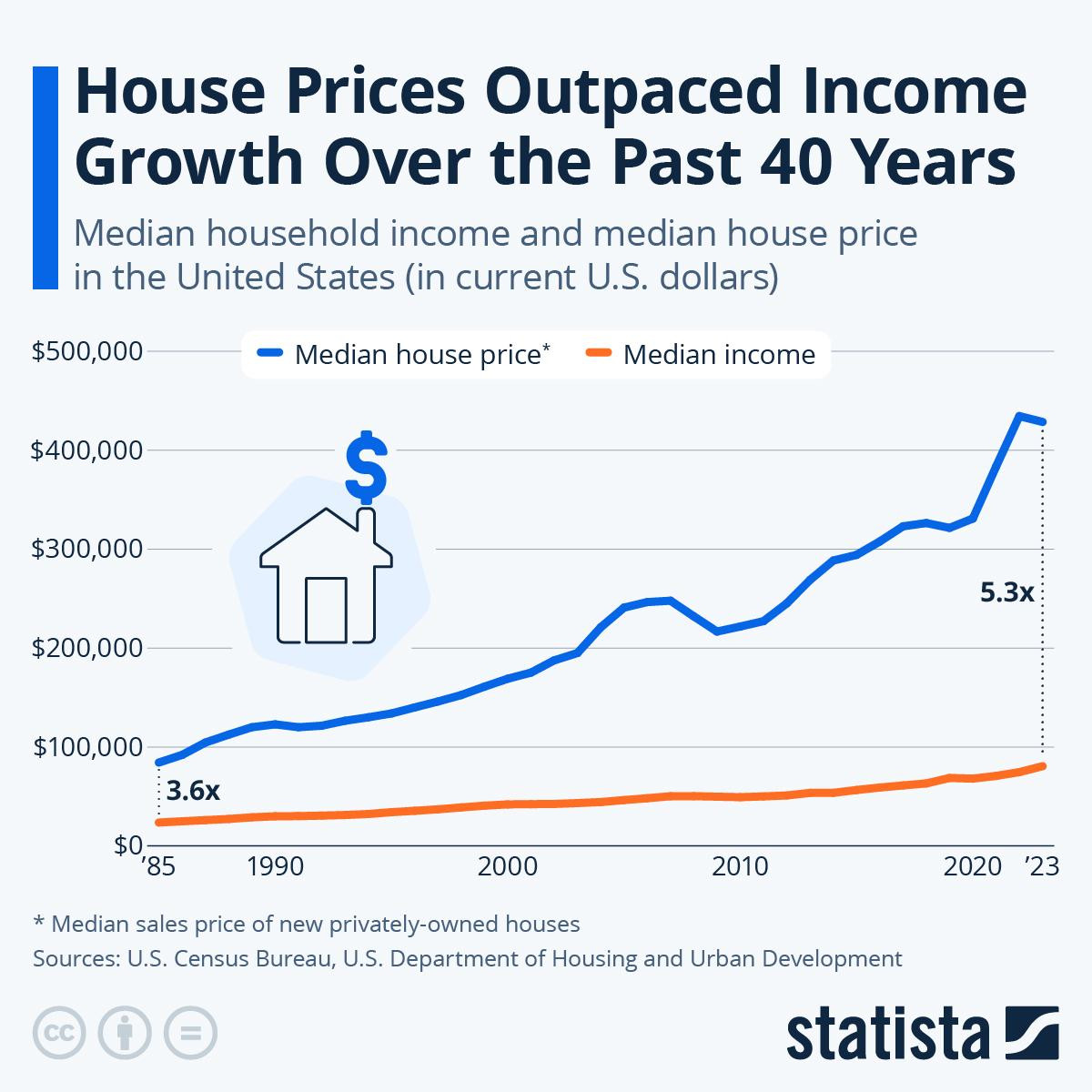

lots of conversation inspired by this, arguments about interest rates and square feet etc, but i think people fail to appreciate how profoundly just *the last five years* of this graph have contributed to a profound sense of hopelessness for many of us. (with interest rates way up, not down!)

Loading quoted Bluesky post...

Steve Randy Waldman

@interfluidity.com

A graph showing median home prices growing much faster than median incomes, with a really shocking increase in median home prices since the 2020 pandemic.

A graph showing median home prices growing much faster than median incomes, with a really shocking increase in median home prices since the 2020 pandemic.

Steve Randy Waldman

@interfluidity.com

i'm sure i've missed some text or tweet or mail or call and offended you.

Steve Randy Waldman

@interfluidity.com

after sunlight is reflected across so many funhouse mirrors, does it still serve as a disinfectant?

Steve Randy Waldman

@interfluidity.com

yesterday i was a bit shocked by the degree to which “flat earth tiktok” had otherwise perfectly normal people just asking questions.

Steve Randy Waldman

@interfluidity.com

excellent but dark. all i can say is, optimism of the will, motherfuckers. ht @olepetter.bsky.social

Loading quoted Bluesky post...

Steve Randy Waldman

@interfluidity.com

i agree with that! it’s about how you generate supply, not just of sq ft of “housing”, but of desirable living spaces in dense, attractive neighborhoods, at scale and at speed. i think it will take some creativity.

Steve Randy Waldman

@interfluidity.com

contractors probably not. they have no ownership stake and are paid by the job. but "capital disciple" — tacit pacing of investment at an industry level to avoid destructive price competition — is ubiquitous. in the US, the charge is mostly leveled at "landbanking" by larger homebuilders.

Steve Randy Waldman

@interfluidity.com

different markets! in the US the reluctat supplier story is about landbanking and the sprawl-builders, not a claim that developers are rationing construction in Pacific Heights. the constraints that bind are different in different places, different markets.

Steve Randy Waldman

@interfluidity.com

no. i think no one can do infill at scale in already affluent / desirable urban neighborhoods, but homebuilders know how to do sprawl. the market would love the infill, but the incumbents do not, and unless the incumbents are downscale, they win.

Steve Randy Waldman

@interfluidity.com

i guess i think you are being unfair here to the plutocrats. it might have ended up becoming a destructive commute source to SF, but the people behind California Forever were genuinely trying to make a new city. if they wanted to be Lennar they’d have succeeded.